The New Great Game – Geopolitics of Critical Minerals

In the first week of July, while the news of China restricting exports of Germanium and Gallium grabbed the headlines, India also upped the Ante in this “New Great Game”, driven by the geopolitics of critical minerals and the race to secure the supply chains.

On 3rd July 2023, China announced that it is restricting exports of two rare metals, Germanium, and Gallium, which are key to the production of semiconductors and other high-tech products, which is seen as retaliatory to sanctions imposed by US and allies against China’s semiconductor industry. While this news grabbed headlines and attention, not reported, or missed by much of the media were two policy decisions by India.

· In the last week of June, Indian Ministry of Mines released a comprehensive Critical Minerals List, consisting of 30 metals and minerals deemed critical for India’s ambitions in green energy, electronics, telecommunications, transport and defence. The list comprises of 17 rare earth elements (REEs), six platinum group metals (PGMs) and four “Battery Critical” elements: Lithium, Cobalt, Graphite, and Nickel. The list also includes Copper, a mainstay and key component for the green energy transition.

· As a part of this broader critical mineral play, during his recent visit to US, Prime Minister Narendra Modi announced that India will be joining the Minerals Security Partnership (MSP), which is a partnership between the US, Canada, UK, France, Germany, Japan, South Korea, and several other countries formed in June 2022 as an initiative to bolster supply chains for critical minerals.

India is stepping-up its game on a broader canvas, where countries across the globe are scrambling to secure critical minerals supply chains and aim to decouple from China, which has long dominated in supply of most critical minerals.

Welcome to the “New Great Game”!!

Understanding the New Great Game

What came to be known as “The Great Game” was played out for the larger part of the 19th century, between the British and Russian Empires in Central and South Asia. It was a diplomatic chess game to secure and control the routes leading to India. While there was no direct military confrontation, there was intense competition to forge alliances with countries in the region and in case of Afghanistan, pre-emptive military action by the British.

What we are witnessing now is a more intense form of the great game, a competition not for routes but resources, led by two countries and their allies: USA and China. This Great Game will be about securing control over the minerals that are critical for our daily life today, all the digital technologies and appliances that have become the mainstay and more critically, for our quest towards clean and renewable energy.

We are living in a fractured geopolitical order and an increasing polarized world with diverging and fragmented priorities. The reconfiguration of supply chains is at the heart of this trend as governments try to prioritize and engage in aggressive and confrontational industrial policy race, especially in strategic technologies, a few examples which are for everyone to see:

· The Inflation Reduction Act (IRA) and the CHIPS and Science Act in the USA.

· Europe’s Critical Raw Materials Act, and

· China’s Made in China 2025 program.

These policies are focussed on two objectives:

1. Maintain or restore manufacturing advantages in strategic sectors, such as clean energy and advanced electronics.

2. Reduce dependence on geopolitical competitors like China.

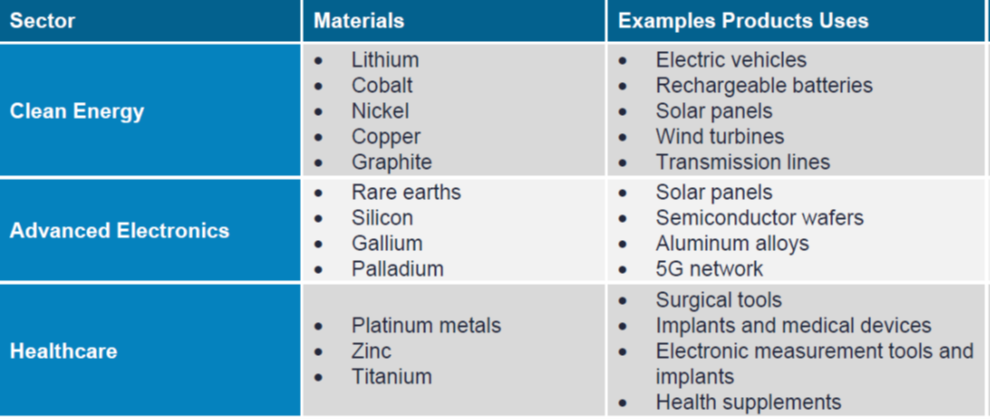

Before we get into more details, let us look at some select sectors and their dependence on critical minerals.

