Narratives, Affect and Popularity in Investing

It all started with a shipwreck. In the 1690’s, London saw a tech bubble that rose out of a successful treasure hunt, which was led by a New England sea captain called William Phipps. A Spanish ship called “Nuestra Señora de la Concepcion” had sunk in the West Indies during the 1640’s and was rumoured to have unimaginable riches on board. Phipps decided to try his hand at locating the ship and the long-lost treasure, and in this endeavour was backed by a group of investors led by the Duke of Albemarle, in what can be termed as the 17th century version of ad-venture capital.

After years of effort trying to locate the wreck, Phipps and his team finally found the treasure in 1687, and what they found was beyond their imagination. He and his team spent over two months hauling up 32 tons of treasure from the ocean floor. On their return to London, after the King, Captain Phipps, and his sailors had received their portions, nearly £190,000 was left to distribute to the partners who had backed the expedition, which amounted to a 10,000 percent dividend, "enriching them beyond expectation". The success of the expedition created a great stir across the country and led to an explosion in new “seawater diving engine” or “diving bell” companies that promised investors similar treasure hunting success with exciting new technology that would enable more efficient treasure hunting expeditions. Others sought to emulate Phipps s success. But unlike in his case, which had investors backing, the new treasure-hunting schemes were floated as joint-stock companies. The age of adventuring, a tradition going back to the Elizabethan privateers, suddenly gave way to an age of speculation.

In England, patents were sought and granted for diving engines for ‘the sole fishing of wrecks on the coasts of America, Spain, Portugal, Ireland, Scotland, and England’ and numerous societies were formed of merchants and gentlemen to manage these expeditions. Between 1672 to 1689, five patents were granted for diving engines, but in the first three years of the 1690s, after Phipps successful expedition, this more than doubled, and added to this were an even higher number of petitions for patents that were filed. These engines were of various make: some like a bell, others a tub, some like a complete suit of armour of copper, and Leather between the Joints, and Pipes to convey Wind, and a Polyphemus Eye in the Forehead to give Light, and staying under Water many hours.

As Edward Chancellor highlights in his book, Devil Take the Hindmost:

· Two types of "diving" company were launched in the wake of Phipps s success. The first kind acquired a "patent" from the government which gave it monopoly rights to "fish" for wrecks at specific locations. Thomas Neal, the Master of the Mint and the leading projector of the age, was involved in three patented salvage companies for operations off Jamaica, Bermuda, and Portugal. Captain John Poyntz of the Tobago Company applied for a patent for "taking up wrecks out of the sea and fishing for pearls and ambergris" in the West Indies. The other kind of diving company was established with a technological patent for one of the recently invented diving engines. As "Engine begat Engine and Project begat Project" over a dozen new diving engine companies appeared. They included the Company for Raising Wrecks in England, secured on a patent for the "diving bell" of the Astronomer Royal, Edmund Halley (the company appeared in the early stock lists as "Diving Halley"). Daniel Foe (as the author of Robinson Crusoe then styled himself) was employed as the secretary-treasurer to another diving bell company, established by a Cornishman named Joseph Williams.

· The diving company projectors set out to stimulate public interest in their shares. "The wealth which was fetched out of the sea was trumpeted all over the World," public demonstrations of diving engines were given on the Thames, and free shares were given "to People of Note and Figure, to give Reputation to the Affair; and these doughty Names were subscribed to play the Part of a Shooing- Horn, and wheedle in the Eassie; Treats and Money were given to the Necessitous and Sharp, to bring their Friends and Acquaintance to see the Engine. In its prospectus, the diving company of Captain Poyntz promised a return of 100 percent to investors. The hype sent shares to a great premium above their issue price. Defoe reported that he had "seen Shares in Joint- Stocks, Patents, Engines and Undertakings, blown up by the air of great Words," with the shares of one diving company rising by 500 percent. However, the craze for diving machines and treasure-seeking companies soon died down after their failure to salvage anything more than a a few Iron-Guns, Chimney Backs, and Ship's Tackle." The share price of the same company that had increased fivefold began to "dwindle away, till it has been stock-jobbed down to 12, 10, 9, 8 /. a Share and at last no buyer." Defoe was writing from unhappy experience, having lost £200 in Williams's diving company: years later he wrote, "I could give a very diverting history of a patent-monger whose cully [i.e., dupe] was nobody but myself."

