Surprised Again? - This Time is Not Different

The twelve golden words from Sir John Templeton ring true every time - ‘The Four Most Expensive Words in English are, “This Time is Different”. One of my all-time favourite books is, “Extraordinary Popular Delusions and Madness of the Crowds”, by Charles Mackay. Originally written in 1841, this classic has timeless lessons. One particular sentence keeps coming back to me and there is no better time to revisit it, than now - “Every age has its peculiar folly—some scheme, project, or phantasy into which it plunges, spurred on either by the love of gain, the necessity of excitement, or the mere force of imitation.”

Most people know virtually no financial history, so when we have a financial crisis or a stock market crash, people are surprised. For many, something like the current occurrence has never happened before. Younger people might be forgiven for believing it is unique to their experience and times, but with an historical perspective, they should not be surprised. We don’t even have to look very far back for another bubble or a crisis – There was the dot com bubble of the late 1990’s and the GFC of 2008.

Somethings never change and it is a sense of Déjà Vu again. Past few years have been so different, yet everything seems the same. When we rise above the mundane existential grind, step back and take a 20,000 ft view, nothing seems to have changed. The post Covid world was flush with liquidity and money was waiting to be invested. In a world of negative to zero interest rates, where debt and safe deposits yielded negative real returns, it was Risk-On. Driven by cheap money, risk looked alluring. Markets around the world rose to dizzying levels. Fundamentals took a back seat and the new kids on the block were: Growth and Concept stocks, Bitcoin and Crypto, Meme Stocks, Electric Vehicles and other themes. Money went into sectors, where new narratives were sold fuelled by the emerging class of Fintwits and YouTube influencers. This was a perfect platform for naïve, inexperienced and wannabe investors to realise their dreams of untold riches and the result was, “This Time Is Different”.

After a Brief lull in 2022, the animal spirits got a fresh lease life with the arrival of ChatGPT, and the new narratives were about Generative AI and how it would radically transform the world as we know it. These new narratives about AI have driven the US technology stocks, especially the Mag 7 to eye-popping valuations and an unprecedented share of global market capitalization, creating what BCA Research calls a "50-year mispricing". For the first time in over five decades, the combined valuation of the US tech firms exceeds that of the entire European stock market. As it happened in the past, investors are sold to the narrative that AI's productivity gains will translate into sustained profits for the US tech giants. But if history has anything to teach, it is that the winners of one technological revolution are rarely the leaders of the next. The network effects that helped entrench the previous generation of tech monopolies may not apply to AI.

Selling Dreams of Wealth and Snake Oil Salesmen

The word Snake Oil has become a symbol of fraud and deception. In the recent past, it has been thrown around during the US elections, when talking about Covid vaccines and now there is even a book titled “AI Snake Oil”. From its origins, when it actually was a well-intended cure for certain ailments, it took the form and meaning that we are most familiar with in the 19th century. The terms “snake oil” and “snake-oil salesperson” are part of the vernacular thanks to Clark Stanley, a quack doctor who marketed a product for joint pain in the late 19th century.

The 1800s saw thousands of Chinese workers arriving in the United States as indentured labourers to work on the Transcontinental Railroad. Most of the workers came from peasant families in southeastern China and among the items the Chinese railroad workers brought with them were some traditional Chinese medicines and prominent among them was Snake Oil. Made from the oil of the Chinese water snake, which is rich in the omega-3 acids that help reduce inflammation, snake oil in its original form really was effective, especially when used to treat arthritis and bursitis. The workers would rub the oil, used for centuries in China, on their joints after a long hard day at work. So how did a legitimate medicine become a symbol of fraud?

The story goes that the Chinese workers began sharing the oil with some American counterparts, who marvelled at the effects. As word of the healing powers of Chinese snake oil grew, many Americans wondered how they could make their own snake oil in the US. Since they did not have any way of getting their hands on the Chinese water snakes, many healers began using rattlesnakes to make their own versions of snake oil. This was led by a charismatic entrepreneur named Clark Stanley, aka The Rattlesnake King. He claimed that he had learned about the healing power of rattlesnake oil from Hopi medicine men and never ever publicly mentioned Chinese snake oil at all. This coincided at a time which saw a dramatic rise in the popularity of "patent medicines", which were advertised in the back pages of a newspaper and were sold as a cure-all for a wide variety of ailments and chronic pains.

