25 years after LTCM debacle – Lessons for today.

September 23rd, the day I am writing this marks the 25th anniversary of the official downfall of Long Term Capital Management (LTCM). For many of my generation, who were still trying to figure out what the Asian financial crisis of the preceding year was about, this was an absolute bolt from the blue. In many ways it was a baptism by fire into the financial markets for me and many others. It was the first time, the words: Hedge Fund, Derivates, Swaps, Options, Leverage and Liquidity became a part of the lexicon. It has all the hallmarks of a gripping story. Started by a legendary bond salesman and two Nobel laureates, based on fail proof mathematical models, funded by enormous amounts of leverage, this was supposed to overturn conventional notions of finance, risk and returns on its head. But it ended being a saga of dazzling success followed by perilous downfall, destruction of enormous wealth, serious risk of contagion and unintended consequences. 1998 was a pivotal moment, the Greenspan Put officially making a ultra loose monetary policy a norm.

It was not supposed to be like this. What happened and what are the lessons we could have learnt?

A recap pf the LTCM story

· LTCM was a hedge fund incorporated in 1994. The founding team consisted of some elite names, John Meriwether, former head of bond trading at Salmon Brothers and two Nobel Laureates, Myron Scholes, and Robert Merton.

· Its primary goal was to use trading strategies based on arbitrage to exploit market inefficiencies. This philosophy was rooted in the belief that markets are efficient in the long run but can exhibit discrepancies in the short term and these discrepancies could provide opportunities for high returns.

· LTCM’s business model was based on a concept called convergence trading, which involved buying undervalued securities and selling overvalued ones, expecting that prices would eventually converge to fair values. This was executed using sophisticated mathematical models and substantial leverage.

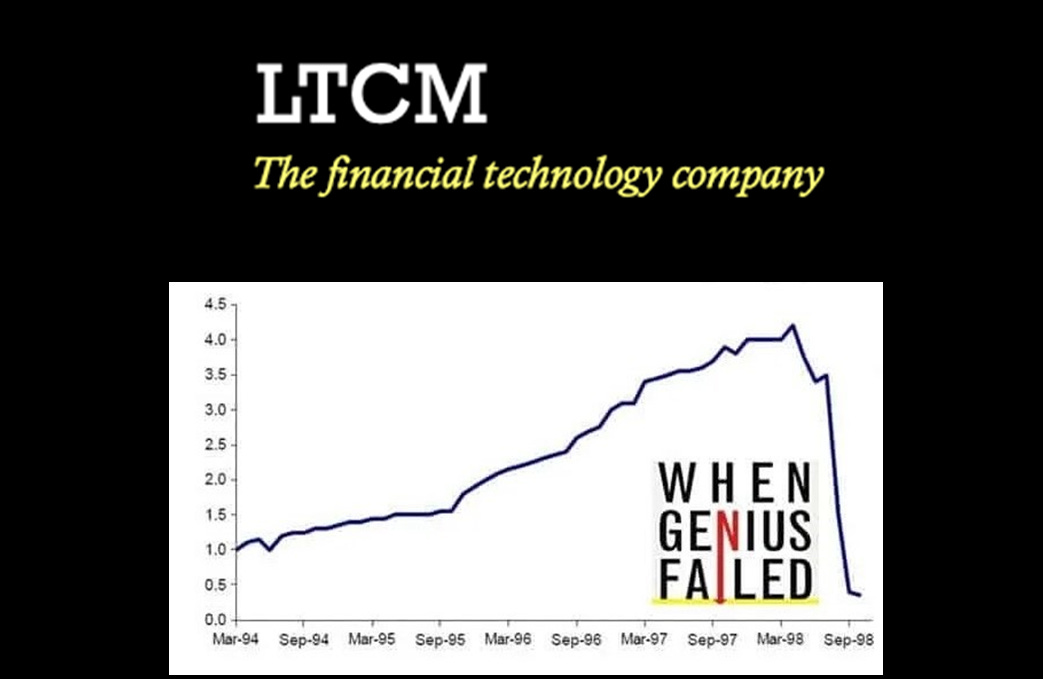

· LTCM's primary strategy was to make money through arbitrage in bonds, which involved taking advantage of small price differences in bonds with similar characteristics but slightly different prices. They would purchase undervalued bonds and short the overvalued ones, expecting to profit when the prices converged. In its early years, LTCM experienced phenomenal success, having returned 40% after fees in 1995 and followed by returns exceeding 40% and 20% in 1996 and 1997. Their capability to exploit the mispricing between Italian and German bonds, led to a significant profit in 1994. LTCM was also a significant player in the derivatives market and its trading strategies often involved complex derivative positions in interest rate swaps and options.