All this sounds familiar! We are currently living through a similar mania around “Artificial Intelligence” and in the past few decades we have seen euphoria over internet and biotech. We reacted, behaved and invested the same way almost 350 years ago as we are doing today. What causes these manias and ensuing panics? There are three specific phenomena that probably help us understand them better: Narratives, Affect, and Popularity.

Narratives

· “No one ever made a decision because of a number. They need a story.” Daniel Kahneman

· Stories are we tell, and Narratives are what we believe in.

As I had highlighted in a couple of my previous articles, in their book, “Bubbles and Crashes – The Boom and Bust of Technological Innovation”, Brent Goldfarb and David Kirsh, analyze fifty-eight major innovations appearing between 1850 and 1970 that may or may not have led to speculative activity. There identify two common themes that underly all the bubbles,

• Uncertainty and Narratives

• Novices and Biases

Every Innovative Technology in history has been associated with lots of uncertainty. Which are the firms and who are the people, who can take advantage of this and benefit from it? Who will capture the value and who will profit? The underlying uncertainty is an integral part of any emerging technology.

This uncertainty is a fertile ground for imagined futures. Fecund minds weave narratives and tell stories that sometimes are plausible, but for most stay well and truly in the realm of incredulous. But we humans are not wired for data, our brains are wired for stories. Stories and narratives captivate us and capture our imagination. They let us imagine a desired future and break free from the humdrum of the present. They offer the lure of escaping to that desired world. Narratives around Business Models, Potential Revenues and Disruption capture our attention and align them to our beliefs.

Every bubble is characterised by the presence of novice or unsophisticated investors. During the dotcom boom, it was the millions who found investing liberating through E*Trade and today it is the Robinhood and Reddit Generation. They tend to be overoptimistic and overconfident, leading to poor buying decisions, increasing the demand for risky assets. These “noise traders” are overly bullish, inexperienced, and less financially literate. They are easy prey to narratives about potential opportunities that are new and seem exciting.

It boils down to “The Power of Stories”. We humans are not hardwired for data, but for stories. We have been sharing stories since the dawn of civilization and these stories have the ability to persuade and connect people, while allowing us to store and understand complex information. MRI scans have shown that neural circuits that process emotion light up when someone is listening to a story. It is this emotional aspect of storytelling that can cause a narrative to catch people’s attention and spread. In the context of today, the feelings of wonder and fear created by narratives about Generative AI’s ability to enhance productivity or potentially destroy millions of jobs through automation has contributed to all the hype. The intensity of the story then relies on its ability to tap into human emotions until it becomes entrenched and goes viral, building narratives.

A nice way to visualize this was put across by folks at Beutel Goodman in the form of a narrative wave. These waves have the power to drive deviations from fundamental value based on a story as highlighted in the visual below. The horizontal line is the fundamental value, which is less volatile and only changes with new information. Narratives, represented by the blue line segments, can cause deviations in asset prices around these fundamental values to either the upside or the downside.

Changes in market narratives have the power to drive the pricing of stocks away from the fundamentals, creating volatile swings in asset prices. These swings are sometimes referred to as “animal spirits”, “uncertainty”, “bull/bear sentiment”, or “fear and greed”, but the key point is that markets are often driven by a story.

Robert Shiller in his book “Narrative Economics”, explains the influence that popular stories have on the way economies operate. The popular stories at the time can change economic outcomes, leading to everything from a craze of novice investors getting into Bitcoin to a spread of panic during a stock-market crash. To get a full picture of what drives financial markets, one must also look at the surrounding narratives. Trying to understand major economic events by looking only at data on changes in economic aggregates, such as gross domestic product, wage rates, interest rates, and tax rates, runs the risk of missing the underlying motivations for change.

