Second Atomic Age – The Global Nuclear Revival

2024 was the year when “AI went Nuclear”. A common thread running through the future plans of Microsoft. Google, Amazon and Meta is their commitment to Nuclear Energy. While Generative AI and Data Centres got all the news bytes and interest, it was this less spoken about fact that deserves more attention. Big tech is investing in or restarting old nuclear reactors and planning new ones to power the energy-hungry data centres that artificial intelligence systems need. These companies are investing heavily in hyperscaler data centres with a voracious appetite for electricity, some of which consume as much electricity as a small city does and they have all come to the same conclusion – Nuclear Energy is the only viable solution.

Last year, Microsoft announced plans to revive the shuttered nuclear power plant at Three Mile Island, the site of the worst nuclear accident in the United States in 1979. Apart from this, they also signed a contract with Constellation Energy to restart another reactor six miles away on the same island, which was shut down in 2019 for reasons of financial viability. Constellation plans to reopen the reactor and sell 100 percent of the electricity that will be generated by it, enough to power 800,000 homes to Microsoft. Similarly in Michigan, another shuttered nuclear power plant at Palisades could be operational as early as 2025. The reactors at Palisades and Three Mile Island would be the first ones ever restarted after decommissioning.

Apart from reviving existing nuclear plants, these tech giants are also investing heavily in the development of new age nuclear reactors, known as Small Modular Reactors (SMRs). In October 2024, Google announced a deal to purchase nuclear energy from SMRs that will be developed by Kairos Power. Two days later Amazon said it had signed agreements to invest in four SMRs to be constructed, owned, and operated by Energy Northwest, a consortium of public utilities in Washington state. Amazon hopes the new reactors can power a cluster of data centres in eastern Oregon. Oracle has joined the bandwagon and is designing an AI data center to be powered by three SMRs, which it says are necessary to meet AI’s crazy energy demands.