· LTCM’s problems started in July 1998, but were aggravated over the next couple of months. The final nail in the coffin came with Russia's default on its sovereign debt, which sent shockwaves through international financial markets, leading to a flight to quality. This completely disrupted LTCM’s strategy, which was predicated on stable market conditions and convergence of prices. LTCM reported huge losses and eventually went kaput.

So, what led to the spectacular reversal of fortunes?

Misunderstanding Risk

· Risk is measurable uncertainty while uncertainty is immeasurable risk.

What is Risk? LTCM’s strategies were based on the concept of “Value at Risk (VaR)”, probably the most damaging concept ever formulated in the finance world. VaR can be defined as the worst loss that can happen under normal market conditions over a specified time horizon at a specified probability. VaR models along with other financial risk measurement tools assume that asset prices follow a “Normal” distribution, or the classical bell curve. According to VaR models used by LTCM, the events that could cause their demise had one in a few million probability and wouldn’t occur in any predictable or foreseeable future.

Unfortunately, it is well known and proven that financial assets do not exhibit normal distributions. They are subject to what are called “Fat Tail Events” or “Black Swans”. What will cause you to lose billions instead of millions? Something rare, something you’ve never considered a possibility and they take place far more frequently than most of us are willing to contemplate.

For LTCM, it was a perfect storm. A combination of events that did not exist according to their mathematical models, happening at the same time:

· 1997 was the year when the Asian financial crisis first struck. Many East and Southeast Asian countries, whose pegged currencies had become grossly overvalued saw the value of their currencies plunge under relentless speculative attacks, many losing more than half their value. Years of explosive growth, driven by foreign inflows and leverage came to an abrupt halt, when the same foreign capital fled to safer havens of liquid markets in US and Europe. As a result, spreads between zero-risk treasuries and riskier mortgages, investment grade corporate and junk bonds widened drastically. LTCM which gambled on spread convergence was caught on the wrong side of the equation. Capital flow reversals also heightened volatility on stock markets which collided with LCTM long established belief in volatility subsiding and reverting to lower historical levels. When the turmoil of Asian stock exchanges spread to Russia in the summer of 1998 and reverberated through major financial centres, LTCM’s extensive short positions in long dated options on stock indices such as S&P 500 and CAC 40 became deep “out-the-money” prompting massive margin calls.

· Compounding these problems for LTCM was an incident unrelated to the market fluctuations, but nevertheless a key one. In the spring of 1998, Travelers Group and Citicorp announced a merger. As part of the deal, Travelers inherited Salomon Brothers, a bond arbitrage house which mimicked many of LTCM’s convergence trades. Travelers’ CEO Sandi Weill had misgivings about Salomon’s business model which he considered as pseudo-scientific gambling and decided to pare down its positions. As a result, many of LTCM’s outstanding convergence trades involving fixed income securities and interest rate swaps were severely disrupted by Salomon Brothers hurried exit. Because Salomon was on the same side of many of LTCM’s trades its sales of illiquid positions exacerbated spreads rather than pushing them towards convergence. As a result, LTCM experienced 1998 one of its worst months in July 1998, which brought the fund down by 14%.

· In August 1998 Russia devalued the rubble and declared a moratorium on its government debt. The default roiled world financial markets as Russian banks and financed companies claimed “force majeure” to default on derivatives contracts which left many western financial institutions exposed to major losses. LTCM had a sizeable position in rubble-denominated Russian government bonds and this exposure was hedged by a matching amount of rubble forward sales. Unfortunately, when Russia defaulted on its bonds, it severely damaged the Russian banks which defaulted on their forward contracts. The Russian bear had stripped off LTCM’s hedge and left it naked!

Forget all three events happening together, neither one of them in isolation could have been modelled by any amount of mathematics. Radical uncertainty is everywhere in our world and LTCM story highlights the limitations of models in getting to grips with the phenomenon.

In their book “Radical Uncertainty”, John Kay and Mervyn King argue that,

“It is a mistake to believe that we can depend on models. Models are inevitably simplifying and, therefore partial - as when economic models assume individuals always seek to maximise utility. They often assume the world is 'stationary' and linear; encourage the putting of numbers on everything; and cannot account for 'reflexivity' - their own impact upon how people think and behave. They make assumptions that may hold for certain 'small world' problems, and this can help us explore some aspects of radical uncertainty, but they should never be taken as representations of the real world. They simply do not scale to embrace the complexity of the 'large worlds' in which we live.”

