Battery Arms Race, Lithium and China

In early February, there was a media frenzy about discovery of Lithium deposits in J&K. Geological Survey of India (GSI) has established 5.9 million tonnes of inferred resources of Lithium in the Salal-Haimana area of Reasi District of Jammu & Kashmir. Everyone went overboard about India on its path to energy self-sufficiency and how this will turbo-charge EV adoption in the country. What caused this excitement about Lithium and why has Lithium become so important for the world.

Lithium’s importance for EV’s.

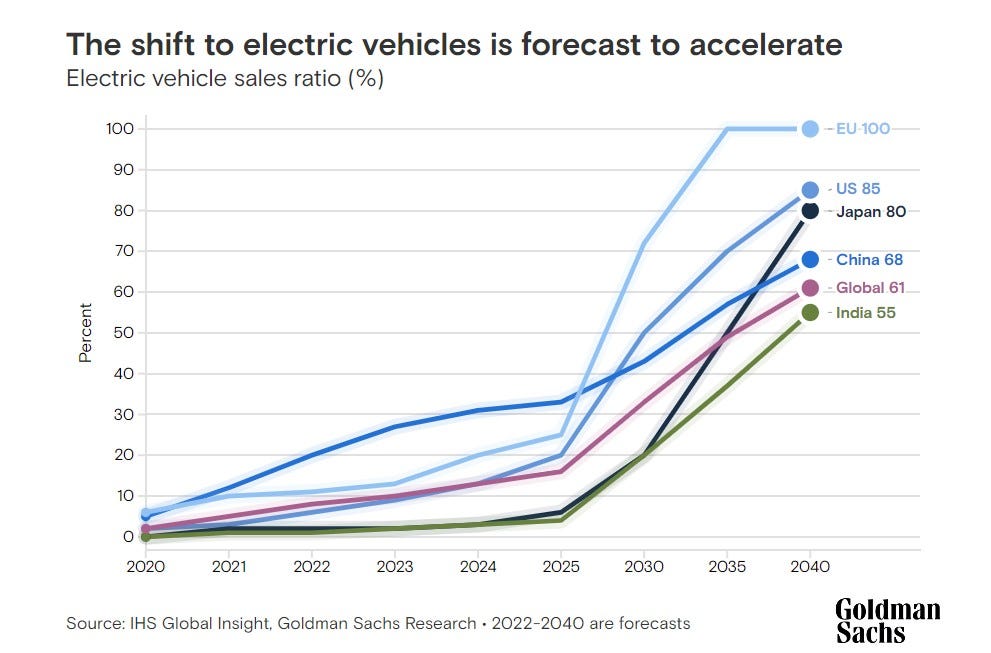

To put it simply, we are entering a Lithium-Ion age. The adoption of electric vehicles is rising sharply aided by government policies and a global push for net-zero carbon emissions.

