Investing for the Future – A New Geoeconomic Reality

“What is changing globally?” This is a question I have been asking myself the past couple years since COVID. We are witnessing events that have not been experienced for over a generation. News is dominated by Geopolitical tensions, Inflation, Supply Chain disruptions and Populist political narratives. We can feel the palpable tension and nervousness and global economy has been volatile and precarious. How do we make sense of this? The past decade has seen its share of crises starting with GFC in 2008. Arab Spring, crisis in Crimea, Brexit and Trump were probably portending to something bigger. Covid and now Russian invasion of Ukraine seem to have pushed things into a new territory and we are seeing a new era of complexity, which will be dominated by Geopolitics and Geoeconomics. How do we understand this change?

The picture above, the “Fall of Berlin Wall” in November 1989, was an event that ushered in era without precedent in history. This was an era that defined may of our lives. This was a seminal moment that united Europe and the world under the umbrella of US leadership, ushering in the era of Unipolar World for close to three decades. Six months after the fall of the wall, Saddam Hussein invaded Kuwait and the response lead by United States was swift and Brutal. A united Europe and rest of the world backed and funded the response, watched on the side-lines by a fractured and decayed Soviet Union in its death throngs. This was followed by, dissolution of Soviet Union, democracy movements sweeping Eastern Europe and elsewhere, China entering the market economy and The Maastricht Treaty being signed in 1992, paving the way for a united Europe.

This ushered in an “Era of the Markets”, that was dominated by

· American defined neo-liberal order

· Financialization and Unfettered capital flows

· Washington Consensus

· Supply chain diversification.

This is an era that is familiar to most of us, defined by the rise of technology and connectivity, rise of democracy and the rise of Asia in a US led world order.

This picture above sums up the change and a very different story, we are experiencing. It marks end to the disastrous two-decade misadventure of US in Afghanistan. The hasty and haphazard withdrawal in August 2021, with civilians trying to cling to the flights taking-off, in a desperate hope of survival and the fear of what was to come under Taliban. Ironic that, six months after this event, Putin’s Russia invades Ukraine and in contrast to 1990, the response from a weary US and disunited Europe was patchy at best, despite the talk. US was reluctant to put boots on the ground and led the response with Sanctions followed by a few Western European countries, but the telling aspect was the fact that, only 39 countries globally implemented those sanctions.

Welcome to the “Era of Complexity” and a “Multipolar World”. What we are witnessing is the birth of a more contested world, with no clear leader or ideology to drive it. It will be dominated by forces that had taken a back seat for over a century. So, what will the world going forward look like and what does it mean for us?

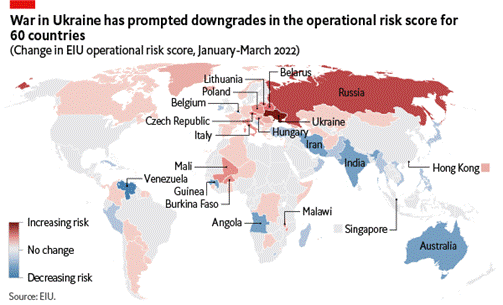

A few weeks after the Ukrainian war started, Economist Intelligence Unit published an analysis, where they downgraded the operational risk score for 60 countries around the globe, as a result of war’s impact

One of the main reasoning behind the analysis is the intensification of geopolitical tensions centred in Europe, which would have a worldwide impact from commodity prices and economic and financial disruption to security.

Similarly, Both Blackrock and Lloyds have been identifying Geopolitical Risks as a major aspect in their analyses. They should know it better, given the amount of money at stake, if something cracks. According to them, Geopolitics has become dominant risk for markets, with direct and likely long-lasting impacts. A new geopolitical world order is coming into view. The Ukraine war and escalating U.S.-China competition have deepened fragmentation and the emergence of competing geopolitical blocs.

One of the key secular trends prominent in the new regime will be, Geopolitics and Geoeconomics of Supply and the brutal trade-offs that will be involved. This will be seen playing out across various domains of

· Trade and Investment

· Resources and Energy

· Technology

· Capital and Currencies

These structural forces will interact and intersect at various levels and the emerging dynamics will impact individuals and society, states, and the international system. Let us dive deeper to understand these forces that would exert a huge influence in the future.

The irony is not lost, when you consider that, it was the fall of Soviet Union that set the stage for a Unipolar World under US Hegemony, and it is the Russian invasion of Ukraine, that brings the era to an end.

Revenge of Geography - Return of Geopolitics

There is an old joke in India that I remember every time someone downplays Geography or Geopolitics. It goes something like this:

· Indian: Thank you God! You have provided my country with everything. Great fertile regions and rivers, amazing culture, wonderful and friendly people, intelligence, and wisdom.