Stanley’s snake oil was a marketing gimmick from the beginning and rattlesnakes have different fat profiles than Chinese water snakes. While he continued producing and selling what he claimed to be snake oil, since the process of repeatedly taking fat from rattlesnakes proved cumbersome, Stanley removed any oil from snakes from his product altogether. It all came to an end after the introduction of Pure Food and Drug Act in 1906, which sought to clamp down on the sale of patent medicines. After seizing a shipment of Stanley's Snake Oil in 1917, federal investigators found that it primarily contained mineral oil, a fatty oil believed to be beef fat, red pepper and turpentine. And it was around this time that snake oil became symbolic of deception, false promises and even outright fraud.

So let us meet some of our modern-day Snake Oil sellers in the financial industry, selling investment ideas. These salesmen know the product is flawed but they sell it, anyway, relying on expert storytelling. Unfortunately for gullible retail investors, there’s an entire bullshit-industrial complex dedicated to concocting appealing narratives, the latest shiny fad that is in demand. Brokers, research analysts, consultants, self-proclaimed experts, talking heads on TV, snake-oil salesmen on social media, there’s a whole ecosystem of people whose livelihood depends on peddling stories to you. Sadly, the leaders of this trend in some cases are “Star Managers” of Mutual Funds, where their narratives manifest in the form of “Thematic Investing”.

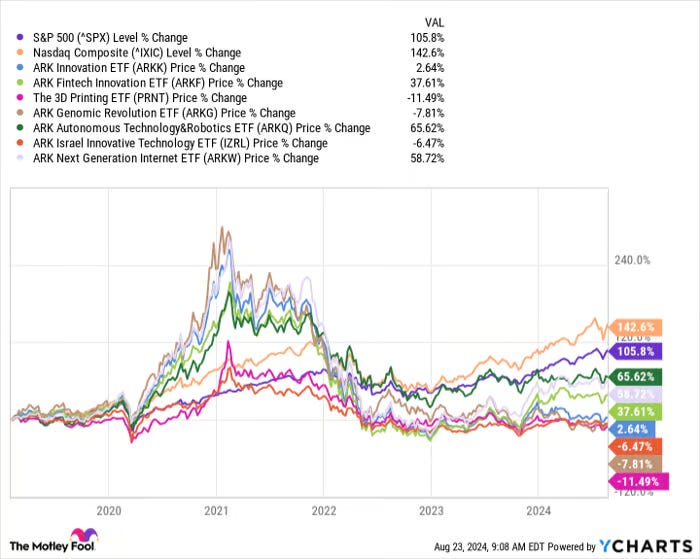

The poster child of Thematic Investing trend is Catherine Wood, Diva of everything Digital, Disruptive and Decentralized. ARK Invest run by her is at the forefront of investing in this exponential change. Their annual “Big Ideas” celebrates the emergence of everything futuristic and how it would change humanity for ever. Read by millions of starry-eyed investors, this is the validation of eternal truth prophesized by the reincarnation of “Oracle of Delphi”. She led the hype and sold dreams of wealth based on investments in world changing innovation. She and her company made quite a name for themselves in 2020 when many of their ETFs were easily outpacing the already bullish market. It was a time when investors readily embraced and bid up stocks of companies with novel business ideas. ARK hyped-up everything from Genomics to Robotics and launched funds to cater to the dreams of retail investors. While Nasdaq and S&P hit all-time highs, gullible investors in these schemes were stuck with sub-par or even negative performance.