As digital technologies dominate our daily life and the move to clean energy becomes a national priority globally, these minerals will play a more important role. Oil and other Hydrocarbons dominated the geopolitics of 20th century, but in a changing world, the oil order dominated by US and its allies is being replaced by countries led by China, who seek to assert their growing importance and power. The world is dependent on a few key players for critical minerals across clean energy, advanced electronics, and healthcare sectors. Today’s players might be different, but their methods, tactics and strategies will bear an uncanny resemblance to those employed by the British and the Russians in the 19th century.

Many of us, immersed in our make-believe digital world, grossly underestimate the importance of this new “Material World” and the implications of any supply chain disruptions to our daily life, a glimpse of it being the semiconductor crisis during Covid.

It has become fashionable for some to propagate the “Dematerialization of Life” myth, built around the fanciful fact that, we now consume less material per dollar of income and the growing importance of services in the economy. But here is the bitter truth: The Material World is the backbone our everyday lives. Without them, our beautifully designed smartphones wouldn’t switch on, our electric cars would have no battery and at the basic level, many of our new energy technologies and the grids that supply our electricity would not function. In 2019 alone, we mined, dug, and blasted more materials from the earth’s surface than the sum total of everything we extracted from the dawn of humanity all the way through to 1950. Our lives won’t come to a grinding halt, if Twitter, Instagram, and Facebook disappear today, but they sure will come to a halt, if a few of these critical minerals are not produced.

In the rest of this post, I will dig a little into the importance of minerals for Semiconductors and Green Energy and also the criticality of Rare Earths. I will skip the EV part as I have covered about it and Lithium in my earlier post, Battery Arms Race, Lithium and China

Mineral Intensity of Green Energy

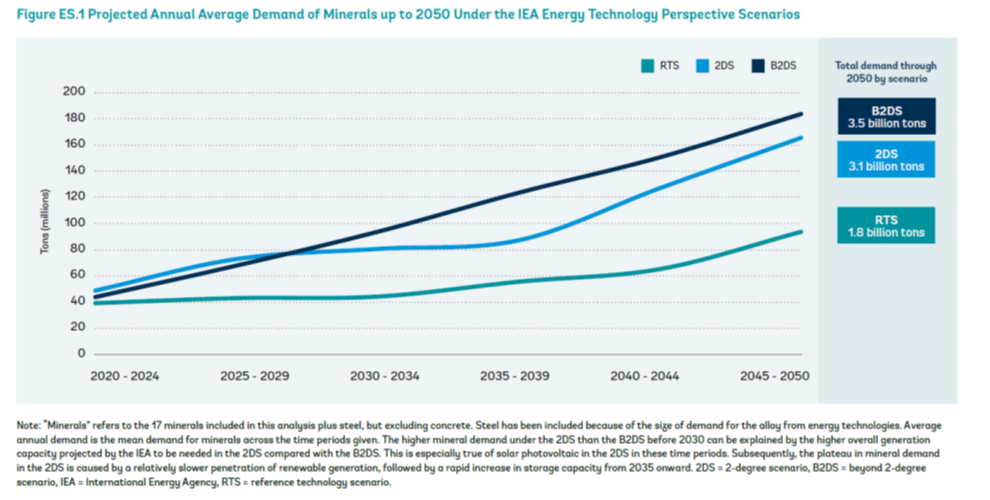

With the move away from fossil fuels accelerating across the globe, there is a growing awareness about the role of critical minerals, rising prices, supply chain delays and disruption. In a report titled, "Minerals for Climate Action: "The Mineral Intensity of the Clean Energy Transition," World Bank findings project the production of minerals, such as graphite, lithium and cobalt, could increase by nearly 500% by 2050, to meet the growing demand for clean energy technologies. It estimates that over 3 billion tons of minerals and metals will be needed to deploy wind, solar and geothermal power, as well as energy storage, required for achieving a below 2°C future.

The clean energy transition is expected to be much more mineral intensive than fossil-fuel based electricity generation. It is important to understand the extent to which mineral demand will grow globally to supply renewable energy and storage technologies. Minerals that are used across different renewable technologies: Copper, Aluminium, Chromium, Manganese, Molybdenum, and Nickel make then critical. Other minerals that have concentrated applications face higher levels of changes in demand. Graphite and Lithium demand are so high that current production would need to ramp up by nearly 500 percent by 2050 just to meet demand. On the other hand, demand for Aluminium has the highest absolute levels of demand from any of the minerals.