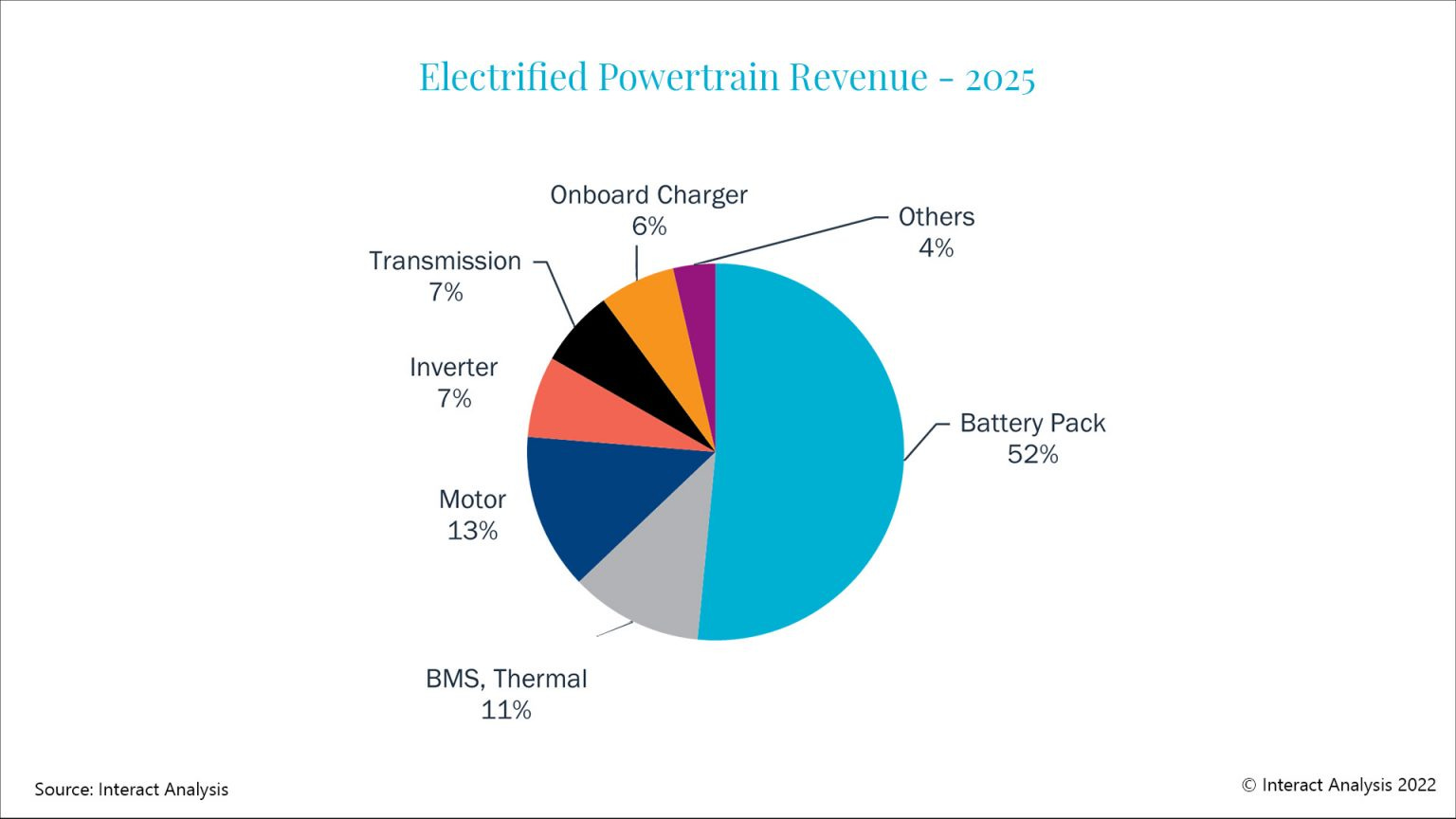

At the center of this phenomenon are “Batteries”, which are the most important part of an electric vehicle and constitute a significant percentage of the cost of the vehicle. Industry experts claim that the battery and related components constitutes ~35-45 percent of cost of an electric vehicle.

For most EV manufacturers, Battery Technology is top of the mind. While there exist different EV battery chemistries and different combinations are seeing a rapid experimentation and evolution to optimize performance, there is a common thread across various EV battery designs: Lithium. It is a near ubiquitous ingredient in current lithium-ion battery cathodes. Solid-state batteries, which could represent the next major innovation in battery technology, are likely to incorporate Lithium in both the cathode and the anode. Looking over the horizon, Lithium’s prominence in battery manufacturing will remain intact even for next-generation technologies for a foreseeable future.

Lithium-ion batteries offer greater energy density, lower self-discharge, and a longer useful lifespan. Lithium is also has ideal chemically as it readily sheds electrons under the right conditions, a property necessary for the intercalation reactions that manage charges within a battery. In sum, lithium-ion batteries store considerable energy in a light package while featuring commercially viable recharging properties for EVs.

The primary components of lithium-ion batteries are a cathode, an anode, a liquid electrolyte, and a separator. In most current designs, the cathode houses lithium during the battery’s idle state.

EV batteries are often classified based on cathode contents. Different types of Li-Ion batteries are:

· LCO or Lithium Cobalt Oxide (LiCoO2)

· LMO or Lithium Manganese Oxide (LiMn2O4)

· NMC or Lithium Nickel Manganese Cobalt Oxide (LiNiMnCoO2)

· LFP or Lithium Iron Phosphate (LiFePO4)

· NCA or Lithium Nickel Cobalt Aluminium Oxide (LiNiCoAlO2)

· LTO or Lithium Titanate (Li2TiO3)

Today, the three most common battery chemistries in EVs are LFP, NMC811, and NMC622. Together these three chemistries account for about 75% of the cathodes placed in EVs across all classes globally. The most relevant battery chemistry remains NMC. Since cathodes also determine the range and account for most of the cost of the overall cell, Lithium plays a very critical role for batteries.