Affect

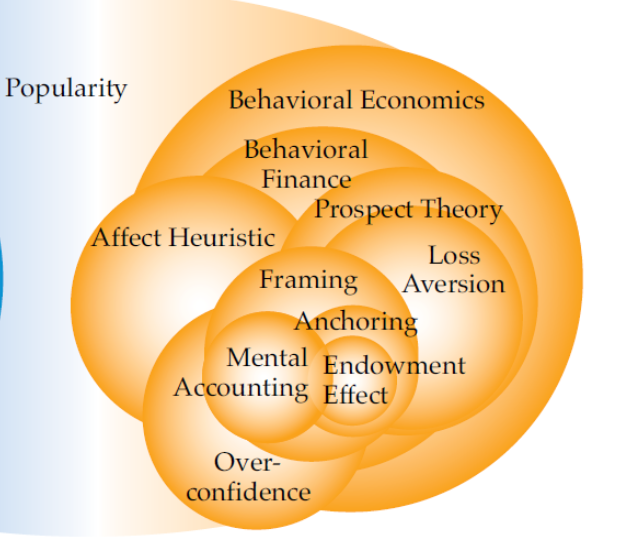

Stories we hear and the narratives about something “Affect Us”. Affect is the faint whisper of emotion or mood, stripped down to valence, positive or negative. Psychologist Robert Zajonc was an early proponent of the importance of affect in making choices. He wrote, “We do not just see a house, We see a handsome house, an ugly house, or a pretentious house”. Beginning in the early 1980s, a lot of work has been done in the area of behavioral finance and today it form the core of our understanding about why bubbles occur so frequently and result in such enormous price movements in manias and panics. They also address many other questions related to the market, some of which are critical to our investment decisions and risk analysis.

The most important discovery is that of the Affect heuristic, an important component of our judgment and decision making. Our strong likes, dislikes, and opinions, experienced as feelings such as happiness, sadness, excitement, and fear, can either consciously or unconsciously, heavily influence our decision-making processes. Affect is emotional, not cognitive, and the response being emotional, need not be rational and often isn’t. Affect plays a central role in what have become known as dual-process theories of our mental processing of information. Individuals understand reality through two interactive parallel processing systems: the rational-analytic system, which is deliberative and analytical, functioning by way of established rules and evidence. The other system, which psychologists have labelled the experiential system, is intuitive and nonverbal. The experiential system draws on information derived from experience and emotional recall and encodes reality into images, metaphors, and narratives to which affective feelings have been attached.

Being emotional, not cognitive, the experiential system is much faster than the rational-analytic system. Just step back and reflect, how quickly a reaction starts to form in our minds if we think of a big investment gain (positive Affect) or we will have a wipeout in a favourite stock (negative Affect). Affect can be such a powerful emotional pressure that it can insidiously override our training and experience in the marketplace and goes a long way toward explaining extreme stock mispricing. Images and associations are pulled into the conscious mind from past, current, and hoped-for experiences. And the more intense our positive or negative feelings are, whether about ideas, groups of people, stocks, industries, or markets, the more intensely Affect influences our decisions on them.

The role of the Affect Heuristic on investors manifests in two very important ways:

· Insensitivity to probability.

· Negatively correlated judgments of risk and benefit

Affect leads to errors in judgment and it causes us to be insensitive to the true probability for investments to increase or fall in price while not factoring in the reasons this should happen. When a potential outcome, such as a major gain from a stock purchase carries sharp and strong affective meaning, the actual probability of that outcome, or changes in the probability due to changing circumstances, will tend to carry very little weight.

A study found that investors apparently did not care what price they paid for an exciting IPO in a bubble market. As economist Robert Shiller demonstrated, if an investor wanted to buy a hundred shares of a company, say at $10, it didn’t matter to him if the company had one million shares to sell or, having split just prior to the IPO, five million shares to offer. Shiller found that quintupling the price of the outstanding stock was immaterial to the IPO buyer, who still wanted to buy the same one hundred shares at $10 a share even though they gave him only one-fifth of the previous value, because he was convinced the price would go higher. If we have very strong feelings about the prospects of a stock or another investment, we will sometimes pay 100 times its real value or more. This finding captures the major reason why stock prices are driven to astronomical heights during a bubble.