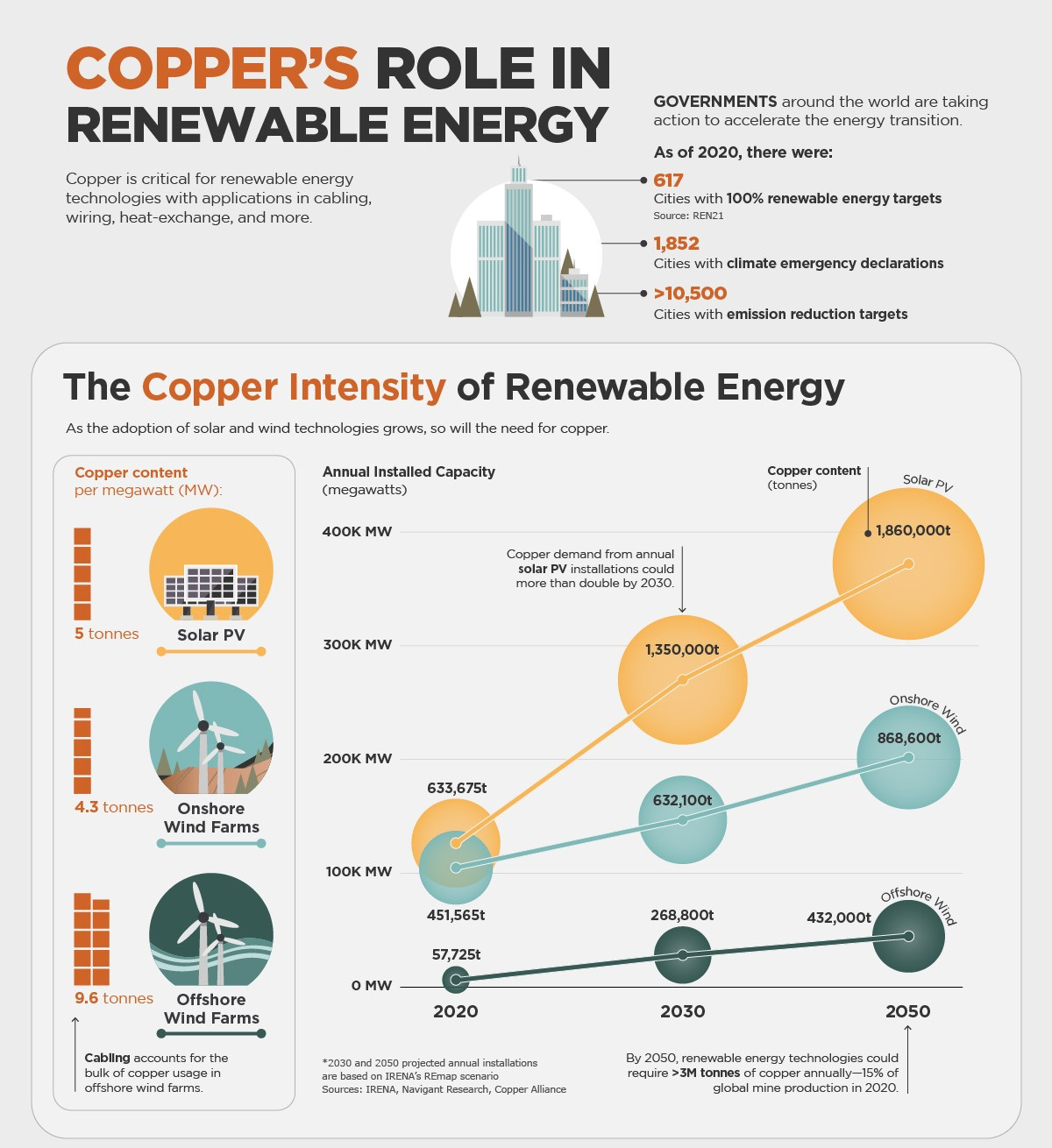

Now consider the humble Copper, which stands out due to its critical role in building both the technologies as well as the infrastructure. Copper has one of the highest thermal and electrical conductivity and as a result, is the most widely used mineral among energy technologies. Solar PV primarily rely on copper for cabling, wiring, and heat exchange due to its efficiency in conducting heat and electricity. Wind energy make use of it for turbines, cables, and transformers. Demand in offshore wind farms is high because they are connected to land via long undersea cables that are made of copper. Copper is also a key part of the grid networks that transmit electricity. With the increasing adoption of renewable energy, the demand for copper will only grow.