Global battery arms race

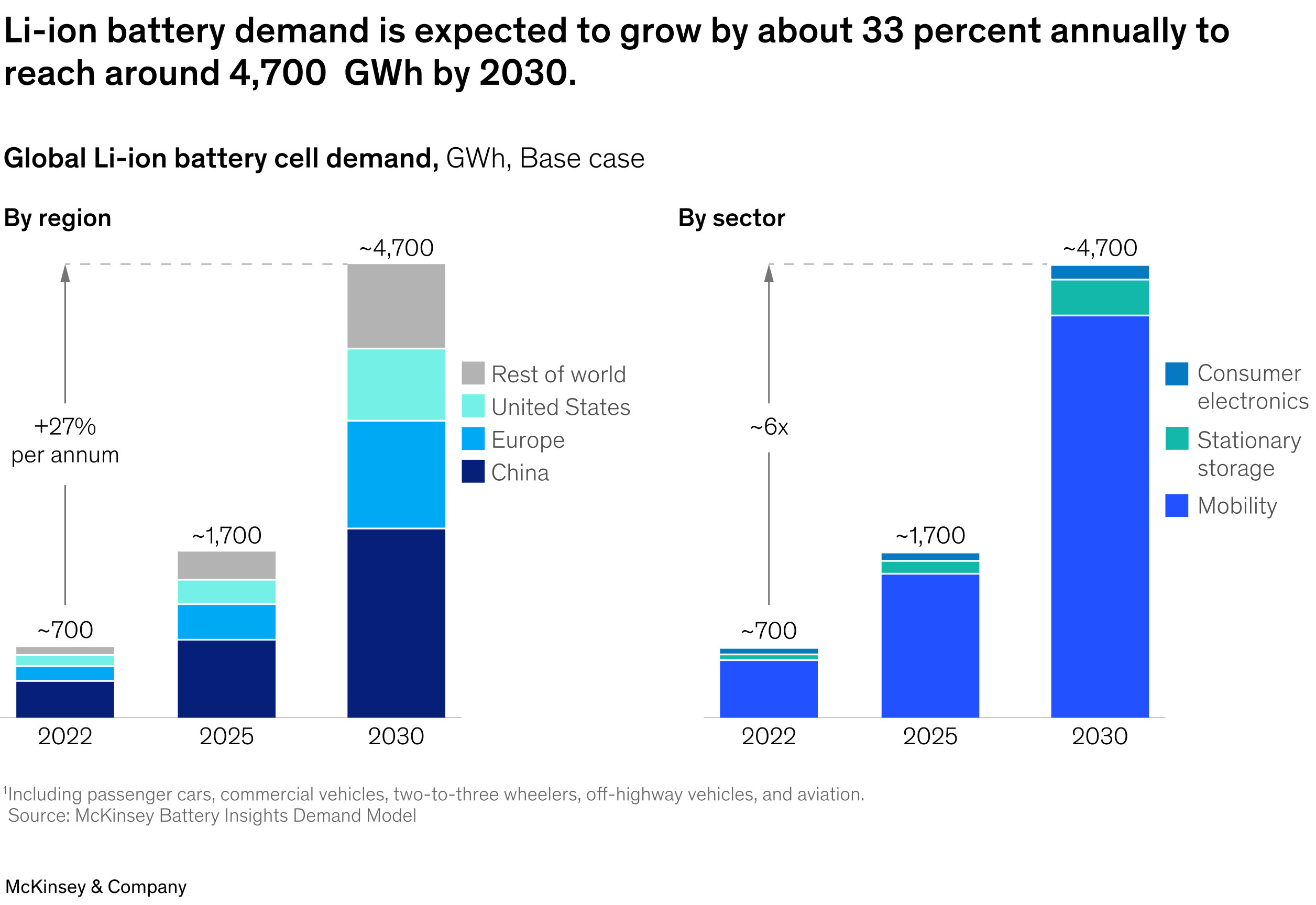

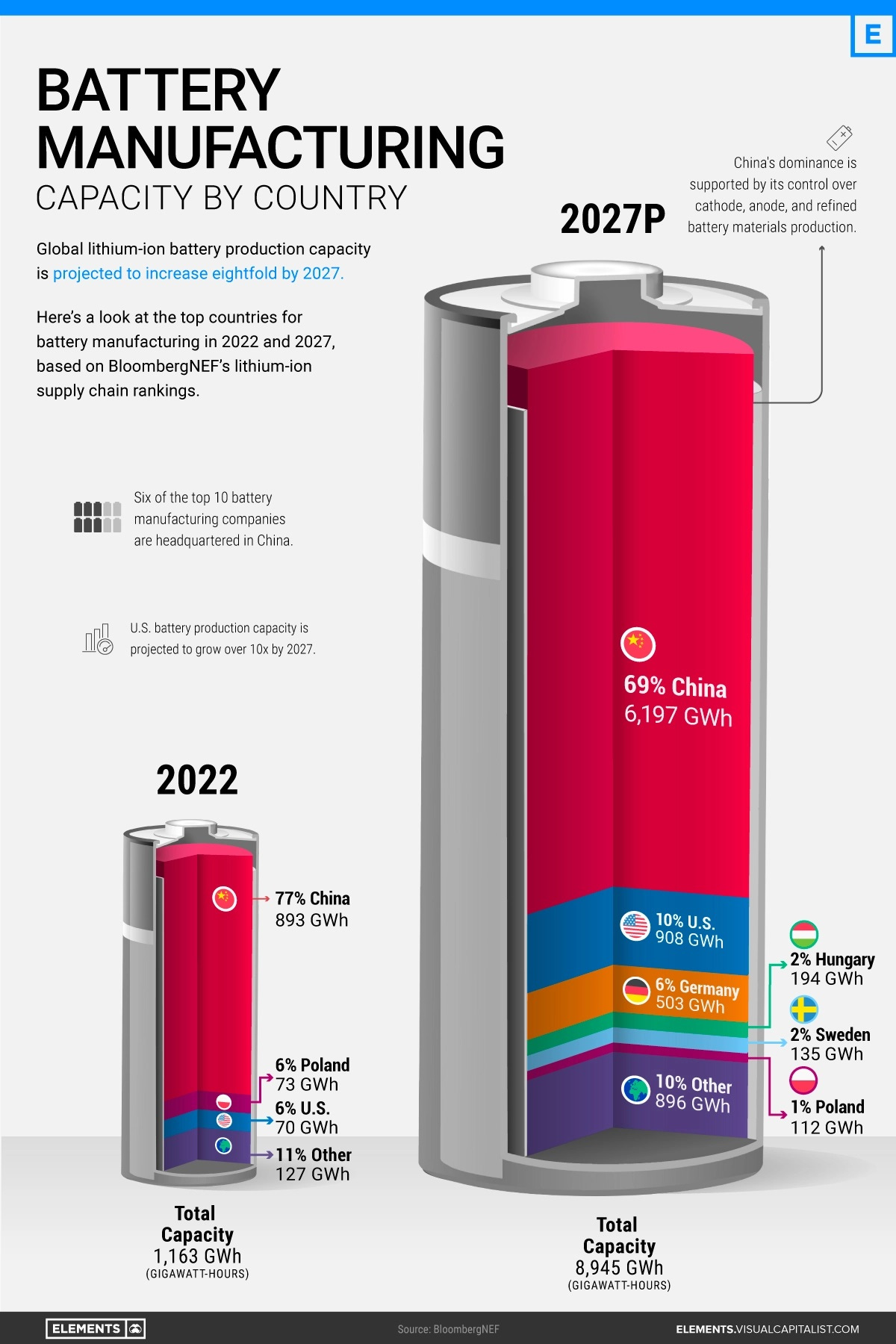

As the demand for electric vehicles is set to skyrocket, according to IEA, it will require 70 million batteries for consumer EV’s alone by 2035. To meet this demand, gigafactories producing new battery capacity will need to increase from the current