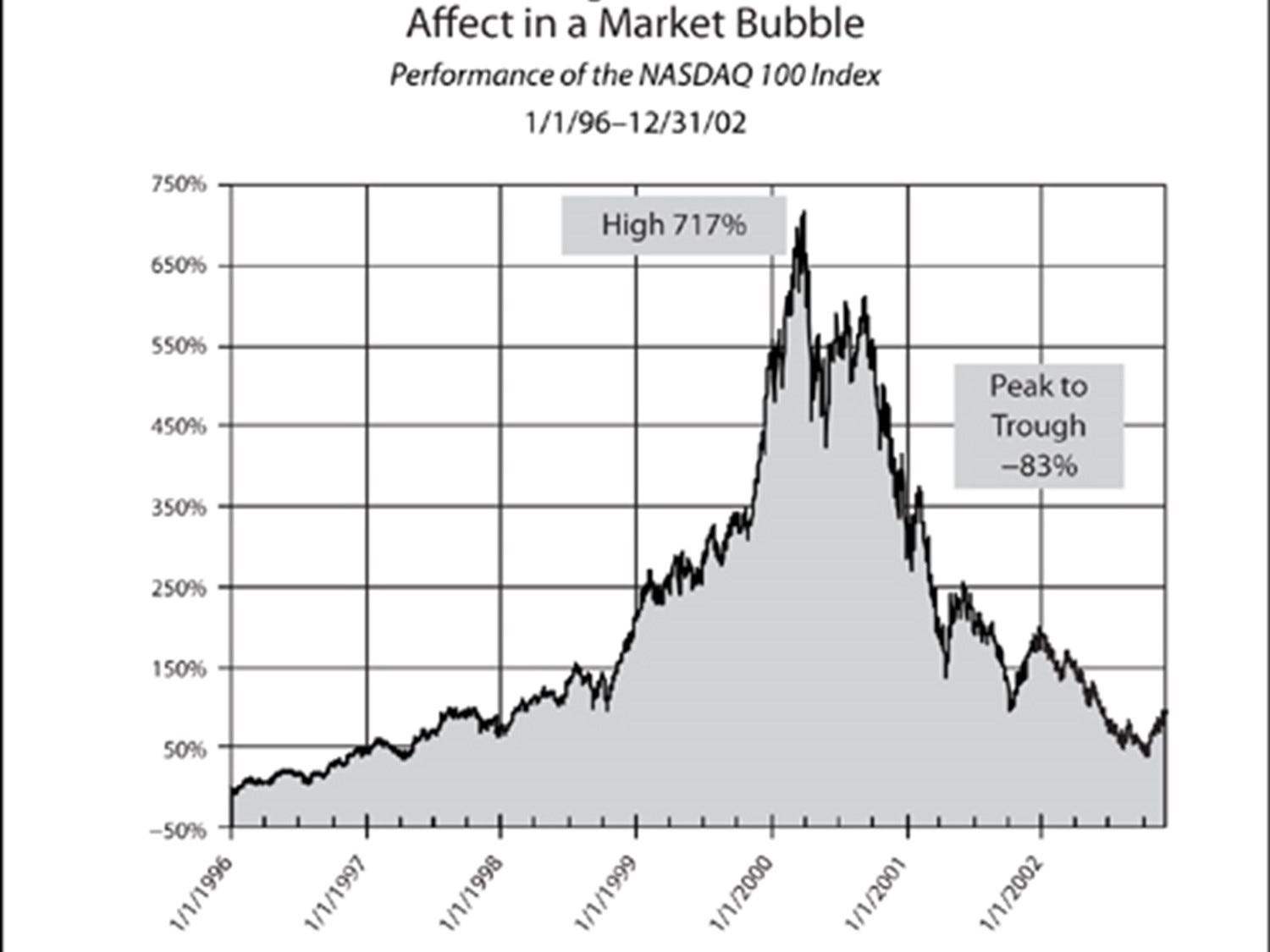

I started my career in the early 1990’s when internet was in its infancy and the first few years were an integral part of what we now call Dot Com boom. The years 1995 to 2001 were a period of great dreams, but also in hindsight, a fair bit of madness. Narratives were built and dreams were sold and unless you were living under a rock, you couldn’t escape the hype. Given the context, the above chart taken from a book by David Dreman is very instructive in explaining the Affect Heuristic and shows how dead-on the findings are. From the beginning of 1996 through the peak in March 2000, the NASDAQ 100 increased 717 percent. From the high-water mark of March 2000, the index dropped 83 percent to its October 2002 low, the worst decline of a major US index since the 1929–1932 period. Near the height of the bubble, the NASDAQ 100 had a P/E multiple of over 200 times earnings. Virtually all of the companies in the index had products or services that projected images of rapid growth, often far removed from any realistic chance of being attained.