Given the complexity of the real world, “Small World or Wind Tunnel” modelling to tackle the problems and uncertainties we face is a sure-fire recipe for disaster!

Leverage and Liquidity - The Axis of Evil

LTCM spectacular returns were built on low levels of its equity capital base and powered by extremely high leverage. At the beginning of 1998, LTCM had an equity base of a little less than $5 billion for an asset portfolio of $125 billion, which meant or a leverage ratio of 25.

· Assets/Equity = $125 billion/$5 billion = 25

Basically, the bottom line was that, if there was a 4% pull back in their portfolio, then their entire equity base would be wiped out.

· Leverage by itself is dangerous enough but when it is combined with illiquidity, it becomes a serious weapon of deadly destruction. LTCM as a strategy pursued matched trades, which combined underpriced and generally illiquid fixed-income securities with very similar but slightly overpriced liquid securities such as 30-year treasuries expecting that over time their market value would revert to fair value and the gap would narrow or disappear. This strategy was clearly predicated on “patient” capital. While investors could be long-term, lenders generally are not. Most of LTCM’s capital was borrowed and lenders are not necessarily patient when their clients are highly leveraged and in times of crisis when capital seeks safe haven in quality and liquid assets, illiquid assets become even more illiquid. If they have to be liquidated on a short notice to meet margin calls because lenders become impatient, they become even cheaper. LTCM was truly exposed to “liquidity risk” as the long side of its portfolio was generally made up of illiquid securities. LTCM fell victim to this vicious cycle. What LTCM overlooked was its exposure to “liquidity risk”.

· The confidence LTCM traders and founders had on their strategy was premised on work by Robert Merton, a Nobel Laureate, and an expert on risk. Merton was convinced that volatility was the sole measure of risk. If a stock or bond had a certain volatility, it might swing higher or lower temporarily but would always return to its calculated rate and LTCM could use volatility as its most important tool. That this assumption was never proved was of no consequence. Added to this was the belief that volatility was mathematically predictable. A large amount of testing was done on volatility, as well as the chance that something could go wrong and LTCM was convinced that it could precisely calculate the odds of what the best, average, and worst days would return, as well as the odds that the portfolio could take serious or mortal losses. Even worst-case calculations showed that the firm could sail through the most punishing financial hurricanes. What they didn’t focus on was leverage or liquidity, which did not matter since volatility was in control. Leverage and liquidity as independent risk elements were considered inconsequential.

· As a result of the firm’s gigantic margin calls and its inability to sell most major positions because they were very illiquid, the fund’s leverage shot up to 100 to 1, which meant that even a 1 percent drop in assets would bankrupt it. But it couldn’t sell to protect itself because its positions were gigantic and always less liquid than the positions it sold short. In the good times its capital, enormously magnified by leverage, made it huge profits. But in those brutal markets, selling even a small fraction of any holding would reduce prices sharply. LTCM was doomed!

Unintended Consequences

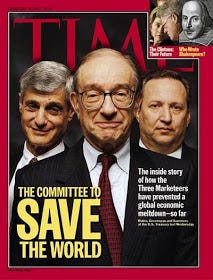

The shadow of LTCM debacle endures even today. The failure of LTCM had the potential to generate broader contagion effects to the financial sector. The official anniversary of LTCM’s downfall is September 23, the day when Alan Greenspan, then Chairman of the Federal Reserve, working with William McDonough, then president of the Federal Reserve Bank of New York, “persuaded” the 14 largest financial firms, into coughing out $3.65 billion to buy all of the assets of LTCM, which had over 60,000 trades on its books comprising over $125 billion of assets and $1.4 trillion notional value of derivatives. McDonough was worried that a disorderly unwind of the firm’s positions would snowball through markets leading to catastrophic losses that would “pose unacceptable risks to the American economy.”

In hindsight, this turned out to be a momentous episode and would reverberate for the next 25 years. Media praised Greenspan’s move and agility. Time magazine put Alan Greenspan, and Treasury Secretaries Robert Rubin and Larry Summers on its cover as “The committee to save the world.” The chaos surrounding a liquidation of LTCM would have, in Chairman Greenspan’s words, “caused the markets to seize up.”

