A Perfect Storm - Panic of 1907 and Birth of the Federal Reserve

It was a perfect storm. Two earthquakes, a real one in San Francisco and the other in the realm of Finance in New York, though seemingly unrelated would play a role in fomenting a crisis that would have long-lasting consequences for the monetary policy of the United States. The Panic of 1907 was 20th century’s first global financial crisis. It was a six week stretch of run on Banks and Trusts in New York City and elsewhere in October and November of 1907. Out of this panic was born, the Federal Reserve system.

The trigger for the panic was a failed speculation that caused the bankruptcy of two brokerage firms, but seen in a larger context, the event and the shock that set in motion a further chain of events to create the Panic was the earthquake in San Francisco in 1906. The devastation caused by the quake, not only ruined the city, but also drew gold out of the world's major money centres. The ensuing liquidity crunch led to recession in the US starting in June of 1907. A recession got transformed into a contraction which lasted 15 months and saw GDP decline by an estimated 30%, the stock market fell 50% and the unemployment rate went from 2.8% to 8%. It caused a severe distrust in the financial system as banks failed every day and in October and November of 1907, 25 banks and 17 trust companies went bust. In the US, which did not yet have a central bank, it took a John Pierpont Morgan to more or less single-handedly save the US banking system by being a one-man central bank.

The Panic of 1907, a book by Robert Bruner and Sean Carr, is a lively and educating account of one of the biggest and most influential financial crises in history and lays out the bigger picture. They identify 7 reasons why the Panic of 1907 was a perfect storm for bank runs and a massive financial crisis:

1. Complexity

2. Buoyant growth

3. Inadequate safety buffers

4. Adverse leadership

5. Real economic shock

6. Undue fear, greed, and other aberrations

7. Failure of collective action

“Information problems are central to an understanding of financial crises. Over time, innovation in financial institutions, markets, instruments, and processes breed growing complexity in the financial system. Complexity makes it difficult for decision makers to know what is going on. The resulting information asymmetries spawn problematic behavior, arising from adverse selection and moral hazard. Information problems contribute to the overoptimism associated with buoyant business expansion and the tendency of debtors to over lever and of lenders to ignore prudent credit standards.

The architecture of a financial system links institutions to one another in a way that enables contagion of the crisis to spread. Trouble can travel. Safety buffers (such as cash reserves and capital) may prove inadequate to meet the coming crisis. Then, one or more shocks hit the

economy and financial system, causing a sudden reversal in the outlook of investors and depositors. Confusion reigns. Public sentiment changes from optimism to pessimism that creates a self-reinforcing downward spiral. In the vicious cycle, bad news prompts behavior that generates more bad news. Collective action proves extraordinarily difficult to muster

until the severity of the crisis and the insight and information held by a few actors prompts mutual response.”

Most crises are preceded by an external shock to the system that acts as a catalyst for the coming crisis. These shocks are rarely predictable, and that unknowable or unforeseeable element is the catalyst that will set it off. It could be wars, natural disasters, the price of crude oil, geopolitical turmoil in the Middle East or an economic or political crisis in the European Union. To start with, the catalyst may seem unrelated to financial markets, but the ripple effects quickly become obvious.

In the case of The Panic of 1907, the event that acted as a shock and catalyst was the San Francisco earthquake of 1906.

On the morning of April 18, 1906, at 5:13 AM, an earthquake registering 8.3 on the Richter scale hit San Francisco hard, when the northernmost 296 miles of the San Andreas Fault, from the California town of Hollister to Cape Mendocino, ruptured. The shaking lasted fifty-five seconds and the eastern side of the fault had moved to the southeast by twenty-four feet. It was followed by massive fires that blazed for four days and nights, destroying entire sections of the city. Eventually, the earthquake and ensuing inferno destroyed 490 city blocks, some 25,000 buildings, forced 55–73% of the city’s population into homelessness, and killed almost 3,000 people.

