Investing Lessons from the Go-Go Years of the 1960’s

In the stock market history, why were the 1960’s called the Go-Go years? One of the reasons was, very often people at the brokerage offices would stand before stock tickers and keep shouting – “Stock X – Go Go Go Stock X”. After three decades, the 1960’s saw the return of euphoria to the stock markets. Scarred and deeply traumatized by the market crash of 1929 and the ensuing Great Depression, an entire generation had shunned the markets, and it was considered a sin and evil. Things started changing in the late 1950’s, driven by a booming economy, low unemployment, and increasing productivity, which continued into the next decade, fuelled by optimism generated by a young Kennedy. It was a decade of extremes and culminated in a whimper with a stock market crash and general mood of social doom and economic gloom.

One of my all-time favourite books is, “Extraordinary Popular Delusions and Madness of the Crowds”, by Charles Mackay. Originally written in 1841, this classic has timeless lessons. One particular sentence keeps coming back to me and there is no better time to revisit it, than now

· “Every age has its peculiar folly—some scheme, project, or phantasy into which it plunges, spurred on either by the love of gain, the necessity of excitement, or the mere force of imitation.”

The Go-Go years had the elements of classic mania and exuberance. There were the growth stocks of Nifty 50, Optimism about the Tronic’s companies, fascination with conglomerates and a boom in the Mutual Funds led by star managers. If that sounds familiar, then to add to it, it was also a period of extreme social strife, stock markets scaling the wall of worry and period of extreme geopolitical tensions driven by the Cold war. It has eerie similarities to our current world, and it makes sense to revisit the Go-Go years and learn from it.

Nifty-Fifty, Growth and Concept Stocks, IPO’s and MF’s

During the 1950’s, the old guard with memories of the Great Depression finally retired and a newer generation showed-up with no memories of the 1920’s and 30’s. By 1969 half of all salespeople and analysts on Wall Street had started in the business in 1962 or later and most of the portfolio managers at various funds and brokerages only saw the good times that began after the WWII. In comparison to the 1920’s, when there were 3 to 4 million people involved with the stock market, the 1960’s estimate was about 31 million in the United States. For this cohort, Nifty Fifty were blue chip stocks with high growth characteristics, which heralded good times and economic boom.

During the 1960s after John F Kennedy became the president, and amidst the growing civil-rights movement, there was a popular belief that the US industry would dominate the global economy and the Nifty Fifty embodied that new sense of economic power. One of the most important reasons for the popularity of these companies was that they had strong business franchises which would earn them high returns on capital for the foreseeable future and were showing above average growth track record. Investment luminaries of the day like, T Rowe Price and Phillip Fisher had advocated investments in ‘growth’ companies to generate above average long-term returns.

The list included the likes of Polaroid, Xerox, McDonald’s, Coca-Cola, IBM and JC Penney, who were the poster boys of the age. The average P/E of the Nifty Fifty was 42x, more than double the 19x P/E of S&P 500. More than 20% of these companies had P/E ratios in excess of 50x earnings by the end of 1972. These were very similar to today’s Mag 7 and were one decision stocks. What happened to them next is a tale as old as time. They got caught in a vortex of euphoria, optimism and enthusiasm and the prices got too far ahead of themselves. They crashed even harder, and the pullbacks were in excess of the market fall. Polaroid dropped 91%, Xerox fell 71% and Avon was down 86%.

To quote the Forbes magazine:

· “The delusion was that these companies were so good, it didn’t matter what you paid for them; their inexorable growth would bail you out. Obviously, the problem was not with the companies but with the temporary insanity of money managers — proving again that stupidity well-packaged can sound like wisdom. It was so easy to forget that no sizable company could possibly be worth over 50 times normal earnings.”

According to John Brooks in his book, The Go-Go Years:

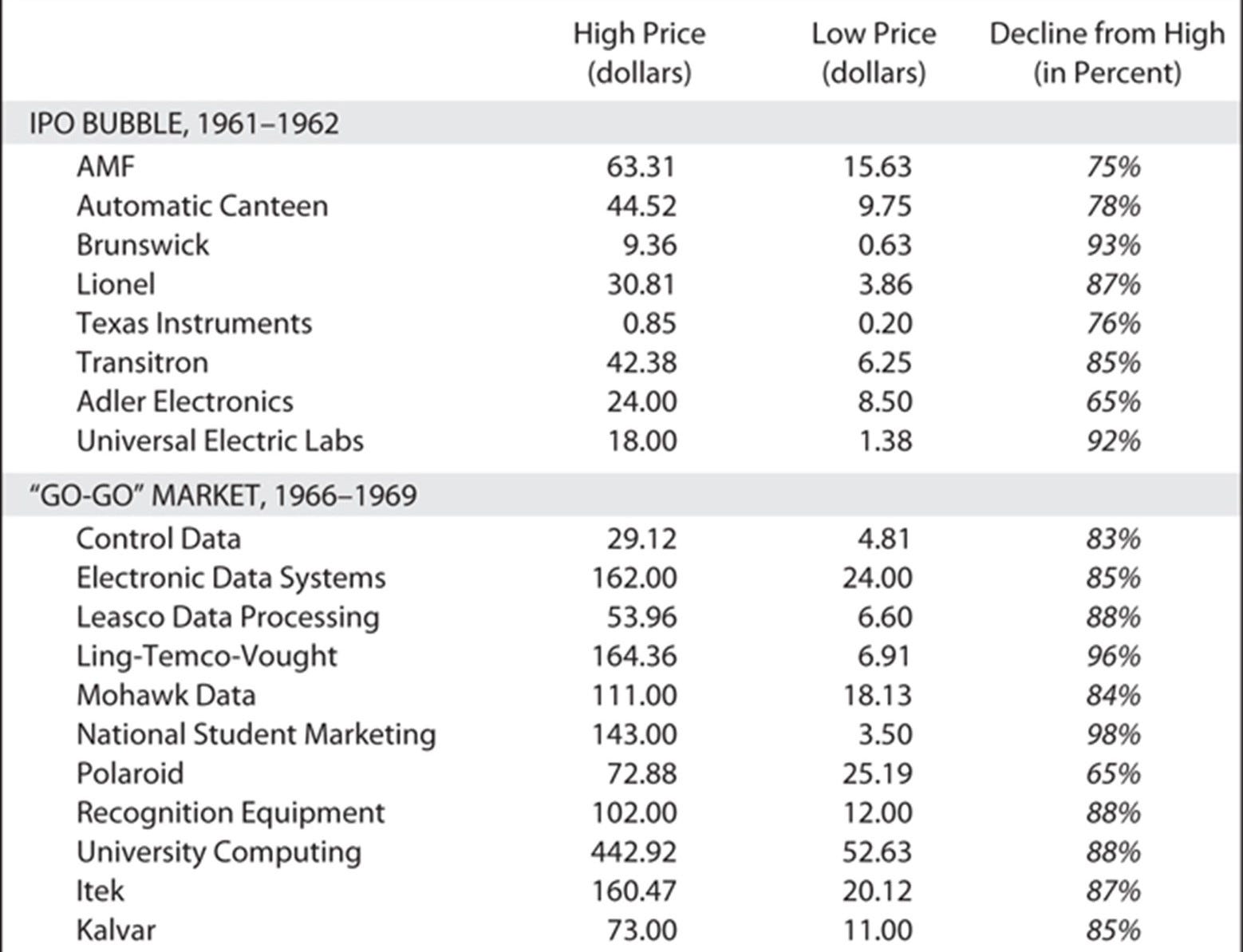

· “A financial consultant named Max Shapiro, writing in the January 1971 issue of Dun’s Review, tried to construct a new yardstick more appropriate to the new situation. As a rough modern counterpart to what the Dow represented in the old days, Shapiro made a list of thirty leading glamour stocks of the nineteen sixties — ten leading conglomerates including Litton, Gulf and Western, and Ling-Temco-Vaught, ten computer stocks including IBM, Leasco, and Sperry Rand, and ten technology stocks including Polaroid, Xerox, and Fairchild Camera. The average 1969-1970 decline of the ten conglomerates, Shapiro found, had been 86 percent; of the computer stocks, 80 percent; of the technology stocks, 77 percent. The average decline of all thirty stocks in this handmade neo-Dow had been 81 percent.”

More recently, Ben Carlson published a similar analysis using Fama/French data to get a better sense of how this time frame played out.

Apart from the Nifty Fifty there was the “Tronics” boom. This was the age of transistor and the beginning of the space age. Anything and everything related to Electronics caught investors fancy. This was considered a new era in which the stocks of electronics companies making products like transistors and optical scanners soared. It was called the tronics boom because these soaring stocks usually had some form of tron or tronics in their name: Astron, Dutron, Vulcatron and Transitron and "onics" like Circuitronics, Supronics and Videotronics, as well as one company that, for good measure, put together the winning combination Powertron Ultrasonics.