annual global manufacturing capacity of approximately 500 gigawatt hours to 3,000 gigawatt hours by 2025 and possibly double that by 2030.

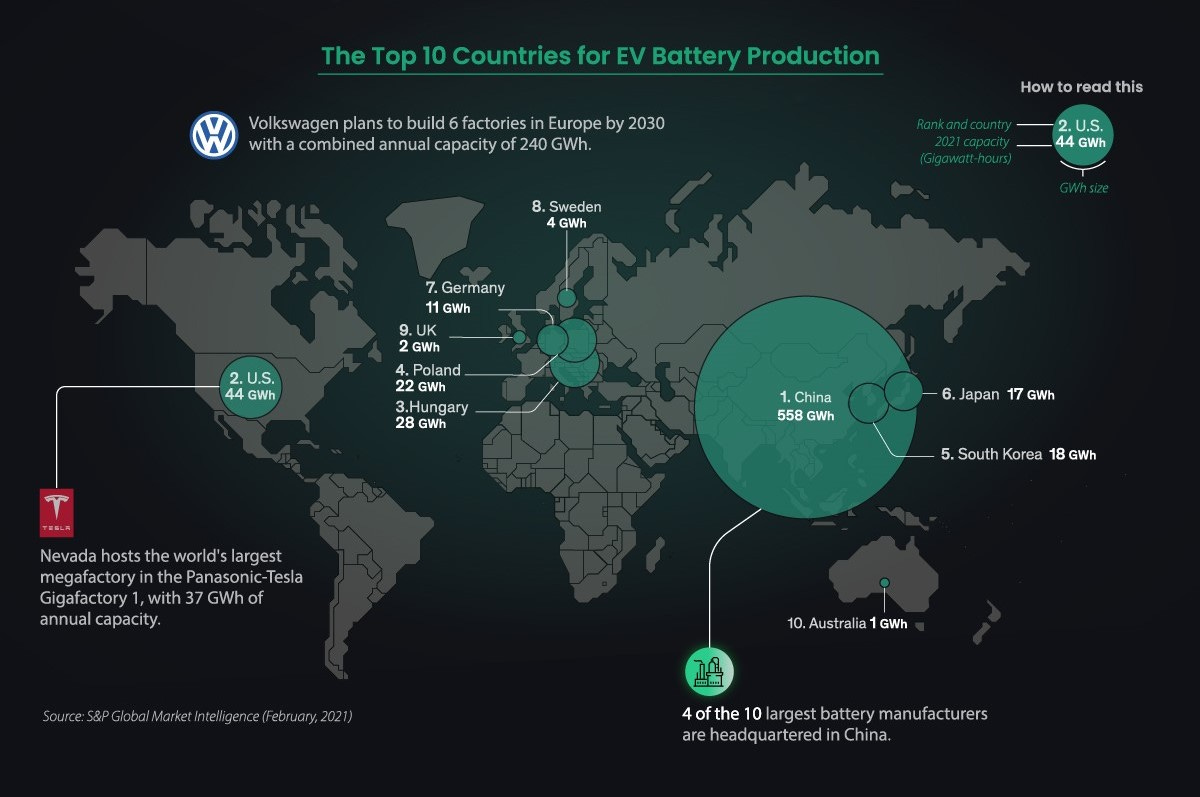

Currently, China produces about 80% of all lithium-ion battery cells. To keep up with China, the UK, EU, and US are all in a global battery arms race to acquire market share quickly.