In a report, Geological Survey of Finland, highlighted the mineral implications for achieving the planned energy transition. They found that, the resulting demand for nearly every necessary mineral, including common ones such as copper, nickel, graphite, and lithium, would exceed not just existing and planned global production capabilities, but also known global reserves of those minerals. Another analysis by the Wood Mackenzie found that if EVs were to account for two-thirds of all new car purchases by 2030, dozens of new mines must be opened just to meet automotive demands, each mine the size of the world’s biggest in each category today. But 2030 is only seven years away and opening a new mine takes 16 years on average.

Richard Feynman once said that “it is important to realize that in physics today, we have no knowledge what energy is.” But today, we definitely know without a doubt that delivering all the energy we require will be all about minerals and materials.

The race is on among countries to ensure they have control and access to these minerals.

Semiconductors and Critical Minerals

Why did China restrict the export of Gallium and Germanium? While it is a retaliation against Chinese semiconductor industry by US and its allies, that does not explain the whole thing.

Gallium and Germanium are strategic elements predominantly used in electronics. Both are byproducts from processing other commodities such as Coal and Bauxite. Gallium-based compounds, such as, Gallium Arsenide and Gallium Nitride are used in the production of semiconductors, LEDs, and solar panels. The largest use of Germanium is in the semiconductor industry. When doped with small amounts of Arsenic, Gallium, Indium, Antimony or Phosphorus, Germanium is used to make transistors for use in electronic devices. China is the world’s largest producer of these two elements, with more than 95 per cent of the global gallium output and 67 per cent of germanium production.

To understand this better, let us visualize the Semiconductor value chain.

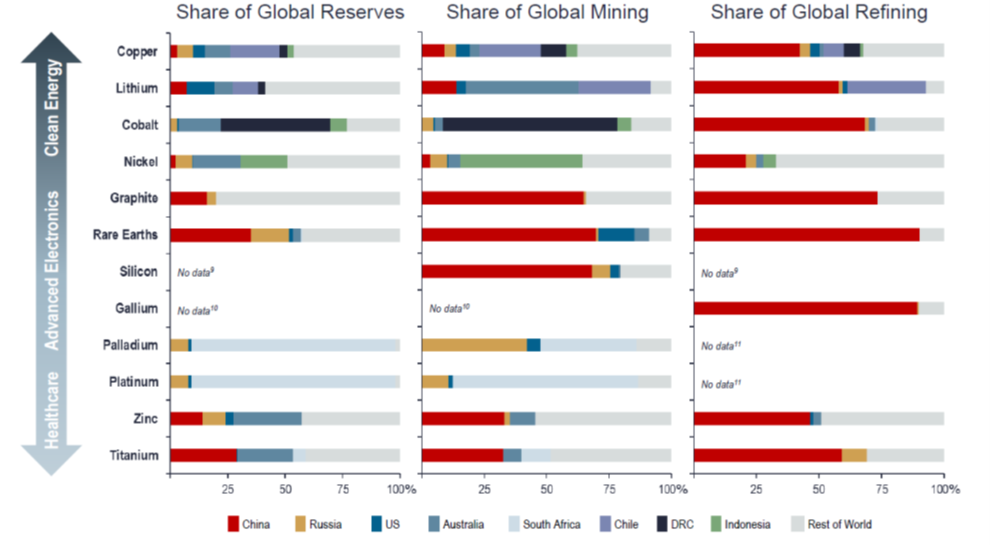

The semiconductor supply chain is highly globalised and interdependent. Each step in the main supply chain is concentrated in a different geographical region of the world, has its own distinct market characteristics, and relies on its very own chain of suppliers. The semiconductor value chain and the critical raw material supply chain balance each other out. While the semiconductor value chain is dominated by US and its allies, the supply chains of crucial minerals for the production of semiconductors is dominated by China and Russia, among others.