Like the familiar story during dotcom and in today’s AI mania, the demand for such companies was huge, but the IPOs were relatively thin, so that stock prices would soar at the launch. Investors argued that "tronics" stocks couldn’t be valued according to traditional methods because they represented a whole new era of the economy that was nothing like the past. This time was different, and the buyers of these issues didn’t really care what the companies made, so long as it sounded electronic. Promoters built narratives about the potential of the revolutionary technologies and unending prospects and growth and eager to satisfy the insatiable thirst of investors for the space-age stocks, they created more new issues in the 1959–62 period than at any previous time in history. As a result, stocks soared to multiples of 50, 100 or even 200 times earnings. Many of the IPO prospectuses of the period contained the following type of warning in bold letters on the cover.

· Warning: This company has no assets or earnings and will be unable to pay dividends in the foreseeable future. The shares are highly risky.

But in late 1962, "tronics" stocks and other growth issues came crashing down in a massive sell-off. This was followed by the crash of the computing stocks later in the decade.

Even though the modern mutual fund was invented in 1924, by 1954 there were only about 100 in existence. Back then the investment management industry was a sleepy business for the uber-elite such as those that went to Ivy Leagues and then used their connections to invest in a fund. Mutual Funds became mainstream during the 1960’s go-go years and Gerald Tsai became the poster child of this era. He was the de-facto pied piper of this era and was to become the original celebrity fund manager. In his book, The Making of a Market Guru, Ken Fisher names Tsai as one of the flamboyant and famous top-performing “go-go” mutual fund gunslingers of the mid-1960s. The Fidelity Investments performance fund which he created in 1957 was the first of its kind investment vehicle for general public and it grew 27-fold in terms of assets under management (AUM) in eight years by 1965.

Tsai was a famed practitioner of what later came to be named "momentum investing". He would buy stocks with positive price and earnings trends and sell when the momentum displayed signs of subsiding. Tsai was a shrewd and decisive stock picker and went hunting for short-term appreciation. He concentrated on a few stocks that were then thought to be outrageously speculative and unseasoned for a mutual fund. People were dazzled by his swashbuckling forays into the glamour stocks of the day, like Polaroid and LTV, which seemed only to go up and up, and his seeming ability to time the market’s every move His method was a stark novelty to the existing value investors. He ignored business fundamentals and intrinsic value of a stock, and focused on stock charts and technical indicators, which resulted in focus on glamour names and price momentum. His annual portfolio turnover generally exceeded 100%, a rate unheard of in institutional circles then.

Though he faced a setback in 1962, when the market dropped 25%, Tsai held on and the market picked up and along with it the fund’s performance. The bull market was intact, and his swift and nimble stock moves were timed to perfection. His popularity as a fund manager can be gauged by simple numbers: In 1946, there was only $1.3 billion invested in mutual funds, but by 1967, the amount reached to over $35 billion. Money flocked to Tsai’s fund and in an era of anonymous money managers, he was the exception. The Fidelity fund he managed grew from $12.3 million in 1959 to $340 million in 1965.

The end game began when Tsai started the Manhattan Fund, which when open for subscription generated 10x more than he anticipated - $247 million in capital, representing what was at the time the biggest offering in mutual fund history. The Manhattan Fund began trading in February 1966, the very same month the Dow Jones made its high of the decade. The following two years were of average returns for his fund, before his legendary performance vaporized. By July 1968, the Manhattan Fund was the sixth worst-performing fund in the country. Probably sensing something, Tsai sold the fund for $30 million to the insurance company, C.N.A. Financial Corporation, post which the fund crashed spectacularly, losing 90% of its value in the years following the market crash of 1969.

Warren Buffett started experiencing a frothy market since early 1968 and for him, Investors were paying less attention to underlying company’s earnings and more to the surging stock prices. He wrote:

· “I believe the odds are good that, when the stock market and business history of this period is being written, the phenomenon described in Mr. May’s article will be regarded as of major importance, and perhaps characterized as a mania. You should realize, however, that his “The Emperor Has No Clothes” approach is at odds (or dismissed with a “SO What?” or an “Enjoy, Enjoy”) with the views of most investment banking houses and currently successful investment managers. We live in an investment world, populated not by those who must be logically persuaded to believe, but by the hopeful, credulous and greedy, grasping for an excuse to believe.”

Finally on May 29th, 1969, Buffett ‘threw the towel’ and brought the curtains down on his investment partnership.