People base their judgments of the risk and benefits of an activity or a technology not only on what they think about it, but also on how they feel about it. If they have an idea or concept they strongly like, they are moved to judge that the risk is low. The more they dislike an idea or concept, the higher they judge the risk. So, Affect again enters into the picture, this time allowing our feelings to tamper with and alter our rational decision making and choices on risk. If stocks are perceived as good, they are judged to have higher returns and low risk, whereas if they are perceived as bad, they are judged to be lower in return and higher in risk. During the 1996–2000 bubble, value stocks, which were far less risky by standard valuation yardsticks, had very negative Affect attached to them. As a result, the influence of Affect on most investors at the time made them believe that those stocks were far riskier than their valuation standards would indicate. They were often thought to be significantly riskier than IPOs or dotcom and high-tech stocks, both of which subsequently collapsed. The risk-reward situation had obviously been turned upside down during the dot-com mania.

Popularity

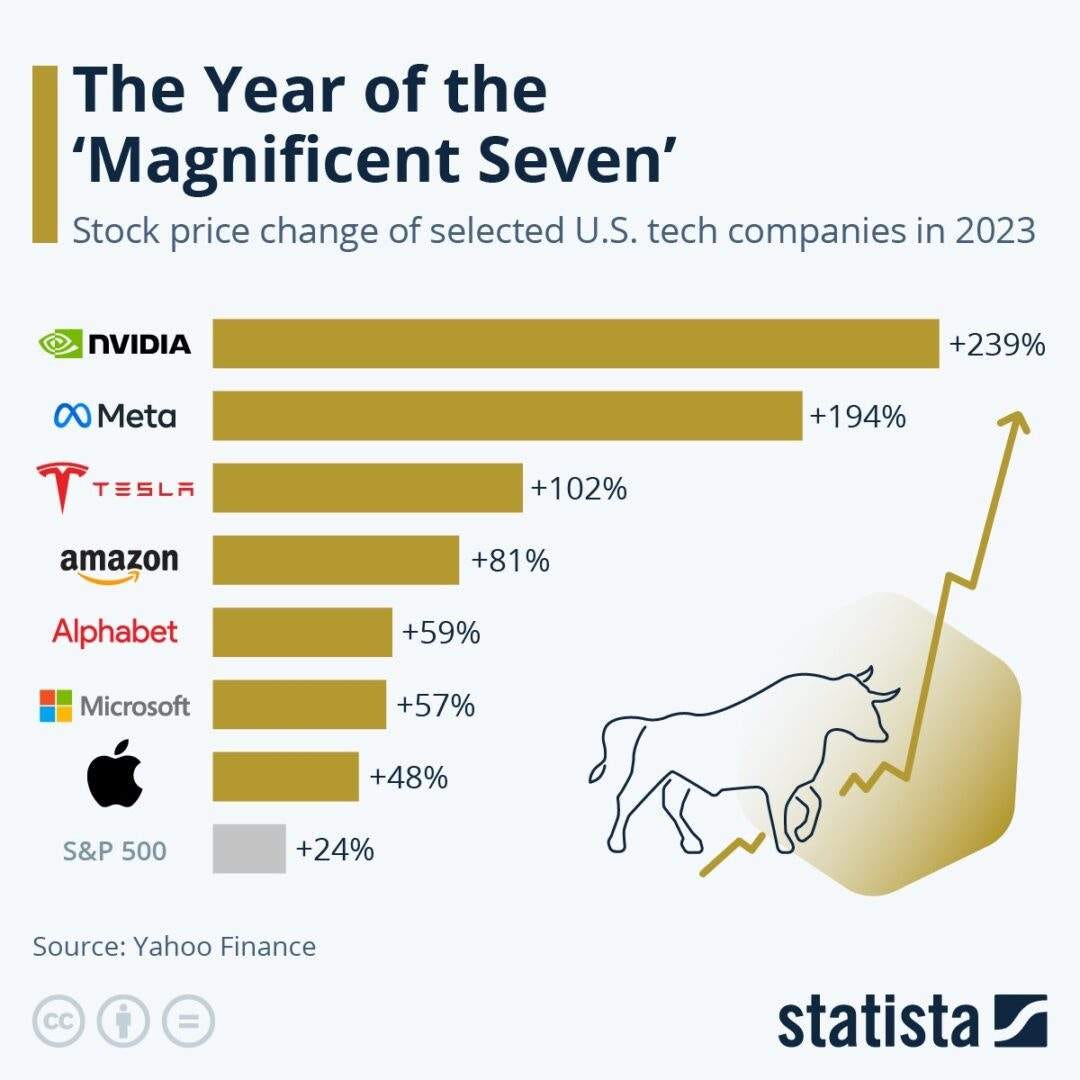

When we talk of popularity, what immediately comes to mind is the fascination with the “Magnificent Seven” stocks over the past few years. The Magnificent Seven are a basket of seven mega-cap stocks that currently dominate the US equity market and include Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla. Five of these seven companies are considered leaders in the technology industry, while the other two, Amazon and Tesla are tech-focused consumer discretionary stocks and are also considered industry leaders. All seven companies are focused on capitalizing on large technology-driven growth trends. They're leaders in the fields of AI, cloud computing, social media, digital advertising, software, hardware, e-commerce, and EVs. These technology trends are driving outsize growth for companies focused on them. Many investors believe this group of mega-cap stocks can continue producing dominant returns. They are capitalizing on technology megatrends that should enable them to continue growing at outsize rates.