· God: Wait till you see who I have given you as neighbours

Geography might not be destiny, but it influences a county’s actions and poses limitations and constraints on what can be done. Over millennia, from the invasion of Alexander, Ghazni and Timur to present day tensions with Pakistan, the North-Western frontier and access defined the history of Indian heartland. It is the same geography that limited European access to India, made them find the sea route to Peninsular India. Geography exerts a huge influence.

· America exemplifies the advantages of Geography. A country, the size of a continent, rich in natural resources, bound on both sides by vast oceans, a natural obstacle from invasions and bordered by countries that are not a physical threat, they have the luxury of pursuing their manifest destiny and be able to project power across the globe.

· It was their geographic position at the outer edge of European land mass and being cut-off from Eurasian heartland, that made Portugal, Spain and England seek maritime routes and create a Maritime Empire.

· Russia’s geography drives its historic memory and psychology. Surrounded by plains to both East and West that made outside invasion a part of life and lack of access to warm water ports forced them to build a land-based empire stretching from Carpathians to Siberia.

Geography then, is the underlying driver of the national policies that define economics, trade, and investments. It shapes how nations interact with others and shapes their interests. shape markets. Despite the rise of communication technologies and digital networks, we have not transcended geography. People might like to idealize a “World is Flat” concept, but the reality is we live in a world divided by mountains, rivers, seas, and the borders, literal and figurative that define what happens globally.

“This is geopolitics boiled down to its essence: the state will always pursue survival and power within the limits of geography, and most of its behavior will be driven by these basic instincts, whether conscious or not”. (Lykeion)

Geopolitics as an idea was a product of the last multipolar world of late 19th century. Multipolar world has been the norm for most of our history till early 20th Century and most of the last century we lived in a Bipolar world. The past 30 years have been an historic anomaly, a period of Unipolar moment. While Geopolitics were important in a US driven world, they were more at the periphery or subsumed by the US led global order. The interests and goals of most countries converged trying to benefit from the advantages of being a part of the globalized world and share the benefits of a unified system. Countries, Companies, and Investors suddenly had no reason to worry about Geopolitics as they were predictable with the US as the arbiter of the outcome. No country derived the most out of this than China, between 1990 to 2020

The GFC of 2008 was a fulcrum that probably punctured the post-cold-war optimism and inexorable rise of Globalization. Arab Spring, Russian invasion of Crimea in 2014, Brexit and Election of Trump in 2016 and US-China trade war were signals that all was not well, but more or less status-quo remained till the advent of Covid-19. Now with the Russian invasion of Ukraine, it is obvious that the world has changed.

China wants to regain its rightful place as the “Middle Kingdon”. The United States, torn my dysfunctional internal politics and rise of populism, failed military adventures in Iraq and Afghanistan has lost the presumed moral supremacy to preach its values. Extreme global inequality, a by-product of globalization and financialization has reversed public opinion about globalization and a clamour for national self-sufficiency is on the rise.

We are seeing the beginning of an era of great power competition. US continues to be influential economically and militarily, but countries of wary of it. Russia is making its own moves and wants to reclaim its lost glory. China is preparing for war and an empire. Germany and Japan are arming again. India, Brazil, Saudi Arabia, Turkey, and other emerging economies are more concerned about growing their economies and identifying their spheres of influence.

Welcome to a truly multipolar world:

· “A New Great Game” in the Eurasian heartland has begun. This time instead of territorial competition, the contest will be for access to resources, connectivity, cheap labour, and energy. This is what Robert Kaplan calls, “The Return of the Marco Polo World”.

· Given the projections for exponential growth of Electric Vehicles, Renewable Energy and Computation Technologies, we will see an intensification of scramble for resources from Africa and Latin America.

· Multiple Rival spheres of influence will emerge. The existing US and China nexus and networks will witness an acceleration of “decoupling”. Trade issues will become national security issues and Regional Powers will throw their weight.

· Securing supply chains and access to resources will increasingly become a national security issue in addition to their economic importance. There will be an increase in Regional Trade Agreements and spawn a host of regional economic networks that would be even more interconnected. But globally there will be less interaction between countries in rival networks.

That is why geopolitics is important today – not just because it seems like the world has gone haywire, but because geopolitics was designed precisely to analyze and predict the kind of macro-environment that is beginning to emerge. (Lykeion)

Geoeconomics, Reglobalization and Decoupling

· Russian gas accounts for 25% of EU energy needs. Russia cuts off gas supplies, sending Europe scrambling for alternate supplies.

· Turkey restricts passage of ships carrying critical grain exports from Ukraine through Bosphorus.