While the earthquake by itself was devastating enough, the fires that resulted from broken gas lines made it worse and because the quake had also broken the main water lines, there was no water supply to fight the fires. After the firefighters pumped the sewers dry in an attempt to stop the flames, they sought help from the army battalion that was stationed at Presidio, the military fort overlooking the entrance to San Francisco Bay. Lacking water to fight the fires, the soldiers used dynamite to collapse buildings into heaps of rubble that they hoped would serve as firebreaks, but instead, these explosions started new fires. There was another unique factor that made the fires worse. Though almost no one in the city was insured against earthquake, everyone was insured against fire as many of the buildings were constructed with wood. Having your house destroyed by fire was the only way to get an insurance payment, so in the aftermath of the quake, citizens whose houses were heavily damaged by the quake, set them on fire.

In the early 20th century, another oddity was that most of the fire insurance in San Francisco was done by British insurance firms. According to historians Kerry Odell and Marc Weidenmier, “Endowed with an excellent natural harbour and easy coastal and river access to the agricultural and natural resource riches of the west, San Francisco had developed strong economic ties to other countries, particularly to Britain. Most of the wheat exported from the west coast and bound for England was financed through San Francisco, and a sizable number of London banks had offices in that city. At the same time, other British financial institutions sought to expand their business in the area. Prominent among these were the British fire insurance companies.”

Damage from the earthquake and fire was estimated to be between $350- $500 million, or 1.3 to 1.8 percent of US GNP in 1906. Because British companies underwrote the majority of the city's fire insurance policies, an estimated £23 million or $108 million at the time, worth of insurance claims were soon presented in London. The Financial Times called San Francisco a $200 million “ash heap”, as London-based insurers began loading gold on ships and sending them to San Francisco as even more claims continued to pile up. Thirty million dollars in gold was sent in April, with more sent during the summer and $35 million worth sent in September alone. The amount of gold sent to San Francisco to settle earthquake claims was equal to 14 percent of Britain’s total stockpile. Operating under the gold standard, this sudden outflow of gold from London was such a massive shock to the British financial system and the magnitude of the resulting capital outflows in summer and autumn 1906 forced the Bank of England to undertake defensive measures to maintain a fixed sterling/dollar exchange rate. The central bank responded by raising its discount rate two hundred-fifty basis points between September and November 1906 and by pressuring British joint-stock companies to stop discounting American finance bills for the next year. Actions by the Bank of England attracted gold imports and sharply reduced the flow of gold to the United States. By June 1907, the United States had fallen into one of the shortest, but most severe recessions in American history.

Into this fragile economic situation came the end of a speculative mania and unravelling of shadow banking system in the form of Trust Companies.

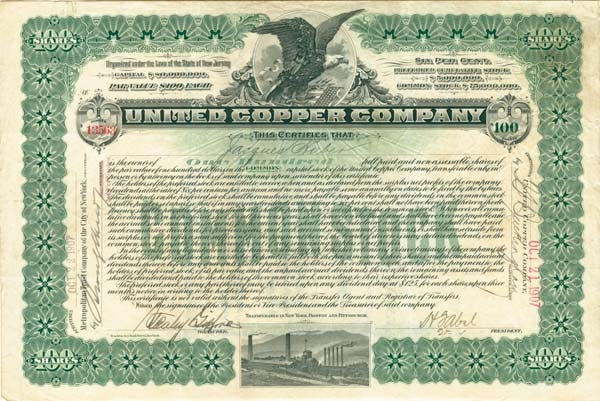

Augustus Heinze was a business magnate in Montana, who made his fortune as a mining promoter, and earned a reputation as a combative businessman who was unafraid of taking large copper trusts to court. This manifested in his battle against Amalgamated Mines. He owned a copper mine which happened to be located near Amalgamated Mines and Heinze claimed that veins of copper emanating from his mine extended beneath the land owned by Amalgamated, and even though it was their land, he claimed the rights to the mineral deposits. After a lengthy court fight, he reached an out of court settlement of $25 million. Heinze then took his massive newfound fortune to New York and aspired to become a banking tycoon. Early in 1907 he established relationships with two of the city’s powerful bankers: E. R. Thomas and C. F. Morse. In those days, it was common practice to expand one’s banking empire through “chain banking,” which involved buying stock in a given bank, and using that stock as collateral to borrow money, and then using that cash to buy stock in yet another bank or trust. Soon Heinze was in control of several banks and was on the board of directors of eight banks and two trust companies. Morse himself was a director of seven New York City banks, three of which he controlled.