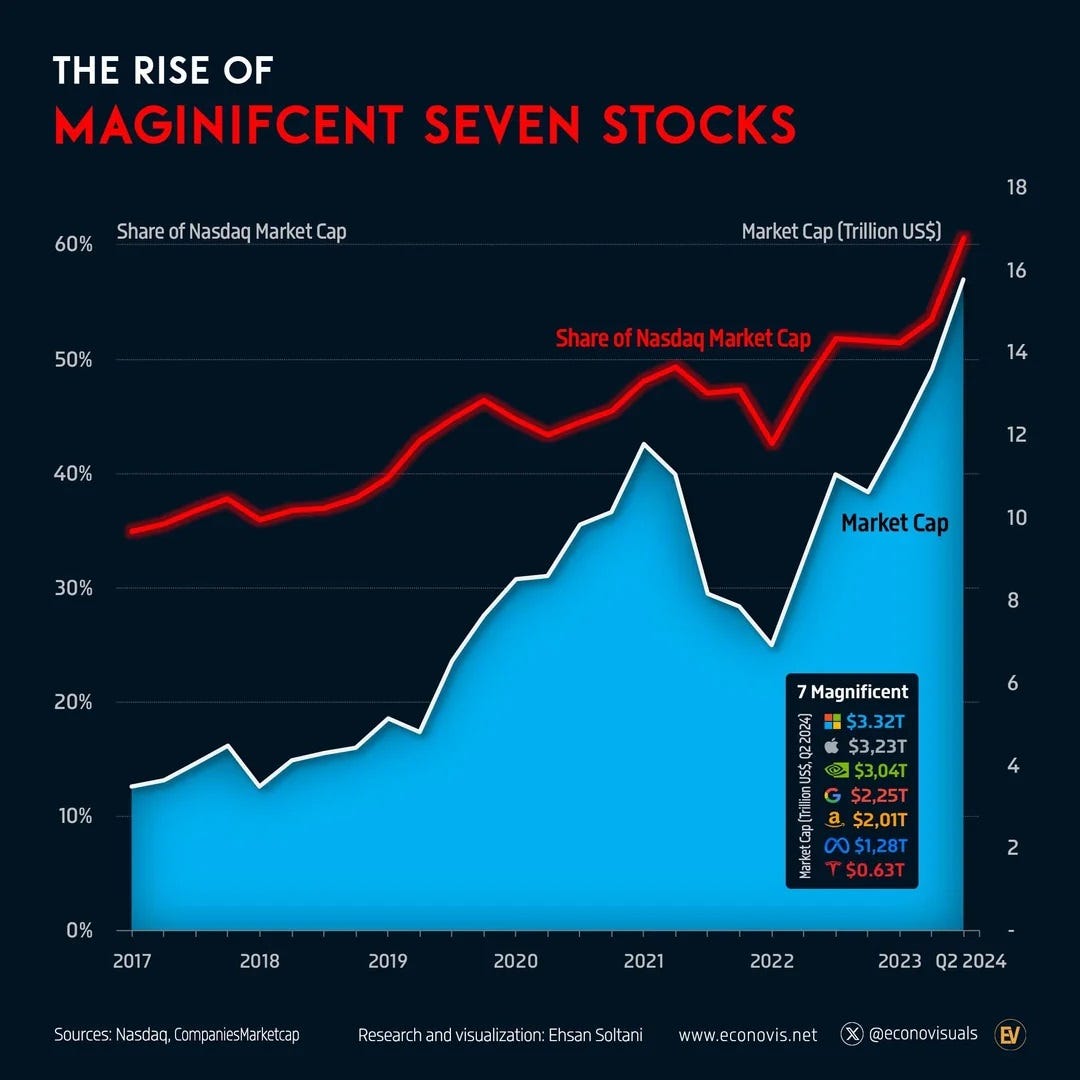

The S&P 500 stock index has been almost totally driven by Magnificent Seven, which have a combined market cap of around $16 trillion. The market prices of the other 493 companies in the S&P index have hardly moved relative to earnings. As of December 31, 2023, these seven stocks cumulatively represented 22% of the Russell 3000 index. From January to October 2023, the Magnificent Seven represented nearly all of the Russell 3000’s gains.

So how does one explain the popularity of the Magnificent Seven?

In 2018, CFA research institute published a book called, “Popularity – A Bridge Between

Classical and Behavioral Finance”. To quote a few interesting points from it:

Popularity is really just another word for demand. Popularity can shift daily or even hourly, but it can also be a relatively stable phenomenon. Some companies are inherently attractive or popular, while others remain uninteresting for long periods of time. Some companies have characteristics that investors seem to like, such as a great story behind them with exciting prospects ahead. Other companies plug along with good results but do not inspire the imagination of investors. These boring or even unattractive companies will have lower valuations, and thus higher costs of capital, than the popular companies.

Popularity is an intuitive and naturally occurring behavioral phenomenon associated with being admired, sought after, well-known, and/or accepted and it is observed in countless settings. From a behavioral literature perspective, the idea of popularity is closely linked to Affect, which is identified as a specific quality of goodness or badness. Affect, or sentiment, is closely linked to the intuitive concept of popularity in that it describes emotional or automatic feelings regarding an asset, investment, or company and the way those emotions influence cognitive decision making.

The popularity approach that emerges from the behavioral finance perspective points to a few important aspects. Investors fail to make nearly instantaneously rational decisions for a variety of reasons: affect, lack of attention, loss aversion, overconfidence, anchoring, mental accounting, and so on. For example, investors who are overly confident may go after the most popular stocks and end up driving the price way up. If these biases are only temporarily connected with a security, they result in mispricing; however, more-permanent biases related to groups of securities can result in long-term premiums. Affect while not the sole driving cause, is a very important element in popularity and exuberance we see periodically.