· China signs a $60 Billion, 27-year LNG deal with Qatar, the largest deal of its kind.

· US passes a CHIPS act, restricting supply of critical semiconductor equipment and materials to China.

· Israel and Lebanon sign a border demarcation deal, that would help both countries to explore natural gas in their territorial waters.

· China urges the GCC countries to trade petroleum in Shanghai exchange, denominated in Renminbi.

· Indonesia is considering setting-up a OPEC like cartel for Nickel and other key Battery metals.

What is the common thread, running through these news items from the recent past? It is Geoeconomics at play and we should expect to see more of this in the future.

Geoeconomics is broadly the interplay between Geopolitics, Economics, and Investments. It is the use of economic instruments to promote and defend national interests, that in turn would produce beneficial geopolitical results. They are tightly interlinked with other nations economic actions on a country’s geopolitical goals.

Recent years have seen an increase in the use of Geoeconomics tools by countries, resulting in brittleness of global value and supply chains. Risk of disruptions to critical economic flows is real, challenging economic resilience. In a volatile global Geopolitical environment, governments intervene more frequently. The texture of bilateral and multilateral economic cooperation seems to be changing fundamentally. This Geoeconomic uncertainty affects corporate decision making and business models, as has been the case with Semiconductors, and will come to be seen in other sectors. There would be restrictions on exporting and importing critical components of the value chain, prohibit cooperation and research for national security reasons and block investments in certain countries.

In the coming decade(s), Geoeconomics as a fundamental force of the Global Economy will be driven by three crucial factors:

· Weaponization of economic relations.

· Securitization of economic relations.

· Balkanization of the global economy.

Before I delve into specific aspects of Geoeconomics, let us try to understand this whole debate about Deglobalization. What exactly is happening there?

Deglobalization or Reglobalization?