Future exponential rise in electricity demand

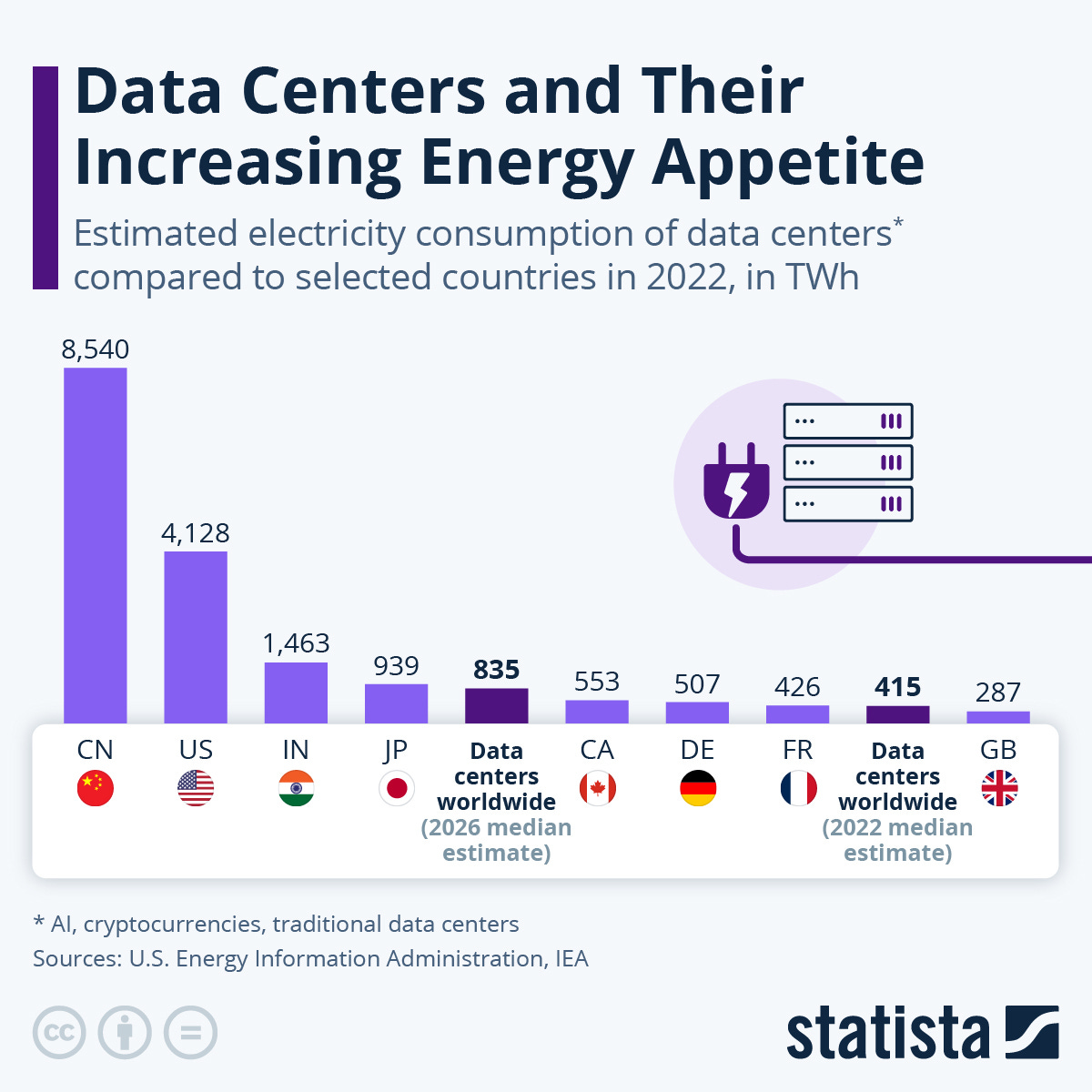

How much energy is consumed by data centres? Rephrasing the question, what is the demand for electricity from the data centres globally? This chart by Statista is self-explanatory!!

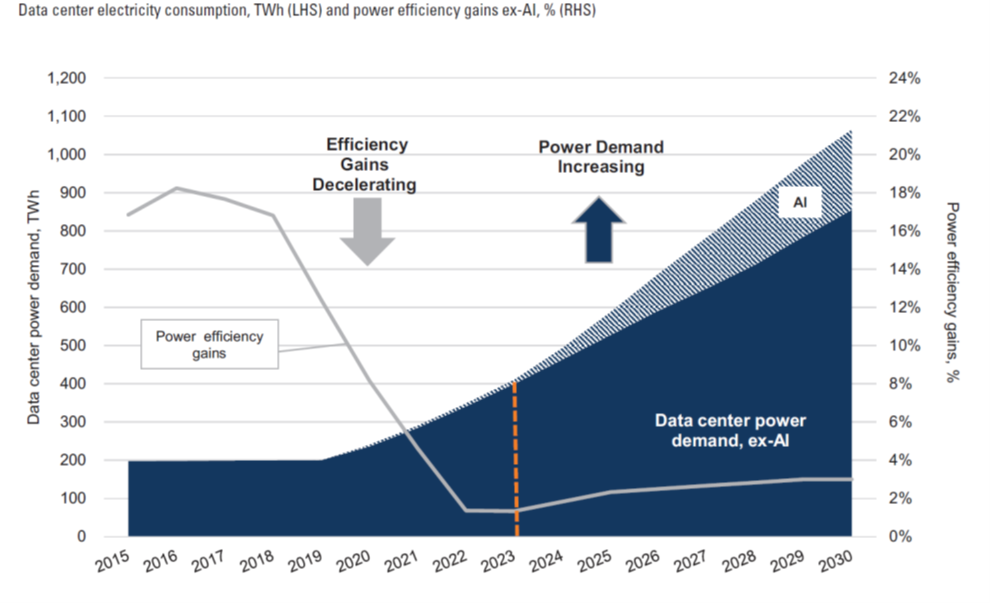

According to a report by Goldman Sachs from April 2024:

· For years, power demand from data centres was flat despite a near tripling in thedata workload. Now with the pace of power efficiencies decelerating and AI demand building, our updated analysis implies data center power demand is poised to grow 160% by the end of the decade, which should drive a significant acceleration to a level of electricity growth in the US and Europe not seen in a generation.