Then Heinze hit upon a scheme he thought could substantially add to his fortunes. He wanted to corner the stock of United Copper and because he already owned a substantial block of United Copper stock, a successful attempt would push the price higher and prove very profitable. His brother Otto was the main brain behind the idea of cornering United Copper. Because the stock had already been so heavily shorted, Otto believed that they were in a superb position to put the short sellers in a very uncomfortable spot, by buying stock in the open market, as there were very few shares locally available on the market. He also believed that most of the stock that the short-sellers had borrowed was, in fact already in Heinze’s possession, and that the short-sellers would have to purchase shares directly from Heinze in order to close their positions. On Monday, October 14, 1907, they started buying United Copper in the open market, pushing the price from $39 to $52 in a single day. The next day, Otto issued a demand from his brokerage, Gross & Kleeberg, that all borrowed shares be returned. The hope at this point was that short sellers would scamper around the city, find absolutely no stock to buy, and helplessly show up at Gross & Kleeberg to be told what exorbitant price they would have to pay. Instead, there was ample available supply of the United Copper stock in the market and the short sellers were able to cover their positions at regular market prices. Once the market realized the game that Heinze was up to, the share price started falling. By the end of the Tuesday, it had fallen to $30 and by Wednesday shares were selling for $10. The market had called their bluff, and the Heinze’s were ruined.

The first casualty of this failed scheme was the State Savings Bank of Butte, Montana, which was owned by Augustus Heinze. The bank held a large amount of United Copper stock as collateral for some of its lending, and with the collateral dramatically devalued, the bank declared its insolvency. At this point, any financial institution associated with Morse or Heinze became immediately suspect in the public’s eye. One of the banks, Mercantile National, insisted that Heinze resign and he did. In spite of this, fearful depositors rushed to the Mercantile to withdraw money as fast as they could. Other banks, including New Amsterdam National and National Bank of North America because of their association with Morse, were crowded with people demanding their money back. To calm people’s nerves, the New York Clearing House, which was a consortium of the city’s banks, demanded that both Morse and Heinze resign all of their banking interests, but this had no impact on public sentiment and the run on the banks continued.

The final straw in the bank run saga was the run on the investment trusts in New York. These trusts were financial institutions that took deposits but did not have the kind of regulation banks had. They still provided almost every function that banks did apart from issuing notes. They were the shadow banks of 1907. These trusts could buy/sell stocks and corporate debt, underwrite/distribute securities, receive deposits, and make loans. Yet, despite all their similarities with banks, they were excluded from the New York Clearing House and could not access the one institution able to throw them a lifeline in times of crisis. What added fuel to this shadow banking fire was the fact that these trusts had no mandated reserve requirements, making them even more fragile. The contagion spread and led to a run on the second largest trust in New York, the Knickerbocker Trust, after an announcement by the National Bank of Commerce that it would not serve as Knickerbocker’s clearing agent. Because of their low cash reserves, the Knickerbocker Trust was forced to close its doors on October 22 as they ran out of funds after seeing withdrawals of $8 million in three hours by frantic customers. The run on Knickerbocker spooked the public, and led to an outbreak of runs on other investment trusts. Other trusts, fearing the possibility of runs, began to call in loans and liquidate assets to build up their cash reserves. These efforts severely disrupted stock and bond markets, where securities dealers faced difficulties in financing the holding of their inventories. Liquidity vanished from the market and asset prices went into a free fall.

Into this chaotic situation entered JP Morgan.

We take the Federal Reserve for granted, but in 1907, US did not have a central bank and the Federal Reserve was a few years into the future. Through the entire crisis, the one man in the middle was JP Morgan and without a central bank to turn to, the financial industry relied on Morgan’s financial resources, connections, public pronouncements, and force of will, to weather the storm.

The day before the Knickerbocker Trust closed doors, they out of desperation had reached out to Morgan and he understood the criticality of the situation and the impact if the second largest trust company went under. Morgan pledged $12 million in support to shore up the bank’s diminishing cash reserves. Next day people still panicked and withdrew their cash, unaware of Morgans pledge. At this point, fears of financial contagion began to spread. An immediate effect of the growing fear was that interest rates for very short-term loans or call rates skyrocketed from 6 percent to 60 percent. Very few banks were willing to lend in such an environment, and those that were willing wanted very high return. As the call rates moved from 60 to 70 percent and later 100 percent, liquidity in market completely evaporated. Stock prices started crashing and on October 24, Ransom Thomas, the president of the New York Stock Exchange went to Morgan’s office to inform him that they were going to close the stock exchange early. Morgan understood that this would only add to the panic.