The fund managers at ARK's ETFs aren't buying and holding stocks and then letting time do most of the heavy lifting. They are trading pretty frequently and in 2024, their stock turnover in the ARK Next Generation Internet ETF was 33%, meaning one-third of the portfolio's stocks have been swapped out for others in the previous 12 months. So much for the conviction of the stories you peddle. Any sensible investor knows that this kind of turnover not only raises funds tax liability, but it impacts performance. Data consistently shows that funds meant to outperform the overall market by more frequent buying and selling of stocks underperform it far more often. To make things worse, it turns out that these funds also bought into their conviction stocks at their peak and what inevitably followed was a fast downhill ride. Too many of ARK’s buys and sells appear to be reactive rather than proactive, when much of the opportunity in question is already in the rearview mirror. And as I write this, the underperformance of their flagship fund continues.

They weren’t exactly great ideas you see!

The dotcom bubble build-up had similar Diva’s and Oracles. Mary Meeker, Henry Blodget and Abby Joseph Cohen. They had helped build the narrative around “Everything Online” and their stories should have served as a lesson. But we have learnt from history, that we don’t learn from history.

Closer home the cheer leader for this type of mis-selling is one of the leading fund houses in India, MOSL. They are experts at spinning fancy mind-numbing narratives and led by their chief “Snake Oil Salesman”, over the past decade they have built emotionally catchy wealth creation narratives with annual reports bearing fancy titles such as: Creating Wealth Through Bruised BlueChips, Hockey-Stick Returns – The power of Economic Profit and Consistents & Volatiles - The two dimensions of Wealth Creation.

One of their fancy narratives of 2024 was about Defence and the unprecedented prospects for Defence industry in India. In sales presentations, they were hyped up with emotionally appealing stories that also built FOMO. It was all about, we are in danger and how dangerous the world has become, a dangerous place after Russia’s invasion of Ukraine, the rising tensions in Middle East, and what this meant for countries like India. We will need to have to manufacture hundreds of thousands of guns, bullets and bombs, and hundreds of ships, submarines, rockets and drones at home. The government will splurge lakhs of crores, and all this money will go to defence companies. So, buy defence stonks and funds TODAY!! They launched their Defence Thematic Fund at the peak of the defence hype and the performance is there for anyone to see. They lured gullible investors at the peak of the hype cycle, probably knowing fully well that, forget outperformance, even capital preservation would be difficult.

Wait! there is more. Balance Advantage Funds are an industry offer, that manage allocation dynamically between equity and debt based on market conditions. They are meant to offer returns that are higher than pure debt, but in times of trouble, they also offer some protection against significant drawdowns. Well in their case, that doesn’t seem to be the case. While the average drawdown for other funds in this category was -6%, MOSL BAF had a drawdown of -23%. That is in many cases worse than 100% equity funds. Well, it seems that their equity investments weren’t exactly something to write home about. It will make this post unwieldy if I start getting into those details.

Did no one see this coming? History has highlighted a few very pertinent aspects:

· Retail investors on average are poor at timing investments. They consistently and reliably buy high and sell low.

· “Star” managers emerge in every bull market, whether by skill, luck, or both.

· Retail investors still manage to lose money or underperform in aggregate, by investing with these star managers and it’s possible, if not likely, that history will keep repeating.

There is enough precedence for this when we look at the dot com mania of the 1990’s.

“During the technology bubble of the 1990s, one of the “star” managers of the time was Janus, a growth manager that developed a good reputation in the 1980s and early 1990s. The sparks began to fly in the latter half of the decade, with the flagship Janus fund rising 39% in 1998 and 47% in 1999. The firm had a more concentrated fund (Janus Twenty) that was up even more, earning 73% in 1998 and 65% in 1999. By 2000 Janus was reportedly taking in $1 billion per day, and firm assets peaked at $330 billion.

What was a virtuous circle on the way up, with fund flows being instantly deployed into a handful of high-flying technology stocks, became a vicious cycle once the bubble burst. As prices began to collapse and redemptions poured in, Janus was forced to unload massive positions in companies like Cisco and Microsoft, driving the prices down even more.

Between 2000 and 2002 the flagship Janus fund declined by 64%, and Janus Twenty dropped 69%. Its Global Technology fund was pasted by 84%. Nearly all the gains from the late 90s bull market were wiped out in percentage terms but given most of the fund inflows occurred in the latter part of the market, in aggregate investors suffered massive losses.”

No one was listening. But are there patterns one can decipher?