· Data center power demand likely to rise 160% by the end of the decade vs. 2023 from 1%-2% to 3%-4% of overall global power demand by 2030. If all of the projected data center electricity demand growth was concentrated into a new country, it would be among the top 10 power consuming countries. We see US power demand growth accelerating to a 2.7% 5-year CAGR by 2030 vs. 0% for the past 10 years, with data centres driving 0.9% CAGR increase and representing 8% of US power demand by 2030 (vs. 3% in 2022). In Europe, we see EU-27 power demand accelerating to a 3.7% 5-year CAGR by 2030 from 0% for the past decade.

The data center industry is seeking energy solutions to reach its goal of increasing power capacity to 1,000 TWh by 2026 while maintaining high standards of scale, efficiency, speed-to-market, and emission-free generation. Nuclear energy is the best option out there. At the same time, other requirements from industries such as EVs and Crpto will also contribute to increased demands on the grid. Someone like Bill Gates, clearly believes that increasing energy needs will increase the importance of baseload power, for which nuclear is the best option. He has invested $1 billion in advanced nuclear energy and has raised nearly the same amount through TerraPower in hopes of making nuclear energy more abundant and less expensive.

Advantages of Nuclear Power

An important criterion that many people miss is the concept of “Base Load Power”, the minimum amount of electric power needed to be supplied to the electrical grid at any given time. Day to day trends of power usage vary and they need to be met by power plants, however it is not optimal for power plants to produce the maximum needed power at all times. Therefore, there are baseload power plants like coal-fired or fossil fuel power plants which provide the minimum needed electricity, and peaking power plants which meet the fluctuating needs. Baseload power must be supplied by constant and reliable sources of electricity, that often run round the year, hence needing a high-capacity factor and not use non-renewable sources like wind and solar, which are intermittent and unreliable. Nuclear plants produce a constant supply of electricity with out any disruptions and are an ideal source for baseload power.

Nuclear energy also has the highest “Capacity Factor”, (93%) of any energy source. What it means is that nuclear plants operate at 93% of their theoretical maximum capacity. For comparison, nuclear plants are 2-4 times as reliable as coal (42.2%), wind (33.2%), and solar plants (23.2%), and 59.7% more reliable than natural gas plants.

Another factor that favours nuclear energy is “Energy Density”, which is the amount of energy that can be stored in a given system, substance, or region of space. Energy density can be measured in energy per volume or per mass and is usually expressed as Megajoules per Litre (MJ/L) or Megajoules per Kilogram (MJ/kg). The higher the energy density of a system or material, the greater the amount of energy it has stored.

Nuclear is also one of the safest ways to produce energy. The safety standards have come a long way since the 1980s. There have only been three significant nuclear power plant accidents since civil power generation began – Three Mile Island (1979), Chernobyl (1986), and Fukushima (2011). Apart from Chernobyl, there have been no radiation-linked deaths or long-term displacements. With the evolution of newer technologies and next generation reactors, safety concerns have reduced drastically. Beyond safety, wind, solar, and nuclear have the lowest total lifecycle carbon emissions of any electricity source. While all three reduce direct emissions, a total life cycle analysis shows that nuclear has the lowest emissions of any other electricity source. Another important factor that favours nuclear energy is the land footprint. Next generation SMRs have a lower footprint and nuclear energy requires just 0.3 m2 of land per MWh of electricity, 50 times less land compared with coal, and 42-63 times less land than on-ground solar, making it the most land efficient source of energy.

Global Nuclear Revival

Globally there are 437 nuclear reactors operational today, of which 90% were built in the 1970s & 80s. There are 60 new reactors under construction, and 100 more are planned. Many old reactors are being refurbished for 80 years or more of total lifetime use.

Around the world, there is a growing chorus in support of nuclear energy, due to various economic and geopolitical factors. The changing policy landscape is setting the conditions for nuclear energy to continue making an important contribution to power systems around the world. Governments are increasingly recognising the benefits of nuclear energy as a low emissions source of electricity, that can make a valuable contribution to clean energy transitions and to energy security. The need to balance climate commitments and increasing energy needs has forced governments and businesses to reconsider nuclear energy. Growing policy support is reflected in recent decisions in several countries to authorise extensions to the operating lifetimes of existing nuclear reactors, for a total of 64 reactors in 13 countries, with a total capacity of about 65 GW, which amounts to around 15% of currently operational reactors.