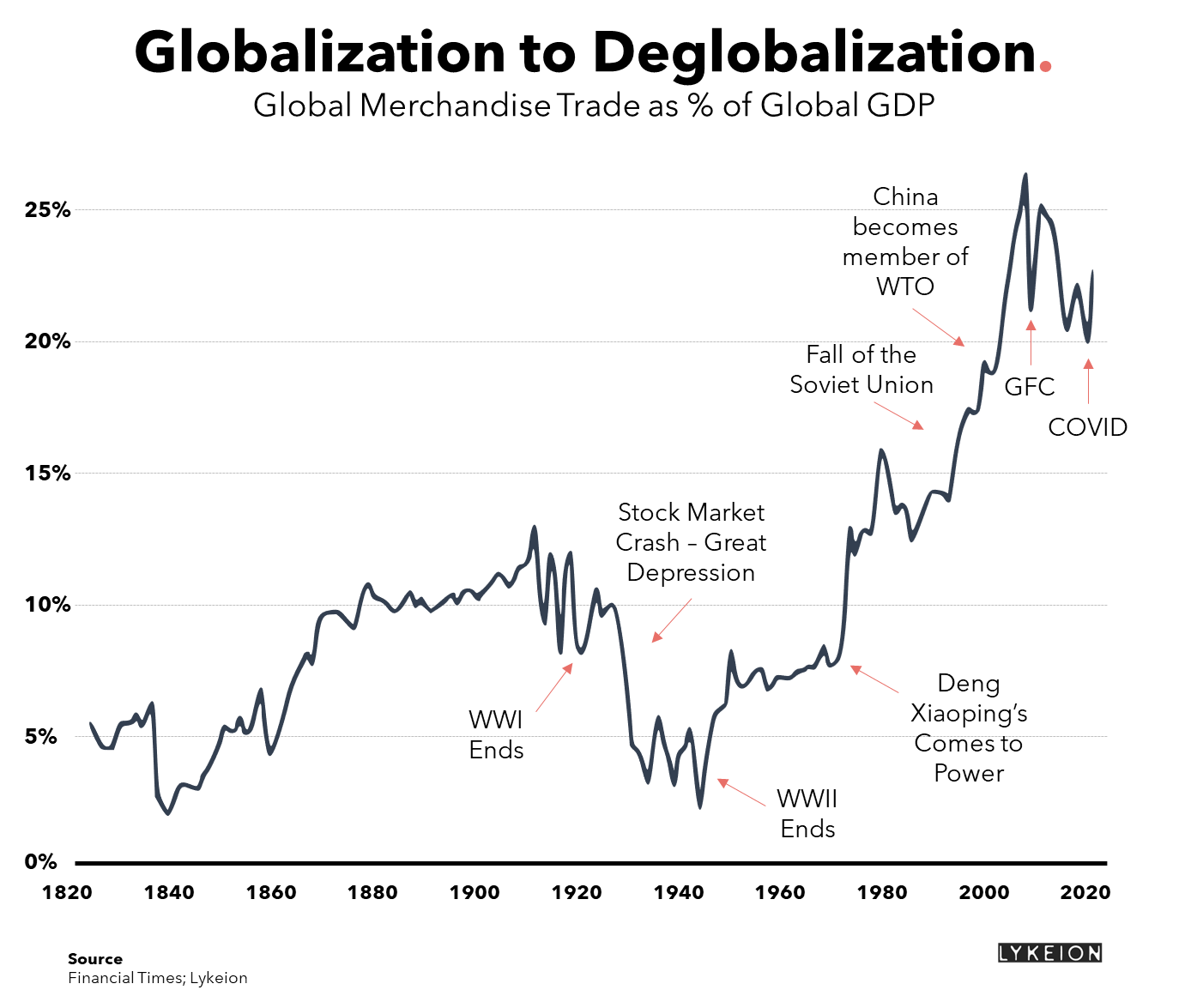

Recently, I came across this graphic. A lot has been written about Deglobalization and the hyped-up consensus seems to be, we are headed for autarky globally.

Despite all the noise, the reality is, rising political tensions are changing globalization, not ending it. We still live in an interdependent world and Autarky is not a practical goal for any country. As they say, the devil is in the details and the graphic below sums it up.

According to a recent McKinsey report on Global Flows: “Every region imports more than 25 percent of at least one important type of resource or manufactured good that it needs, and often much more. Latin America, Sub-Saharan Africa, and Eastern Europe and Central Asia are net importers of manufactured goods; they import more than 50 percent of the electronics they need. The European Union and Asia–Pacific import more than 50 percent and 25 percent, respectively, of their energy resources. North America has fewer areas of very high dependency but relies on imports of both resources, notably minerals, and manufactured goods.

What we are seeing is “Reglobalization” and the rise of “Regionalization”, not Deglobalization. Global value chains are evolving, and reconfiguring driven by new Geoeconomic forces: Resilience, National Economic Priorities. Stakeholder Interests, Demand and Supply.

· Between 1995 and 2008, the direction of change was almost uniformly toward less concentration and more interregional trade as truly global value chains were unleashed by trade liberalization and technological progress.

· After around 2008, patterns of trade flows diverged. Global value chains accounting for around 40 percent of trade, including energy resources, electric equipment, and pharmaceuticals, reversed course, becoming more concentrated.

This trend towards regionalization and concentration is best understood looking at data. Regional Trade Agreements (RTAs) show how globalization is changing, not dying

From the data, it is also clear that, since 2005, majority of RTA’s have been for services trade, underlining the fact that global trade is not declining, but moving from Goods to Services. While global trade has stabilized, flows linked to knowledge and knowhow are driving global integration. Growth in global flows is now being driven by intangibles, services, and talent. They have picked up the baton from goods trade whose growth as a share of the global economy stabilized around 2008 after 30 years of rapid expansion. Flows of services, international students, and intellectual property grew about twice as fast as goods flows in 2010–19 while data flows grew at nearly 50 percent annually.

How will this trend of Concentration and Regionalization play out going forward?

Geoeconomics of Critical Value Chains

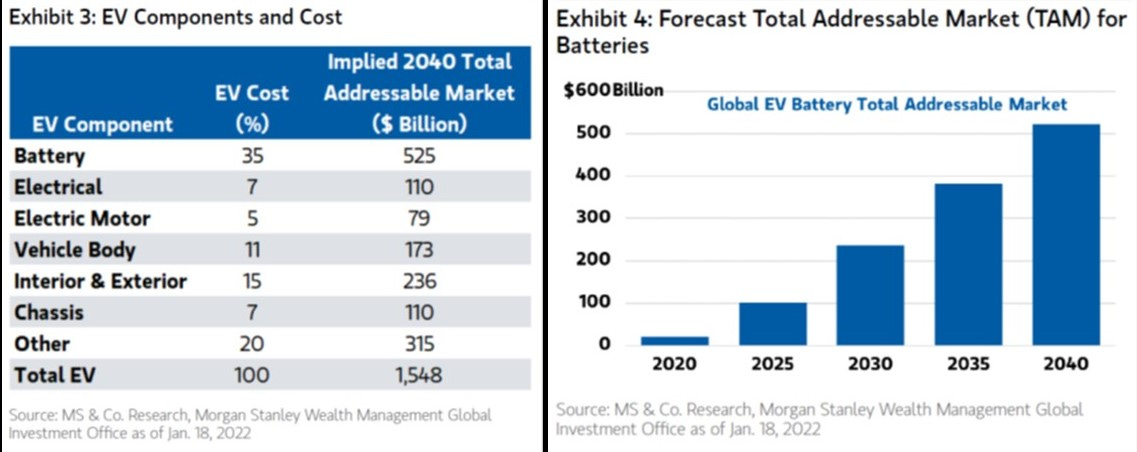

EV Batteries

What is driving this impulse from countries like Indonesia to create a cartel for Battery materials? Let us understand this through some data.