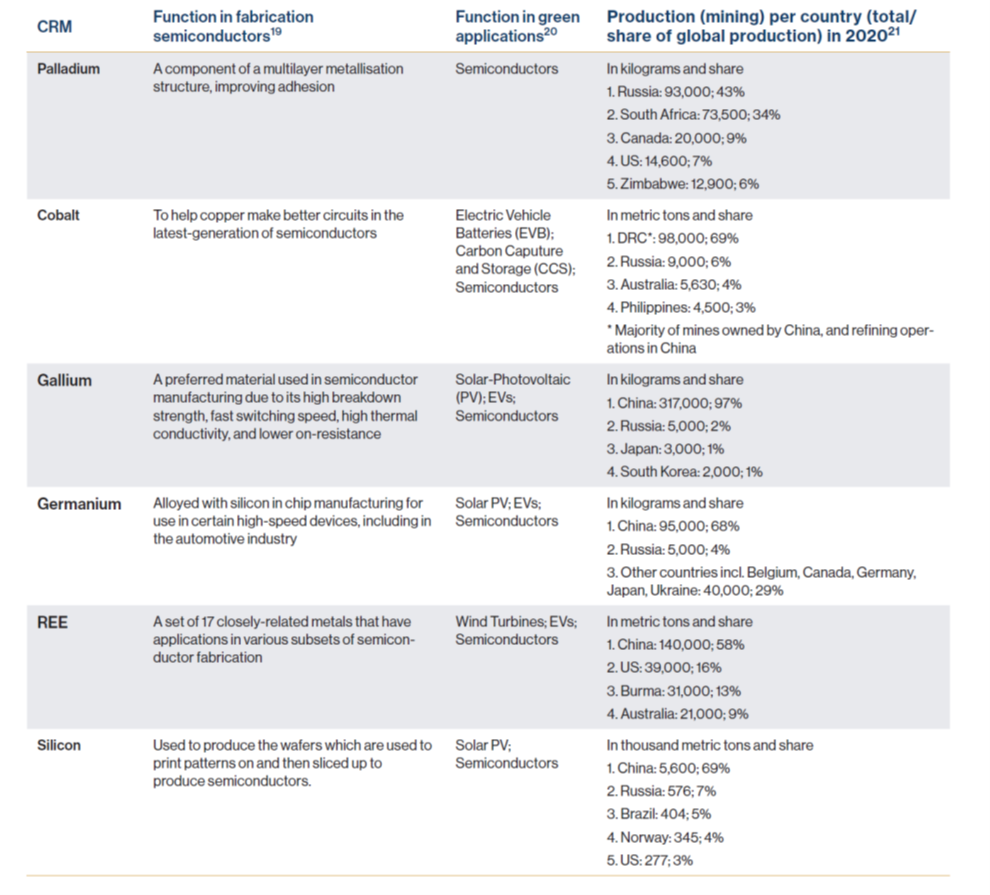

Critical minerals, such as Palladium, Cobalt, Gallium, Germanium, Rare Earth Elements (REE) and Silicon, constitute the foundation upon which the entire semiconductor supply chain rests, including essential supplies of anything ranging from equipment and wafers. These are exacerbated by various geological and economic limitations: availability of deposits, time needed to set up mining, refining and processing capacity, and environmental impacts of mining, which complicate relocating the industry elsewhere. Currently there is over reliance on China and Russia for the supply of these critical minerals and poses a profound threat to the semiconductor industry in US, EU, Japan and Korea. Similarly, political and social instability in countries such as DRC adds to the insecurity of the supply chains.

China and Russia have a stranglehold over six key critical minerals required for the fabrication of semiconductors.