In their book, “Bubbles and Crashes – The Boom and Bust of Technological Innovation”, Brent Goldfarb and David Kirsh, analyze fifty-eight major innovations appearing between 1850 and 1970 that may or may not have led to speculative activity. There identify two common themes that underly all the bubbles”

• Uncertainty and Narratives

• Novices and Biases

Every Innovative Technology in history has been associated with lots of uncertainty. Which are the firms and who are the people, who can take advantage of this and benefit from it? Who will capture the value and who will profit? The underlying uncertainty is an integral part of any emerging technology. This uncertainty is a fertile ground for imagined futures. Fecund minds weave narratives and tell stories that sometimes are plausible, but for most stay well and truly in the realm of incredulous. But we humans are not wired for data, our brains are wired for stories. Stories and narratives captivate us and capture our imagination. They let us imagine a desired future and break free from the humdrum of the present. They offer the lure of escaping to that desired world. Narratives around, Business Models, Potential Revenues and Disruption capture our attention and align them to our beliefs.

Every bubble is characterised by the presence of novice or unsophisticated investors. During the dotcom boom, it was the millions who found investing liberating through E*Trade and today it is the Robinhood Generation. They tend to be overoptimistic and overconfident, leading to poor buying decisions, increasing the demand for risky assets. These “noise traders,” are overly bullish, inexperienced, and less financially literate. They are easy prey to narratives about potential opportunities that are new and seem exciting. With crypto, that story is the promise of disrupting and replacing the traditional financial system. With AI, it is about absolute change in how the world functions and nothing short of a total humanity-wide revolution. Gold is being sold as a hedge against doomsday that is around the corner and as has been the case for 5000 years, it is and will be the only safe-haven and insurance against some horrible thing that’s about to befall the markets. I wish, if only history and future worked this neatly and nicely. But who cares?

Final Words - Don’t Predict, React

Despite three years of falling prices, which have significantly improved the attractiveness of common stocks, we still find very few that even mildly interest us. This dismal fact is testimony to the insanity of valuations reached during the Great Bubble. Unfortunately, the hangover may prove to be proportional to the binge. The aversion to equities that Charlie and I exhibit today is far from congenital. We love owning common stocks—if they can be purchased at attractive prices. . . . But occasionally successful investing requires inactivity. – Warren Buffet in 2003.

Golden words from the Oracle of Omaha.

History might not repeat, but it definitely rhymes. History is a veritable museum of human follies and foibles, that seem to have a similar pattern. The manias, panics, bubbles and crashes separated in time and space, all seem to have similar patterns and occur in the context of identical backgrounds. In todays’ world when all this can be accessed at the click of a few buttons, why is it that we never seem to learn? Look at the headlines in the recent days: inflation numbers, rising interest rates, hiring freezes, margin compressions, slowing growth in China, climate change and rising food insecurity. There seems to be heightened amount of uncertainty. How might all this play out? Well, I don’t know. I don’t know what might happen next week or next month. There might be a recession or there might be another war. Will the markets rise or fall? No one has ever come out clean in predicting that. None of us know what will happen. For all we know there just might be a Black Swan lurking around the corner. Future is inherently uncertain.

This is a great illustration from Jack Raines of Young Money. The biggest risks come from two things

· Our perception of risk, which forces us to panic and do something that is not in our best interest.

· Risk from that we don’t know.

As Morgan Housel put it nicely,

“The idea that uncertainty is higher now than it was, say, one or two or five years ago is a strange one. It implies that the future was more predictable in the past, before the pandemic struck and inflation spiked, and the war broke out. But it wasn’t, of course. The risks were always there. People were just blind to them. The future is always endlessly unpredictable. What changes isn’t the level of uncertainty, but the level of people’s complacency.”

The biggest risk is doing something based on assumptions. Sell everything off and put the money under a mattress or just go no holds barred and invest everything in the market. Fatal risk will come out of me doing something extreme driven by emotions. I am a student of history and if there is one thing I have learnt, it is that we react in extremes. Doomsday scenarios have always been with us but gain larger credence during times of stress and uncertainty.