As a side note, does this complex combination of Narratives, Affect and Popularity explain the underperformance of value stocks? In a 2016 interview, Eugene Fama, who was awarded the Nobel Prize in economics for developing the efficient market hypothesis, said the following:

· “Value stocks tend to be companies that have few investment opportunities and aren’t very profitable. Maybe people just don’t like that type of company. That to me has more appeal than a mispricing story, because mispricing, at least in the standard economic framework, should eventually correct itself, whereas taste can go on forever.”

Final words

Let me end this by talking about the visual I shared at the beginning of this post. It is called, “The Fool and his Money” and was the work of Louis Dalrymple towards the end of the nineteenth century. It shows an oversized man labelled "Promoter" sitting atop a ticker tape machine, holding a large butterfly net into which a throng of investors, some labelled "Broker, Merchant, and Banker", are tossing money in exchange for balloons labelled "Sash and Door Combine Stock, American Beet Sugar Co., Distillery and Warehouse Co. Stock, American Caramel Co., Auto-Truck Co. Stock, Print Cloth pool Stock, Chicago Milk Co., Knit Goods Co. Stock, and International Silver Co." One balloon labelled "Inflated Industrial" has burst.

This was probably an apt description for the times, at the height of gilded age and for a country that had seen a wave of financial crises in the past few decades. But it also an apt one for our own time and all the manias and panics we have seen through the twentieth century. We can probably make sense of the rising and waning popularity and manis through the lens of Narratives and Affect. Understanding forward-looking narratives is part of the art of investing.

· In Science, Progress is Cumulative. In Finance, Progress is Cyclical

Interesting way to capture a persistent trend resulting in diabolical outcomes. My thoughts veer to the recent US of A elections and the results ticking in. Popularity, narrative and Affect has shaped this result. Markets are rewarding it. We have to now wait for the correction. How long? A few years or immediate?

Nicely written article. Informative and insightful, tells me that nothing much has changed in the last 300 years.