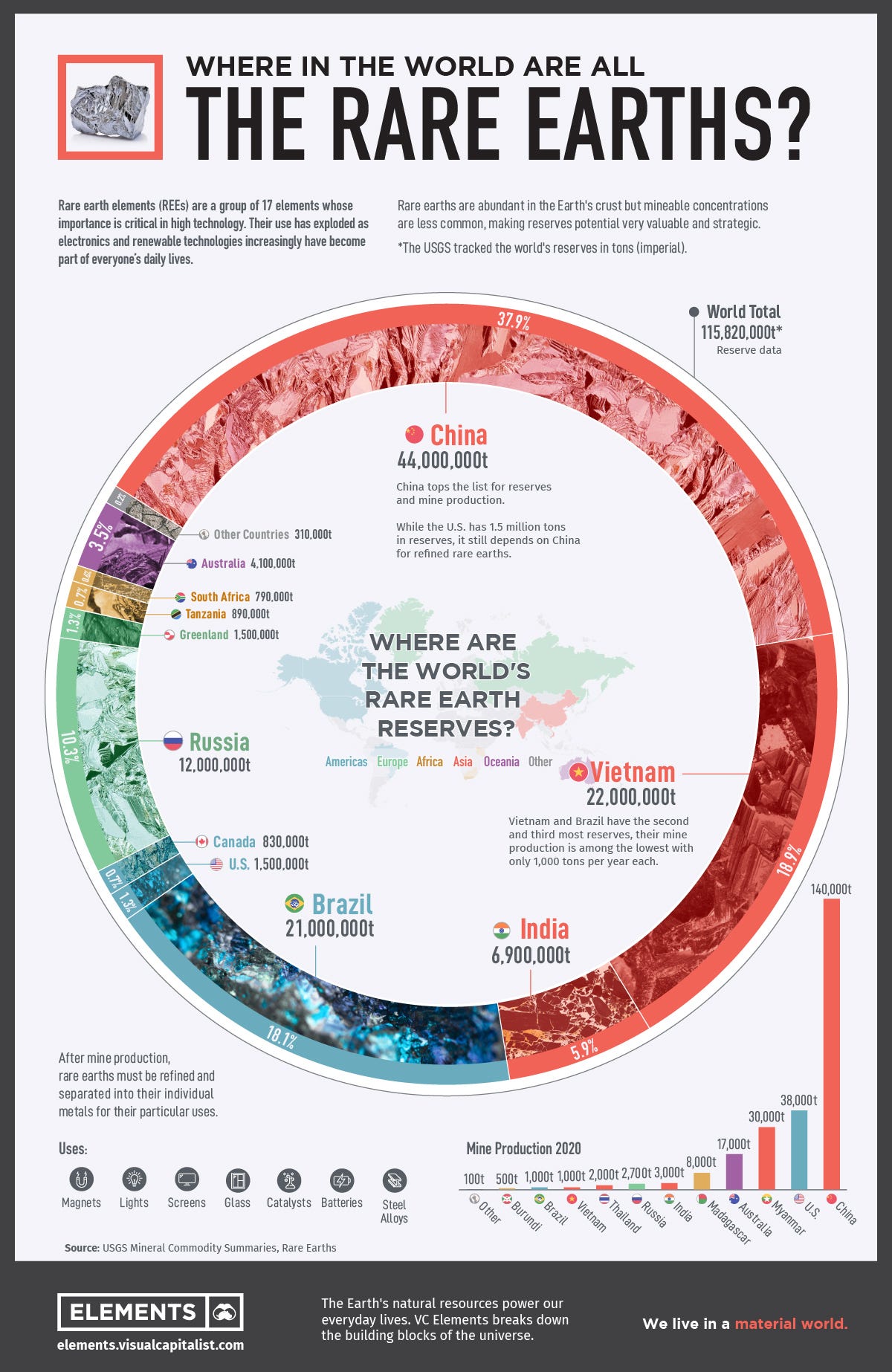

Rare Earth Elements – Not So Rare But Critical

Cutting across all digital, renewable and defence applications are Rare Earth Elements (REE).

REE is a collective term for seventeen chemical elements in the periodic table consisting of Yttrium, Scandium, and the 15 elements of the Lanthanide series. Despite their name, REEs are not very rare and found far more commonly in the Earth’s continental upper crust than most precious metals such as Gold and Platinum. Some REEs such as Cerium are as abundant as industrial metals like Copper and Nickel. However, this abundance is distributed throughout the crust and is rarely found in concentrated deposits. REEs are therefore costly and energy intensive to extract. The four lightest REEs: Lanthanum, Cerium, Praseodymium, and Neodymium, typically constitute more than 80% of these deposits, and heavier REEs such as Europium, Terbium, and Dysprosium are much more difficult to find. Materials that contain REEs are crucial for manufacturing of electronic and optoelectronic devices as well as high-power magnets for electrical power generation.

As of today, China accounts for 63 percent of the world’s rare earth mining, 85 percent of rare earth processing, and 92 percent of rare earth magnet production. Rare earth alloys and magnets that China controls are critical components in missiles, firearms, radars and stealth aircraft.

In 2010, China decided to ban exports of rare earths to Japan for a few months after a maritime incident. Japan relied almost entirely on rare-earth imports from China to produce solar panels, car engine components, and magnets, among other technologies. Again in 2019, in response to Trump administrations dealing of Huawei, China threatened to include certain products using rare earths in Beijing’s technology-export restrictions. China could easily decide to restrict access to rare earths again, on a larger scale with bigger and disastrous consequences.