Many countries are also designing policies that support the expansion of nuclear energy capacity. Currently, more than 40 countries plan to build new reactors or are considering doing so, including around 10 that do not as yet have any nuclear capacity. In December 2023, more than 20 countries pledged to triple global nuclear capacity collectively by 2050. At COP29 in 2024, an additional 6 countries have joined the pledge. Support for SMRs has grown in recent years and over 30 countries have been developing SMRs or are considering deploying them.

Since 2017, the majority of new commercial nuclear construction has taken place in just China and Russia and in 2022, the growth rate of nuclear energy consumption was -1.0% in the US, whereas it was +2.5% in China. In advanced economies, the major challenges facing nuclear power growth are its high capital costs and long development timeline. Building a traditional nuclear plant, with about 1 GW capacity takes a median of 88 months and costs about $8 billion to $14 billion. Emerging next generation reactor designs are predicted to reduce costs and make it possible to realize the full potential of nuclear energy. SMRs could reduce upfront costs and construction time, due to their simple and more modular design. SMRs typically generate under 300 MW, as opposed to 1GW for standard reactors, and may be able to modulate their power outputs, making them both cheaper and more flexible. SMR companies are developing reactors that can be entirely fabricated in a factory and installed on-site, reducing development costs.

SMR designs with capacities at the upper end of the range are under development in the United States and United Kingdom. Medium sized reactors are the focus of R&D in China, Japan and Korea. Several countries are working on smaller SMRs, for example in Canada to provide power to remote areas and in India to power steel mills. Various EU countries are interested in deploying SMRs with a wide range of sizes under consideration depending on policy, agreements with SMR developers and energy security needs. Some African countries, including Kenya and Ghana, are also looking into building SMRs.

This infographic below from Mitsubishi provides a good visual understanding of how nuclear reactors are evolving.

China Takes the Lead

China dominates global supply chains for EV’s, renewable energy and batteries and is now setting its sights on becoming a superpower in nuclear energy. China understands the simultaneous need for clean baseload power in the form of nuclear in addition to intermittent renewable energies to reduce its current heavy reliance on coal. Over the past several decades, as the West has grown increasingly cautious about nuclear, China has forged ahead and is now building twenty-five reactors, more than the next six countries combined. In fact, it has more nuclear reactors under construction than any other nation in the world, and approved ten new reactors in each of the past two years. The country is expected to surpass France and the United States to become the world’s leading nuclear power generator by 2030. It also is responsible for a new breakthrough, a meltdown-proof nuclear reactor, which has been a goal for several US companies and US Department of Defence, but which China is building faster.

· China intends to build 150 new nuclear reactors between 2020 and 2035, with 27 currently under construction and the average construction timeline for each reactor about seven years, far faster than for most other nations.

· China has commenced operation of the world’s first fourth-generation nuclear reactor, for which China asserts it developed some 90 percent of the technology.

· China is leading in the development and launch of cost-competitive SMRs.

· China likely stands 10 to 15 years ahead of the United States in its ability to deploy fourth-generation nuclear reactors at scale.

· China’s innovation strengths in nuclear power pertain especially to organizational, systemic, and incremental innovation. Many fourth-generation nuclear technologies have been known for years, but China’s state-backed approach excels at fielding them.

· US and China are likely at par when it comes to efforts to develop nuclear fusion technologies, but China’s demonstrated ability to deploy fission reactors at scale gives it an advantage when fusion comes online.

· Looking narrowly at scientific publications on nuclear energy, China ranks first in the H-index, a commonly used metric measuring the scholarly impact of journal publications.

· From 2008 to 2023, China’s share of all nuclear patents increased from 1.3 percent to 13.4 percent, and the country leads in the number of nuclear fusion patent applications

Final Words

The nuclear energy race is well and truly underway. As the world continues to develop economically, driven by both industrialization and technological advancement, its need for power is increasing. Nuclear has taken the center stage owing to multiple factors: Artificial Intelligence, EV’s, Cryptos, Climate Change and Decarbonization, Energy Security and Geopolitics. In all of history, no country has advanced economically without access to affordable, reliable, and secure energy. Robust energy is the foundation of economic strength, which in turn undergirds national security through resources and innovation. In the coming years and decades Nuclear Supply Chains will be an arena of intense competition. My next article will be about the evolving Geopolitics of Nuclear Energy and Uranium and how Russia and China plan to dominate it.

Thanks, simple and informative