Companies are racing to secure and strengthen their positions in the battery supply chain, from mineral extraction and processing to battery and EV manufacturing. This sector is seeing a move towards vertical integration, with companies wanting to control crucial components of the supply chain. These include plants by major battery cell manufacturers, including LG Chem, SK Innovation, Panasonic, BYD, Samsung SDI and others, as well as emerging and startup players across the lithium-ion battery supply chain. As vehicle manufacturers scale up their plans for electric vehicles, many including Tesla, Volkswagen Group, GM, Ford, Daimler, and others are also investing and expanding their gigafactory footprints, whether through joint ventures with battery cell manufacturers, or through eventual in-house battery cell manufacturing.

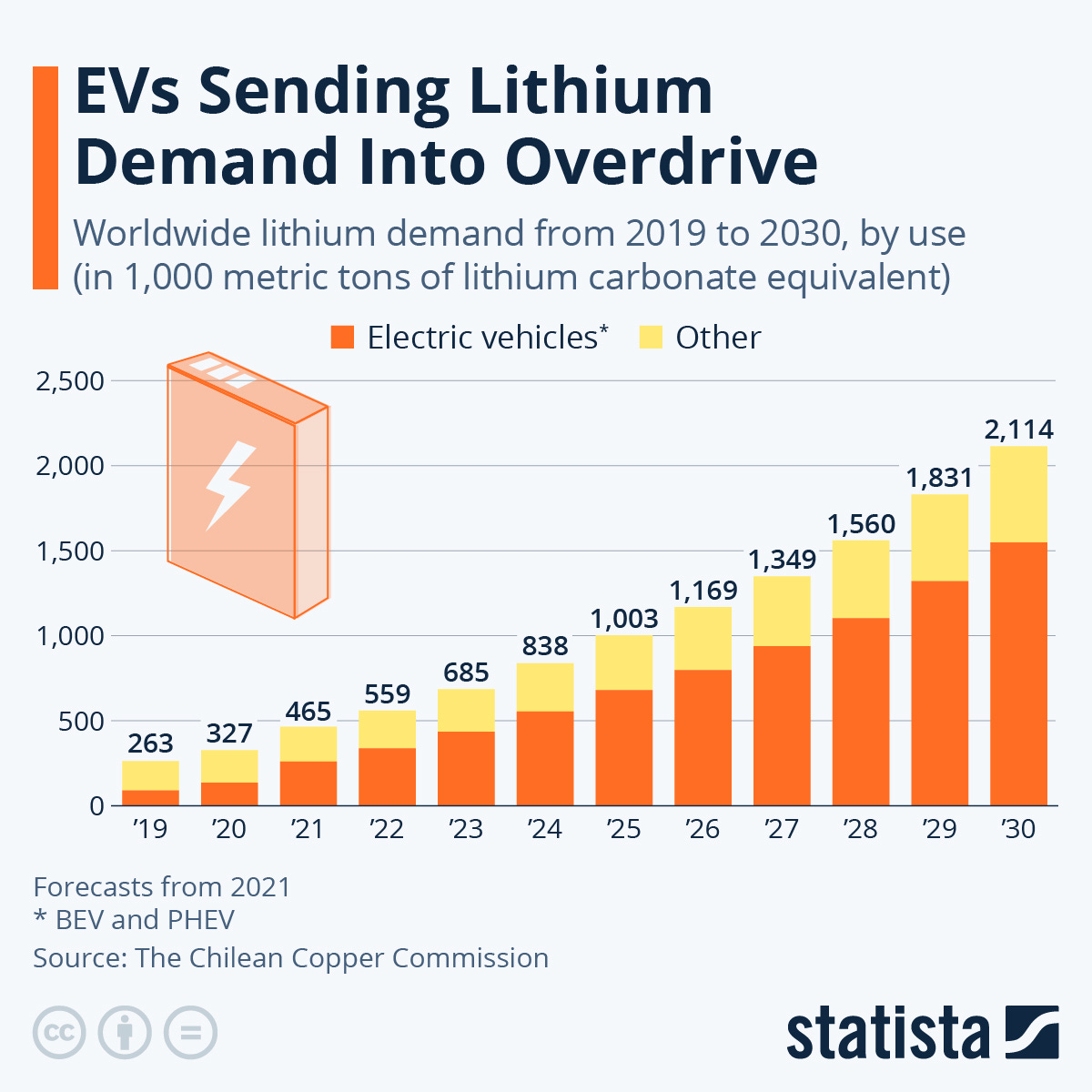

All these batteries need Lithium and according to IEA forecasts, between 2020 and 2040, Lithium demand is expected to increase by a staggering 42X. With newer EV models coming soon with better battery performance, which means higher energy density and range, demand for Lithium is only likely to go up.