Sadly, as followers of financial markets would recognize, LTCM was a dry run for the leveraged subprime derivative disaster that was to come a mere decade later in 2008-09 and even the more recent Gilt and Banking crises of 2022 and 2023. The terms, Too Big To Fail” and “Systematic Risk” probably existed in regulators lexicon in some form before 1998. But post the LTCM fiasco, they became mainstream and part of the regular thought process. For the too big to fail financial institutions, moral hazard became a way of life. Big financial institutions figured out that they could juice their profits by engaging in ever-riskier behavior because someone else would bear the consequences of that risk. If excess risk-taking leads to disaster, the Fed could be counted on to add liquidity and protect them against catastrophic losses.

This was the birth of “Greenspan Put”, which is still very much alive and kicking, despite it resulting in a greater financial catastrophe a decade later, GFC in 2008.

Lessons not learnt and the rise of carry.

· We have learnt from history, that we don’t learn from history.

The quarter century post LTCM has mostly been a period of very accommodative monetary policies globally and between GFC and Covid pandemic, many western economies were characterized by near zero interest rates. A direct consequence has been rapid increase in “Carry Trade”, a trading strategy that serves as a metaphor for the incentive system built by ultra-loose monetary policy, a financial system highly leveraged and fragile.

Carry provides insight into the fundamental nature of modern finance dominated by shadow banks: Private Equity, Hedge Funds, Money Market Funds etc. Though the nature of the assets they invest are very different, many widely employed trading and investment strategies rely on funding provided by banks, securities dealers, and other money market lenders at short term, or in the form of leveraged loans, typically issued with longer terms but with floating interest rates.

IMF in its recent “Global Financial Stability Report” from April 2023 highlights this fact:

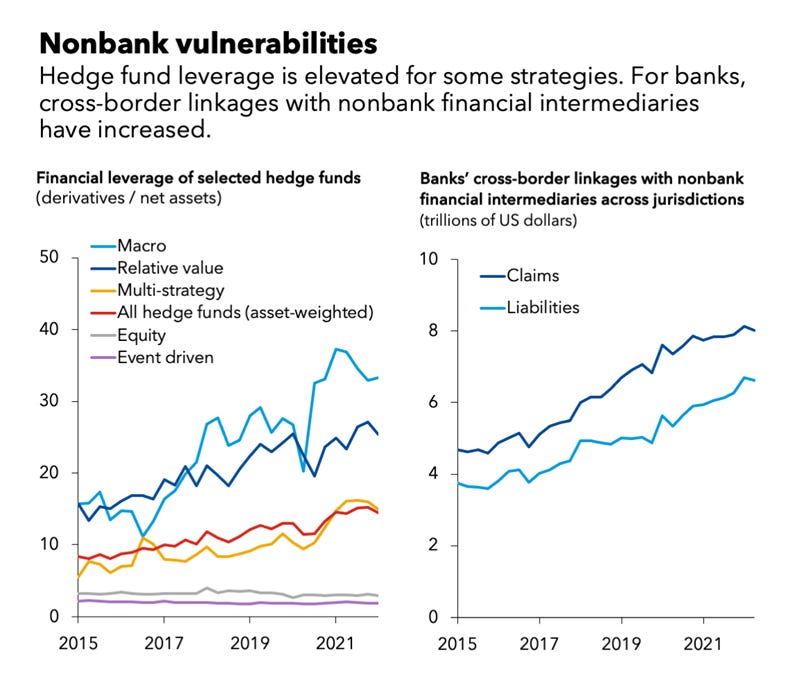

· Nonbank and market-based finance has experienced spectacular growth since the GFC. During this period, the share of global financial assets held by nonbank financial intermediaries (NBFI) has grown from about 40 to nearly 50 percent.

· At the same time, vulnerabilities related to financial leverage, liquidity, and interconnectedness have built up in certain segments of the NBFI ecosystem. Particularly dangerous is the interaction of poor liquidity with financial leverage: The unwinding of leveraged positions by NBFIs can be made more abrupt by the lack of market liquidity, triggering spirals of asset fire sales and investor runs amid large swings in asset prices. Because dealer banks provide NBFIs mostly with financial leverage, interconnectedness can also become a crucial amplification channel of financial stress.

· Liquidity stress in the NBFI sector can spill over to the broader financial sector, as could be seen during recent stress episodes such as the March 2020 dash-for-cash episode or in association with liability-driven investment funds in the United Kingdom, and eventually to the real economy.