Globally Electric Vehicle sales are expected to grow rapidly. According to a recent Morgan Stanley report

Batteries are the most important part of an electric vehicle, and their demand is likely to be exponential

The race for Electric Vehicles is leading to companies investing heavily in Battery manufacturing. Every big name across the Auto Industry in the USA, Europe and China has announced plans to significantly increase their battery manufacturing capacity. The graphic below shows the current and future plans for battery manufacturing across the globe in 2021.

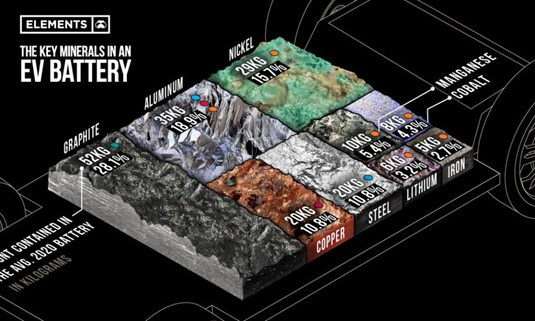

Despite all the noise about, EV being green and Green Transition, manufacturing batteries is mineral intensive. The cells in the average battery with a 60 kilowatt-hour (kWh) capacity, the same size that’s used in a Chevy Bolt, contained roughly 185 kilograms of minerals. This figure excludes materials in the electrolyte, binder, separator, and battery pack casing. For example, NMC batteries, which accounted for 72% of batteries used in EVs in 2020 (excluding China), have a cathode composed of nickel, manganese, and cobalt along with lithium.

A few countries dominate the EV Battery value chain. Lithium is mostly available in the three countries of lithium Triangle, Argentia, Chile and Bolivia, followed by Australia and Zimbabwe. World’s largest deposits of Cobalt are found in DRC and Indonesia is the largest producer of Nickel.

The race is on to secure long-tern supplies by countries and companies. We are moving from “Shortage Economy to Fear Economy”. The past couple of years, initially Covid and then followed by Ukrainian war have reinforced globally the fear of shortages. The general feeling is that the shortages are here to stay given the febrile state of the global economy and this will have an impact on all the sectors. The FOMO on critical supplies that will stall an economy is driving nations and companies with a global footprint to devise strategies that secure their supply chains.

We will see this playing out in other sectors too.

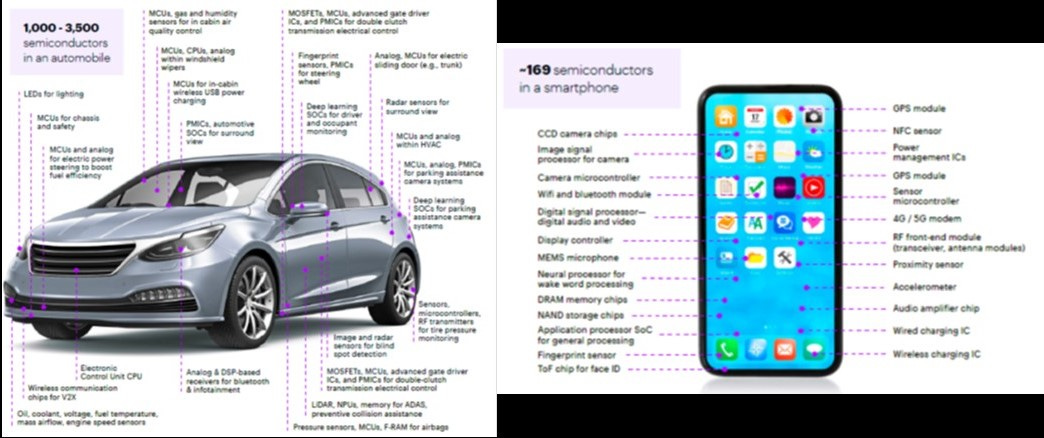

Semiconductors

If there was one news that dominated the global news in 2020 and 2021, it was Semiconductor Shortage. While every major industry got impacted, the worst hit was the Global Auto Industry. Semiconductors are the life blood of our interconnected economy. Let us look at two most used products daily, Cars and Smart Phones and their dependency on Semiconductors

The criticality of Semiconductors is not limited to Communication and Auto. They are the backbone of every industry today.