· The investing environment I discussed at that time (and on which I have commented in various other letters has generally become more negative and frustrating as time has passed. Maybe I am merely suffering from a lack of mental flexibility. (One observer commenting on security analysts over forty stated: “They know too many things that are no longer true.”)

So, what led to the bursting of the Go-Go years bubble? While the market crash started in 1969, the bear market peaked in 1973 and 1974. Some of the underlying reasons were:

· Overvalued Stocks.

· High crude oil prices post the Arab Oil embargo.

· Watergate scandal which involved President Richard Nixon.

· End of the Bretton Woods monetary system after the unsustainable debt burden of the US following the Vietnam War.

· Increase in Inflation and Interest Rates.

· Rising unemployment which reached 6% by the end of 1970.

“Bubbles and Crashes” - Elementary, My Dear Watson

Reading about the Go-Go years gives a sense of Déjà vu. I have lived through the dot com bubble and the characteristics were all similar and familiar. You would be forgiven if the same feeling crops up today. All the usual suspects are there: Growth and concept stocks and add meme stocks, momentum investing, star fund managers and the absolute disregard for the underlying basics and gathering economic and social storm clouds.

History might not repeat, but it definitely rhymes. History is a veritable museum of human follies and foibles, that seem to have a similar pattern. The manias, panics, bubbles and crashes separated in time and space, all seem to have similar patterns and occur in the context of identical backgrounds. In todays’ world when all this can be accessed at the click of a few buttons, why is it that we never seem to learn?

What makes these Bubbles and Crashes recurring? Are there patterns one can decipher?

In their book, “Bubbles and Crashes – The Boom and Bust of Technological Innovation”, Brent Goldfarb and David Kirsh, analyze fifty-eight major innovations appearing between 1850 and 1970 that may or may not have led to speculative activity. They identify two common themes that underly all the bubbles,

• Uncertainty and Narratives

• Novices and Biases

Every Innovative Technology in history has been associated with lots of uncertainty. Which are the firms and who are the people, who can take advantage of this and benefit from it? Who will capture the value and who will profit? The underlying uncertainty is an integral part of any emerging technology.

This uncertainty is a fertile ground for imagined futures. Fecund minds weave narratives and tell stories that sometimes are plausible, but for most stay well and truly in the realm of incredulous. But we humans are not wired for data, our brains are wired for stories. Stories and narratives captivate us and capture our imagination. They let us imagine a desired future and break free from the humdrum of the present. They offer the lure of escaping to that desired world. Narratives around Business Models, Potential Revenues and Disruption capture our attention and align them to our beliefs.

Every bubble is characterised by the presence of novice or unsophisticated investors. During the dotcom boom, it was the millions who found investing liberating through E*Trade and today it is the Robinhood and Reddit Generation. They tend to be overoptimistic and overconfident, leading to poor buying decisions, increasing the demand for risky assets. These “noise traders” are overly bullish, inexperienced, and less financially literate. They are easy prey to narratives about potential opportunities that are new and seem exciting.

So, is there a way to identify these bubbles? Yes. Goldfarb and Kirsh provide a checklist. If the sum of all your answers is affirmative, you are in a bubble. Avoid these and save yourself the agony and the loss

• Story: Is the story particularly compelling or sticky?

· Use: Is the story about something that you are familiar with in terms of use or imagination but in an area that you fail to understand the business well?

· Novices: Are there other naive investors in the market? Who is investing in this technology?

· Pure play: Is there a stock that is believed to track the fortunes of the technology directly?

• Competition: Does the narrative ignore future competition?

· Business model: Are there a variety of stories about how money will be made commercializing the new technology?

· Narrative accelerator: Did something or somebody turbocharge the narrative?

· Leverage: Are investments significantly leveraged? Do intermediaries play a large role?

The most successful long-term investors are those who avoid becoming mesmerized and attached to current and trending narratives. They look beyond the weekly and monthly action in the markets. They tend to step back and reflect, understand and analyse the megatrends and larger cycles that drive a multifaceted global economy. There are always bull markets with-in bear markets and vice versa. While one bull market might be ending, another is likely to begin elsewhere, in another sector or probably in another class of assets.

· In Science, Progress is Cumulative. In Finance, Progress is Cyclical

The last three lines resonate a lot…

Nifty 50 in 70s and in the Cold War era? Did I miss a wise metaphor or comparisons in parallel but distant timelines? (I really didn’t understand it. I first thought maybe Nifty 50 is old enough and it tracked US companies earlier).