Morgan gathered the presidents of the city’s banks at his office and informed them that unless they raised $25 million among themselves to provide to the exchange, 50 brokerage houses would fail immediately. The deal was done in 10 minutes, and the money reached the market half an hour before the closing bell. Morgan also tried to shore up confidence by making a rare statement to the press: “If people will keep their money in the banks, everything will be all right.” The panic did not subside the next day and Morgan again had to lean on bank presidents to loan the exchange an additional $10 million. Morgan knew he could not sustain this kind of cash infusion indefinitely, and that Friday he organized two public relation committees, one working with the clergy, to calm their congregations on Sunday, and the other with the media, to explain the financial backing Morgan and his men were providing and why it would stabilize the situation. Despite all this effort, the City of New York informed Morgan a couple of days later that if it did not receive $20 million in emergency funding within the week, it would also go bankrupt. The mayor of the city appealed to Morgan directly, who quietly agreed to purchase $30 million in city bonds.

One of Morgan’s final acts was in yet another looming crisis in the form of the Tennessee Coal, Iron, and Railroad Company (TC&I). Moore & Schley, one of the largest brokerage firms in the country, had borrowed heavily during the crisis, and the collateral used for the loans was their substantial holdings of TC&I stock. The stock itself suffered heavily and lost a lot of value during the panic. This put Moore & Schley at risk as their loans would be called due to the deteriorating conditions of their collateral. If the loans were called, Moore & Schley would have to liquidate their TC&I position swiftly, which would not only crash the stock but cause extensive collateral damage to other stocks in the market as well. Morgan came up with a plan that not only saved TC&I, but also benefitted his financial empire. His company US Steel decided to acquire TC&I at a price of $90 per share, which while being a positive for US Steel, would also eliminate the risk of Moore & Schley’s prospective collapse and further worsening the financial contagion.

(I have intentionally not gone into details Theodore Roosevelt’s crusade against big business and the Sherman Anti-Trust act, and the negotiations between the government and Morgan for US Steels acquisition of TC&I. It would have made the blog post even longer 😊)

President Woodrow Wilson signed the Federal Reserve Act in December 1913, culminating three years of discussion and debate over the development of a central bank.

After the panic of 1907, although the bankers of the city, and the populace in general, were grateful for Morgan’s support and leadership, it had become apparent that relying on a single wealthy individual to shore up the collective financial health of the nation put the country in a vulnerable position. The next year, in May 1908, Congress passed the Aldrich-Vreeland Act to establish the National Monetary Commission. Its purpose was to investigate the causes of the panic from the year before and explore ways to prevent such a panic in the future. The chairman of the committee, Senator Nelson Aldrich went to Europe, a continent with established central banking system, to study their central banks operations and the study lasted for two years. He was convinced of having a central bank and believed that the series of problems that occurred in 1907 could largely be attributed to a lack of credit. Without a central bank to turn to, the city’s banks had to rely on the deep pockets of Morgan and his associates. Having an industry rely on its own internal resources seemed shortsighted.

On his return in November 1910, Aldrich called for the now famous meeting at the Jekyll Island Club, located off the Georgia coast. It was attended by Aldrich and senior officials of the Treasury Department, Hendry Davison of JP Morgan, Paul Warburg of Wells Fargo, and others from First National Bank of New York, and Kuhn, Loeb & Company. The men decided that the best course of action was for the United States was to create its own central bank, with the banks themselves holding key spots on its committees. The National Monetary Commission submitted final report in January 1911. The recommendations were debated for a full two years and finally on December 23, 1913, Congress passed the Federal Reserve Act, which President Woodrow Wilson signed on the very same day, and the Federal Reserve System was born.

Here is why the Fed could create a depression:

https://arkominaresearch.substack.com/p/why-fed-could-create-depression?r=1r1n6n