All roads lead to Lithium miners

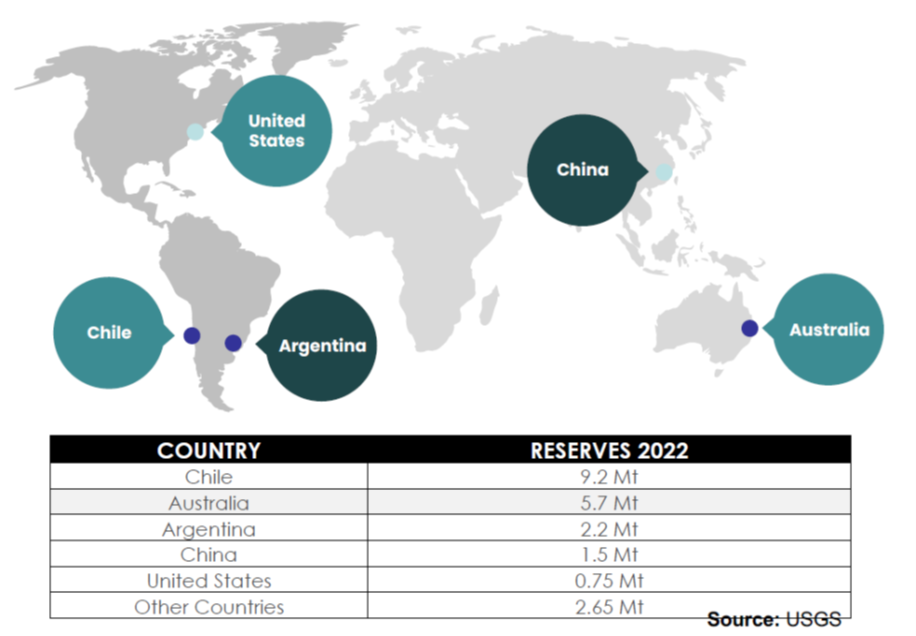

The proven global lithium reserves are estimated at 22 Mt, while the identified global lithium resources have increased substantially to 89 Mt. Many reserves and resources are found in countries which have not yet commercialized its production.