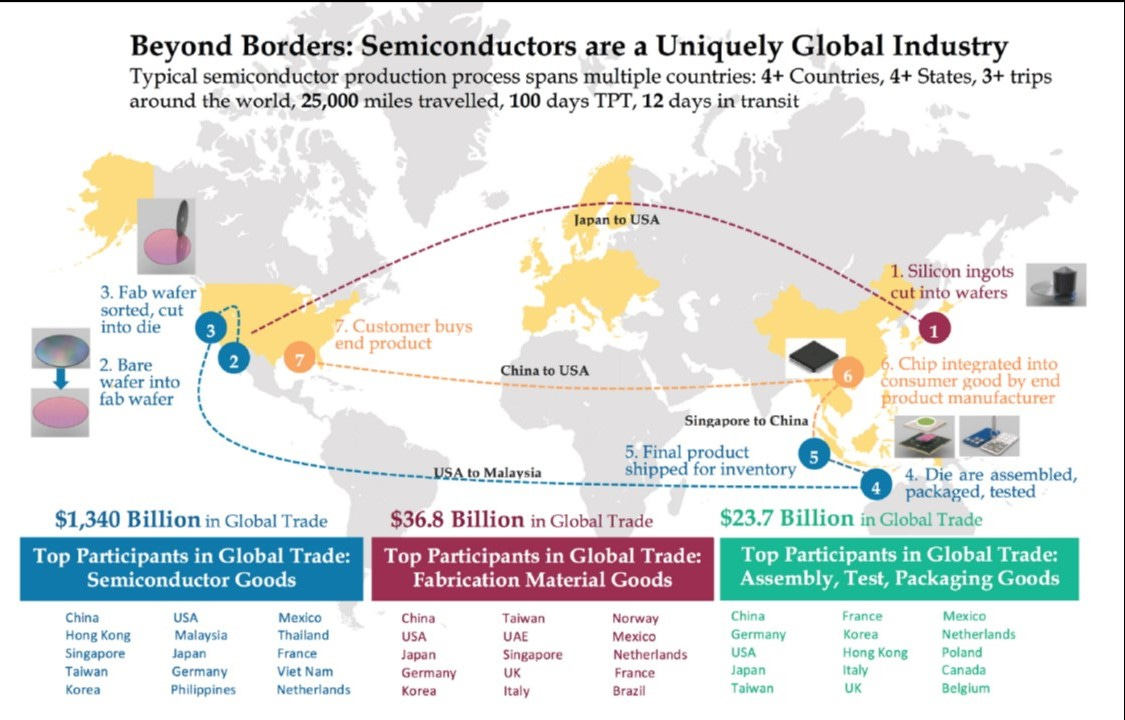

Globally advanced computer chips drive economic, scientific, and military capabilities. Complex supply chains underpin production of these chips. The half-trillion-dollar semiconductor supply chain4 is one of the world’s most complex. The production of a single computer chip often requires more than 1,000 steps passing through international borders 70 or more times before reaching an end customer.

Combined, the criticality of semiconductors plus the fragility of supply chains has pushed countries to consider various options to reduce dependence on countries like China. In August 20. 22 Joe Biden signed a Chips act, which represents the biggest US foray into industrial policy in 50 years. What forces pushed semiconductors to the apex of US industrial policy?

· A fear of Chinese technological ascendency in general and semiconductors in particular that added to the acute post-pandemic shortage of chips for making everything from automobiles to laptops. US also wants to avoid the vulnerability of advanced chips produced in Taiwan and South Korea Chinese attack or blockade

· The US semiconductor production dropped from 37 percent of the global total in 2000 to 12 percent in 2021. While they have made reversing this a priority, Chinese moves to invest heavily into Chips is a cause of serious concern. US wants to deny China and Russia access to advanced chips and chip-making machinery.

Following-up on the CHIPS Act, The United States also sanctioned the Chinese Semiconductor Sector. This was classic Geoeconomics at play, to impede China being self-sufficient in the area of Semiconductors. Semiconductors are a strategic vulnerability for China considering the importance of advanced chips required for future, AI, 5G and Military applications. China has been stepping up its push to master advanced semiconductor manufacturing. Through its massive National IC Investment Fund, established in 2014 and recapitalized in 2019, and other regional and local funds, China has earmarked funding in excess of $200 billion, more than the inflation-adjusted cost of the US Cold War-era Apollo moon shot—to move China up the manufacturing curve. Yet it has so far achieved limited results. China’s leading fabrication company, Semiconductor Manufacturing International Corporation (SMIC), remains three to five years behind industry leaders Intel, Samsung, and TSMC.