Post the episode in 2010 episode, Japan started working on an aggressive diversification strategy to find alternative suppliers. By 2021, it had successfully achieved a reduction of Chinese rare-earth imports from 90% of total to 60%. Japan also created Japan Australia Rare Earths (JARE), a special-purpose vehicle created to invest in rare earth mining. In 2023, Japan invested $133 million through JARE in Australian rare earth producer Lynas that would secure priority supply rights for Japan until 2038.

Geopolitical and Geoeconomic Implications

Just when the world was recovering from supply chain disruptions induced by Covid, Russia’s invasion of Ukraine has amplified and rekindled the fears and insecurities globally about critical minerals. The breakdown of trade in vital resources: Natural Gas, Neon and temporarily Palladium, between EU and Russia post the invasion, created a febrile atmosphere of mistrust where economic ties between geopolitical contenders, even if mutually beneficial and on the surface solely commercial, cannot be guaranteed.

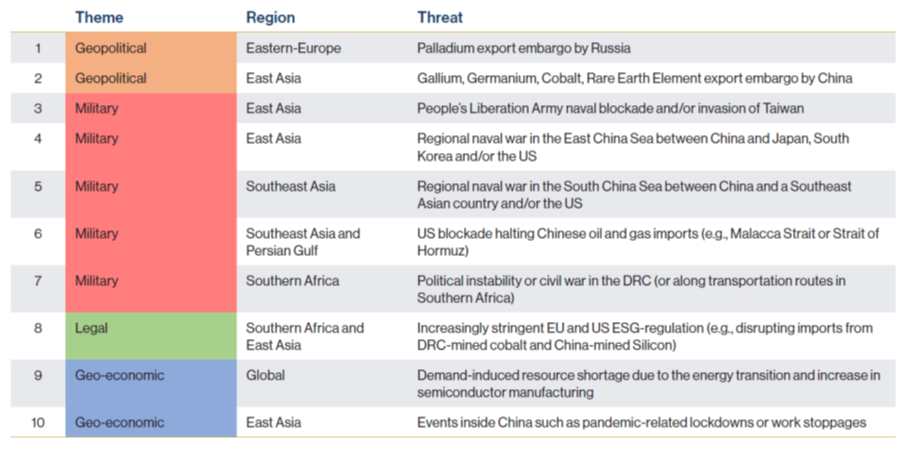

In 2022, post the Russia’s invasion, Hague center for strategic studies identified ten pending threats to the critical raw material for semiconductor supply chain. One of their possible threat, China curbing the export of Germanium and Gallium has already come true.

A few other key critical mineral risks could be:

· With its control over the processing of a vast number of critical materials, China might decide to take further advantage and decide to geopolitically leverage Rare Earths, Graphite, and Titanium. China has strong incentives to do so sooner rather than later, before supply chains shift.

· Growing demand is outpacing supply for copper, a critical material for electricity sector. This might get exacerbated by political situation and risks in top producing countries: Chile, Peru, Russia, the Democratic Republic of Congo (DRC), combined with geopolitical tensions, lagging exploration and production investments, and declining reserve quality.

· The vulnerability of geographic locations where materials are extracted and processed along with the policies implemented by countries that either produce and export materials or source them for the development of their industries.

What we are witnessing might be a perfect storm: a combination of production, policy, and geopolitical factors, which might indicate how supply chains for critical minerals will evolve. Current geopolitical dynamics and the evolving multi-polar dynamics strongly suggest that existing interdependencies will not change in the coming years and China as a top player in the refining of most materials will leverage its position. Added to this will be the growing demand, that could create and amplify supply bottlenecks leading to increase in costs. Materials critical for the green energy sector: Cobalt, Nickel, Graphite, and Rare Earths, face very high level of production and processing concentration by a few countries.

As I had mentioned in my earlier article, Investing for the Future - A New Geoeconomic Reality:

In conclusion, we are entering an era of uncertainty, complexity and volatility. It will come with a host of threats, but also great opportunities. Spotting these opportunities will require all of us to unlearn lessons of the past three decades. We are not returning to world of “Great Moderation” and predictable businesses. What we need is new set of lenses to identify these opportunities and open mind to assess all possibilities and outcomes.