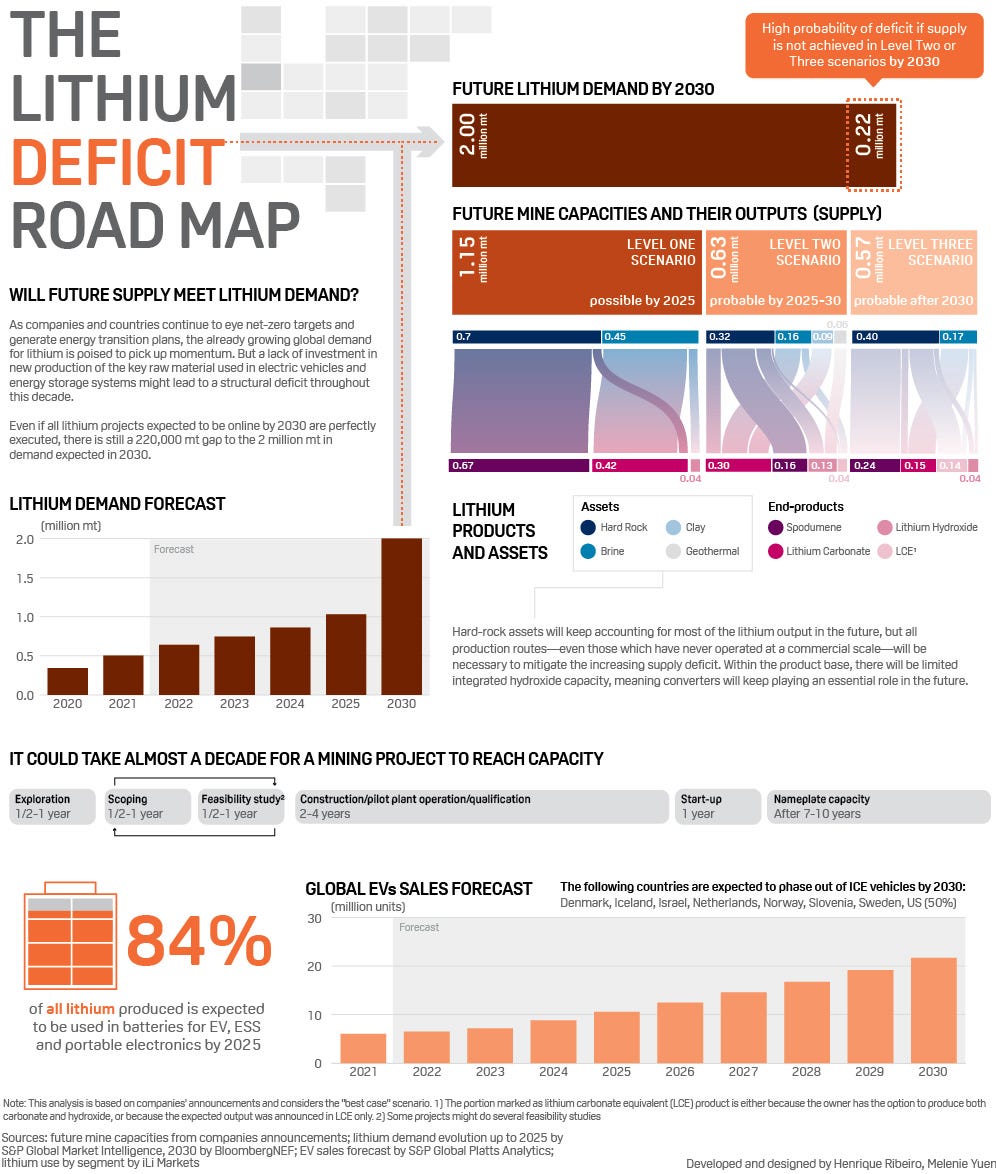

There are two main types of lithium resources: spodumene and brine. While each accounts for about half of lithium deposits globally, it is all about the availability of battery grade lithium products, which can pose a large risk. Lithium saw a bear market during 2018-2020 and as a result, investments into Lithium mining saw a steep fall. In early 2018, a lot of new spodumene ore capacity from previous investments showed up in supply, in anticipation to an expected EV boom that didn't materialize till the end of 2020. This oversupply crashed prices and halted investments. With the surge in demand for EV’s post 2021, suppliers of Lithium have been accelerating their expansion. Although the battery industry has been investing significantly in downstream battery capacity, Lithium mining got less funding than required and as a result, even faster investments into mining capacity could still cause structural deficit in the coming years.

According to IRENA:

· Investment in lithium production needs to be increased. Current and planned projects are expected to come online to meet demand between now and 2025, but there is a high probability of a tight lithium supply between 2025 and 2030. Lithium supply can likely switch to deficit if additional projects are not added to the pipeline to meet 2030 demand.

· Lithium production must quadruple between 2020 and 2030 to meet growing demand, from 0.345 Mt in 2020 to 2 Mt in 2030. It is critical to ramp up exploration and production now, considering the lengthy timeline for lithium mining projects to meet increasing demand.

· It is necessary to invest in technological advancements to reach previously inaccessible resources, improve recovery rates and speed. 90% of exploration permits in 2021 were in China, Chile, and Australia, it is important to expand mining to other countries.

Its China all the way

While US, EU and other countries have been talking about clean energy, a move to electric mobility, increasing battery production and securing critical raw materials, much of it is has been on paper. But quietly over the past two decades, China has already staked out the EV industry and its value chains. China has come to dominate the lithium battery market from end to end and there is little realistic hope of US, EU or any other country catching up. With 93 giga-factories inside its borders and nearly 900 gigawatt-hours of manufacturing capacity or 77% of the global total, China is home to six of the world’s 10 biggest battery makers. 101 of the 136 battery manufacturing plants scheduled to enter operation by 2030 will be based in China.

“Control oil and you control nations,” Henry Kissinger once said. Today, China seems to believe in, “Control lithium and you control nations”. Behind China’s battery dominance is its vertical integration across the rest of the EV supply chain, from mining the metals to producing the EVs.

Though China does not have anything close to the world’s largest lithium reserves, the country has come to dominate the global lithium battery supply chain. Nearly 80% of Lithium deposits are in four countries: South American lithium triangle of Argentina, Bolivia and Chile, and Australia. China holds less than 8% of the reserves, but is the world’s largest importer, refiner, and consumer of lithium. It buys 70 % of lithium compounds and supplies 70% of lithium production to domestic battery makers.

· State backed Chinese mining consortiums control about 80% of the global raw lithium production and approximately 65% of the world’s lithium processing and refining processes. China is actively working to further consolidate its dominant position with 6.4 million tons of lithium supplies being secured by Chinese companies around the world in 2021.

· Chinese mining companies are stepping up efforts to increase their access to lithium deposits in a bid to meet the growing global demand for batteries. The likes of Ganfeng, Suzhou TA&A, Sinomine and BYD, have all taken steps to acquire lithium mining rights in South America and Africa.

· Ganfeng Lithium has acquired Argentina mining group Lithea, and the deal gives Ganfeng rights to two salt lake brines in Argentina, Pozuelos lithium salt lake and Pastos Grandes lithium salt lake. Ganfeng has gradually increased its lithium assets in Argentina. It has started construction on a $600m lithium chloride production plant in Salta and is aiming to reach annual production output of 20,000 tonnes of raw lithium. Ganfeng also owns a full stake of the Mariana project and 47% of the Cauchari-Olaroz project in Argentina.