While Semiconductor industry is at the forefront of Geoeconomics of Technology, the same process seems to be repeating across the entire technology spectrum, be it AI or 5G. New technologies were primarily viewed from an economic and commercial standpoint. But it has now increasingly become a foreign and security policy issue. Emerging technologies in particular have become both an object and a driver of international cooperation and competition, shaping the global landscape in different and sometimes unexpected ways. High tech has come to signify high politics too. Today, digital and tech advancements are geopolitical issues of the highest order, with the second wave of digital innovations being at the heart of economic and technological supremacy.

Geoeconomics and Secondary Economics

As I had asked earlier, What is the common denominator between Qatar’s LNG contract with China, Turkey flexing its muscles in the region or Saudi Arabia's oil production against the wishes of the United States and also wanting to join BRICS bloc? All these are pointers to an underlying phenomenon: many countries that are often categorised as second tier geopolitically are increasingly becoming independent geoeconomically. They are no more inclined to follow the demands of more powerful countries like USA or China and this will have a great impact on the global economy. This autonomy is being displayed not only by countries like India, Turkey, the Gulf countries, and Brazil, but Kazakhstan, Azerbaijan, Vietnam and Malaysia, as well. Add to this the recent visit by German Chancellor Scholz’s trip to China or the Arabian Peninsula’s relationship with Russia.

A few years ago, I came across a map from US Geological Survey about the different countries that have minerals, where US import dependency is greater than 50%.

This map makes intuitive sense in today’s world. If US is dependent on these countries for critical minerals, then so most other countries. Let us not forget, Energy Transition, be it Energy Storage, renewable Energy or Electric Vehicles along with all the computing power required for advances in communication and computing, are mineral intensive.

With this kind of global dependence on critical components of value chains, Secondary Economies and possibly even some Tertiary economies are very likely to flex their muscles in a Multipolar World and a Fractured Global Order.

· Their aim will be to boost their power and independence amidst a global imbalance. Being part of critical value chains can be a source of power. Both Climate change and Energy transition can shift comparative advantages. Globally distributed value chains defy the logic of Big and Small countries. This further promotes trade leverage and policy autonomy for secondary economies.

· The rivalry between the world’s two largest economies, US and China also plays to their advantage. Recently we have seen Saudi’s play-off interests of both the countries. In Asia and elsewhere countries are taking advantage of this geopolitical environment to draw investors from both US and China.

· Countries like Turkey and Kazakhstan will derive economic advantage from their geopolitical status of “pivot state”. Similarly, Grain-producing countries in Latin America have taken the opportunity to rearrange their exports. India has been particularly active in the ramp-up of South-South flows by racking up new free-trade agreements.

· There is a very high possibility that we are headed towards a world run by cartels like OPEC, as countries become aware of their new power. Indonesia took the first step with its proposal at the G20 summit to form a nickel production bloc. A world run by cartels will be far more influenced by second-tier powers than by superpowers or major importers.

Understanding Decoupling

While I have focussed more on Geoeconomics of value Chains, one important aspect to understand would be, “Decoupling”. The past few years, since the election of Trump, news bytes about US-China decoupling have garnered enough attention. But this phenomenon may play out with many other countries like Japan, Korea, India, and members of EU might pursue their own paths.

Decoupling is not a monolith and will play out across different areas in different ways. The three most visible areas will be:

· Macro Decoupling – Financial and Currency

· Trade Decoupling – Value Chains and Supply Chains

· Technological Decoupling – R&D and Standards

So, what is driving it? According to Rhodium Group,

“Decoupling dynamics are being driven by myriad factors. Many countries around the world are reviewing their levels of dependence on certain economies either as a result of shifting geopolitical allegiances or to mitigate supply-chain risks, such as those created by the global COVID-19 pandemic. However, at the root of decoupling are fundamental changes in how the world’s two largest economies, US and China now see themselves in relation to each other and the rest of the world”.

· China is flexing its muscles and wants to regain its place in the world. It no longer is reticent or ambiguous about the nature of Chinese system but touts the advantages and differentness of it.

· The US defines China as its strategic competitor and considers it to be a threat to the rules-based world order it promulgated post the WWII. It blames China as a being unaccountable and lacking transparency and taking advantage of its growing prowess to circumvent globally accepted norms.

· EU seems to be operating in a grey zone. It now defines China differently across various areas: as a partner in addressing common challenges, an economic competitor, and a systemic rival. There also seems to be hesitation and resentment with-in EU to toe a US line given its high-handedness and recent trans-Atlantic differences.

Digging deeper into this topic will be filling enough pages, worth all the trees in a forest. I have earlier touched upon the trade and value chain’s part. But two other important aspects will play out significantly in the future.