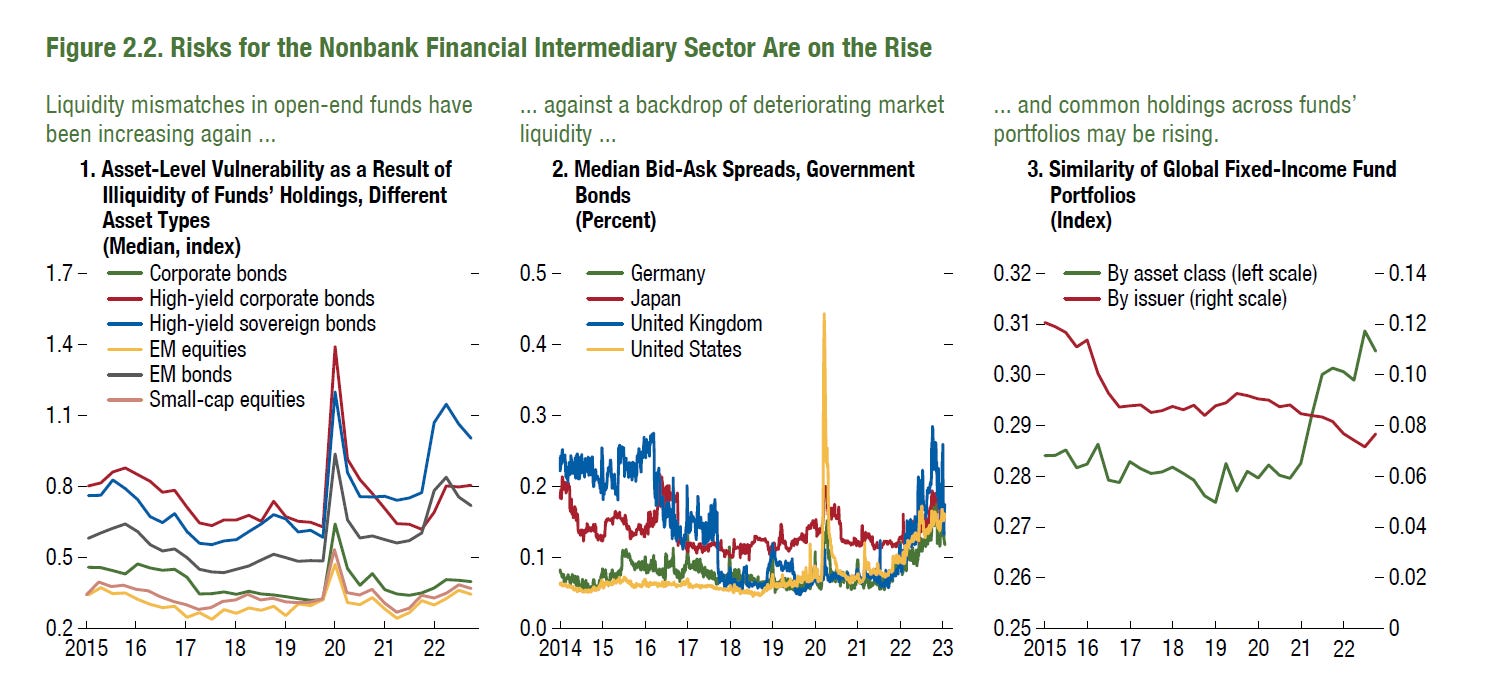

· Over the past year, the liquidity of open-end funds holdings has deteriorated to levels last seen at the onset of the COVID-19 pandemic, implying high vulnerabilities of asset markets as a result of liquidity mismatches.

We cannot predict what might or may happen in the coming months and years. But one thing is certain:

· Financial systems in which many participants rely predominantly on leverage and carry rather than the quality of the assets to reach their return goals are unstable, since small losses can trigger widespread insolvencies.

The past eighteen months have also seen rapid rise in interest rates. Given the amount of leverage in the system, logically something has to break. We managed to avert a banking crisis precipitated by the fall of Silicon Valley Bank, but deep structural faults remain.

Financial institutions still rely heavily on complex mathematical risk models, small world models for large world realities. These models are wrapped in gibberish of Greek alphabets and many of them defy logic. We can be pretty sure that they are not built to evaluate risk arising from the growing complexity and uncertainty globally and Wall Street blissfully lives on, wrapped in the fancy world of “Deficient Market Hypothesis.”

· Progress is cumulative in science, but cyclical in finance.