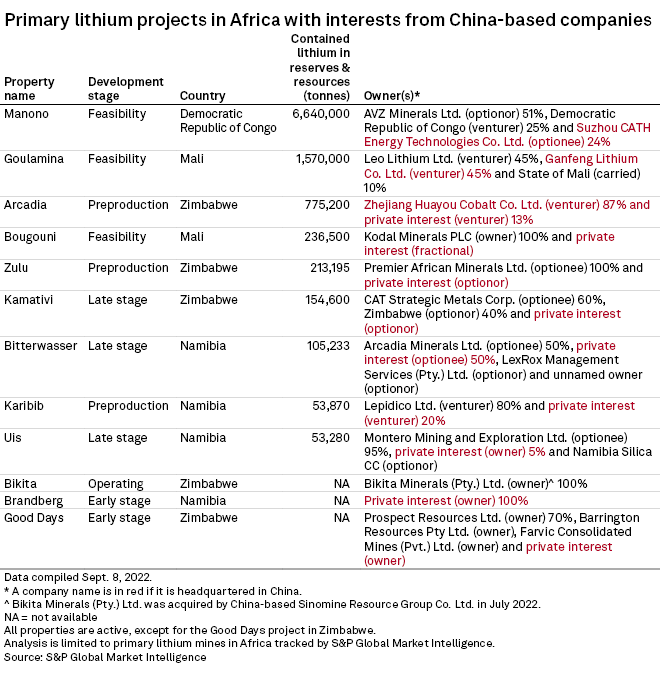

Beyond South America, China is also winning the race for Africa’s Lithium. In March 2023, Africa’s first Chinese-owned lithium concentrate plant started trial production at Arcadia, in Zimbabwe, a mine bought by Huayou Cobalt in 2021 for $422mn, part of a recent wave of Chinese lithium deals in the country.

Africa can play a critical role in easing Lithium supplies globally. African countries led by Zimbabwe have significant proven resources and can rapidly bring lithium projects online this decade. Commodity trading giant Trafigura predicts Africa could supply a fifth of the world’s lithium in 2030 and China sees it as possible rising star for lithium.

While US and EU have been busy talking partnerships with Africa for securing critical minerals, Chinese companies and investors have been busy buying up African mines to produce these minerals. In 2022, Chinese mining companies Tsingshan, China Nonferrous and Huayou Cobalt invested nearly $1.5 billion in Zimbabwe and in the same year, Sinomine Resource Group announced its plans to expand its current production at the Bikita mine by investing $200 million into building a new lithium plant.

Geopolitics of Lithium – Battle lines are drawn.

China has taken a decisive lead in Lithium and Battery production. While US, EU, Australia, and other countries try to play catch up, redrawing the geopolitical map of Lithium will be contentious, acrimonious, and harder. While oil-based geopolitics had placed the Middle East and the western world led by US at the center, the current structure of the Lithium industry places South America and Asia at its heart, with China leading the way. China’s leading position has been a work in progress since the turn of the millennium as it decided to focus on Electric Vehicles and the associated supply chain, and its strategy has been a resounding success.

In March 2022, the International Energy Agency (IEA) launched a voluntary critical minerals security program which includes stockpiling, recycling, and resilient and transparent supply chain mechanisms. Considering that IEA forecasts lithium demand growth to be the strongest of all critical minerals, rising over 40 times by 2040, Lithium features prominently. Unfortunately, many Lithium producing countries are not members of IEA, such as Bolivia with vast Lithium deposits. Major producers like Argentina and China are just association countries and Chile, the world’s second largest lithium producer is seeking membership. This means the IEA would need to overhaul its membership to include countries at the center of the Lithium supply chain to be relevant in the new energy scenario.

China might grab this opportunity to create a consortium of the world’s largest lithium-producing nations to balance market needs and ensure the security of supply chains, just as the Organization for Petroleum Exporting Nations (OPEC) has done for oil. These supply chains will include refining, component manufacturing, cell manufacturing and recycling, on similar lines to what China has already achieved.

What are the implications of this race to build-out of lithium-ion battery capacity globally? While China has understood this fundamental shift for a number of the world’s most important industries early and has taken a lead, EU and US have just realized the implications. So far China’s battery manufacturing ambitions have been limited to its own border. But as it tries to expand beyond, this could become a Geopolitical hot potato. Chinese battery manufacturers have a captive demand at home and will not be reliant on Western automakers. But companies such as Ford and Mercedes are and will be dependent on Chinese companies such as CATL for batteries and this can cause significant angst politically in US and EU. While EU has a planned for battery manufacturing capacity of 700 GWh in the coming years, it has no presence in Lithium refining and processing and will be dependent on China for foreseeable future.

While many EU countries plan move to 100% electric mobility by 2035, they are also ratcheting up the regulatory pressure. They have introduced ‘Rules of Origin’, which mandates battery and car manufacturers to localize supply chains, forcing them to source precursor battery materials from UK or EU suppliers from 2024 or face punitive tariffs. A similar Batteries Regulation is in works, which means many mineral refineries and their downstream customers must be compliant with EU standards.

For those who have seen Geopolitics of petroleum playout in 20th century, this might seem like a familiar script. What we are seeing is reordering of supply chains and geopolitics of large and important industries globally and the true nature of it will playout in the coming decade.

Welcome to the Li-Ion Economy 😊

…… and For Savvy Investors

In an evolving and fast changing industry like Electric Mobility and the Battery Economy, it pays to understand the value chain and identify the opportunities. I have mentioned about Ganfeng Lithium briefly above. According to Jenga Investments, Global Outperformers Report:

“Ganfeng Lithium, a market leader in lithium mining, compounded its revenue and operating profits by 40% and 59%, respectively, and returned 2,749% over a decade till 2022. Value investors primarily focused on relative multiples would have found Ganfeng Lithium very expensive. Its EV/EBIT rarely fell below 40x (only during 2018-2019, when lithium prices fell by half). Growth investors would have said its earnings are too dependent on the cyclical lithium price, while quality investors would have screened out all materials industry players.”