· Technology Standards – The US and Silicon valley have been at the forefront of setting standards for most part of 20th century for Computing, Communication and Dital. For many emerging and new technologies, leadership is yet to be claimed in setting. But China is upping the ante, creating a new kind of competition, no longer about technological superiority, but about rule making and system design. Standards are often invisible, yet they play a fundamental part. They can be seen as a powerful form of transnational authority by defining the status of public and private parties involved. The exponential developments in the technology sector will require a vast array of new industry standards to support it. China aims to set this global governance agenda and shape the international norms and widely practiced standards.

· Finance and Currency – It is China’s stated goal to “Knock Dollar off its Pedestal”. China will intensify its efforts to decouple from Dollar based trading and financial system. In pursuit of this goal, it will enlist other countries that are equally wary of dollar dominance. China has been trying for more than a decade to carve out a bigger global role for the yuan, or renminbi (RMB). In the current environment, driven by fears about impact of US economic policy and weaponization of the Dollar, Beijing has changed its approach and stepped up its efforts. Primary goal is to reduce its strategic vulnerability that stands in the way of China’s geopolitical ambitions.

Conclusion – Investing for the Future

How should we approach the new world order? What does it mean for investors and companies? A couple of points to note about what might come:

Macroeconomic Divergence

· As we move away from the stable waters of “Washington Consensus”, we are entering choppy global waters. As the aims and goals of different countries diverge, we are likely to see a divergence of policies in a multipolar world and this would definitely result in divergent Macroeconomic and Business performances across the spectrum.

· The three biggest economic blocs, US, EU and China seem to be moving in different directions. In 2023, the US is most likely to face a recession. China will probably rebound from its self-inflicted Zero-Covid policy and EU is well anyone’s guess. At the same time, countries like India, GCC Countries, Japan and Korea will probably be middle of the spectrum.

Greenflation and Stagflation

· Inflation has been in the news for the past year. Expect to hear more of it going forward. Driven by long ultra-loose fiscal and monetary policies, this bout of inflation has been further fuelled by supply side shortages, further restructuring of supply chains, rise in cost of energy, metals, food and fertilizers. We should expect to see more Capex in industrial capacity as the drive for self-reliance and friendshoring. If inflation is here to stay and aided by rise in populism, we might see more fiscal intervention by the governments across the globe, further fuelling inflation and eventually leading to Stagflation.

· As we move towards Green Energy and Decarbonization, a reality not discussed much is Greenflation. Greening the planet is mineral and commodity intensive and given the Geoeconomics and development of new supply chains, it will lead to Greenflation. A double whammy is the fact that, there has been gross underinvestment in Fossil Fuels the past decade. As the world accepts the inevitability of they being an integral part of out economy and enter a new investment cycle, expect Energy prices to stay high

Investments as a Macroeconomic Play

Let me highlight here a very useful insight and a chart from Cognitive Investments:

“In an environment where economic policy (and economic performance) is diverging wildly, there is now enormous potential for wealth creation in picking the right countries – and avoiding the wrong ones. There is a common misperception that stock markets across the world essentially move up and down together, and that investors can get optimal “international exposure” by simply owning a broad international mutual fund or ETF. This is wrong. It confuses correlation – i.e., how markets move together on a day-to-day, or week-to-week basis – with actual long-term returns.

Although global stock markets can be highly correlated in the short term, the dispersion of returns across various geographic markets – which is what investors really care about – is extremely wide and is bound to get wider in the coming decade. In a typical year, there is a return gap of ~70 percentage points between the best-performing country and the worst performing country. Put another way, in any given year, putting your money into the best performing country could earn you a +50% return, while putting your money in the worst performing country could lose you -20%. It pays to be picky”.

Investments as a Value Chain Play

As we had highlighted earlier, Battery Value Chains are going to play a important role in the future. We will need batteries, literally everywhere, be it Energy Storage or Electric Vehicles. Committed and planned Capex across the value chain will be huge. Is it possible to play the Battery Capex Cycle?

Well Morgan Stanley thinks so. They have identified a set of organizations that would benefit from this cycle. They have created a Battery Capex Portfolio, identifying 13 companies that would benefit across the value chain: Upstream, Midstream and Downstream. These include companies involved in mining Lithium, to battery Manufactures and End user OEM’s. They highlight this as a play on geographic margin in the US and Europe, as war and inflation usher in the next phase of innovation.

In conclusion, we are entering an era of uncertainty, complexity and volatility. It will come with a host of threats, but also great opportunities. Spotting these opportunities will require all of us to unlearn lessons of the past three decades. We are not returning to world of “Great Moderation” and predictable businesses. What we need is new set of lenses to identify these opportunities and open mind to assess all possibilities and outcomes.

Great insights...